Key Stats for Helios Technologies Stock

- Current Price: $69

- Full-year revenue: $839 million, +4% YoY (reported); +6% pro forma excl. CFP divestiture

- Full-year diluted non-GAAP EPS: $2.56, +22% YoY

- Q4 revenue: $211 million, +17% YoY; +29% pro forma excl. CFP

- Q4 diluted non-GAAP EPS: $0.81, +145% YoY

- 2026 full-year revenue guidance: $820M–$860M (midpoint $840M; +6% pro forma)

- 2026 full-year diluted non-GAAP EPS guidance: $2.60–$2.90 (+7% at midpoint)

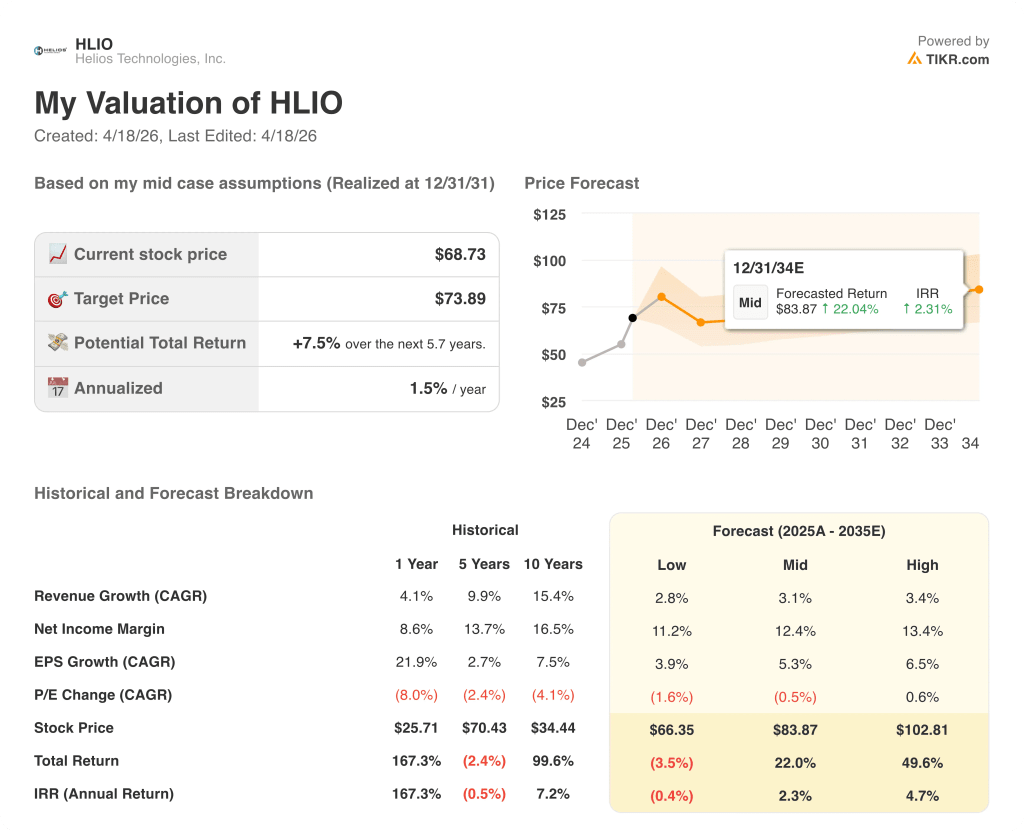

- TIKR model price target: $74

- Implied upside: ~7.5% over 5.7 years (1.5% annualized)

Helios Technologies Stock: Q4 2025 Earnings Breakdown

Helios Technologies stock closed out a genuine turnaround year with Q4 revenue of $211 million, up 17% year-over-year and ahead of the company’s own guidance.

On a pro forma basis stripping out the divested Custom Fluid Power (CFP) business, Q4 growth was 29%.

Full-year revenue came in at $839 million, up just over 4% reported and 6% pro forma, marking the first year of top-line growth after three consecutive years of declines.

Diluted non-GAAP EPS for Q4 was $0.81, up 145% year-over-year, with full-year non-GAAP EPS reaching $2.56, up 22%.

Electronics was the standout segment, posting 31% sales growth in Q4, driven by strength in recreational end markets where one customer is realizing meaningful share gains, plus solid infrastructure-linked construction demand in industrial and mobile channels.

Hydraulics grew 10% in Q4 on a reported basis and 27% pro forma, with construction across all regions the primary driver and the agriculture market posting back-to-back quarters of year-over-year growth, the first such streak since the post-COVID destocking cycle began.

CEO Sean Bagan framed the result directly: “We returned to growth by executing on our customer-centric go-to-market strategic initiative.”

On the capital allocation front, Helios Technologies stock investors received two notable announcements at the March 20 Investor Day: the Board approved the first-ever dividend increase in company history, raising the quarterly payout by more than 30%, and management confirmed $13.6 million in share repurchases in 2025 at an average price around $55 per share.

Adjusted EBITDA margin in Q4 reached 20.1%, the second consecutive quarter back in the 20s, with full-year adjusted EBITDA totaling $161 million.

For 2026, management guided full-year revenue of $820M to $860M, representing 6% pro forma growth at the midpoint, with diluted non-GAAP EPS of $2.60 to $2.90, up 7% at the midpoint.

Q1 2026 guidance calls for revenue of $218M to $223M, up 22% pro forma at the midpoint, with diluted non-GAAP EPS of $0.65 to $0.70, up 53% at the midpoint.

Management flagged chip supply constraints and ongoing tariff uncertainty as the primary near-term risks to the back half of 2026, noting the company locked in component inventory as a partial buffer.

Helios Technologies Stock: Financials

The quarterly income statement tells a clear margin recovery story: four consecutive quarters of gross margin expansion as volume leverage and the removal of the lower-margin CFP business worked through the P&L.

Q4 revenue grew 17.4% year-over-year to $211 million, the strongest quarterly growth rate in the data set, accelerating from 13.3% in Q3 2025.

Q4 gross margin reached 33.8%, up from 31.9% in Q4 2024, continuing a steady climb from the 30.6% trough posted in Q1 2025.

Q4 operating margin expanded to 12.8%, up from 9.9% in Q4 2024 and the strongest quarterly print in the data set shown, confirming the operating leverage management has flagged for several quarters.

Operating income grew 51.7% year-over-year in Q4, the second consecutive quarter of double-digit operating income growth after the 22.5% gain posted in Q3 2025.

The recovery arc is visible across the full 2025 sequence: operating margins of 8.7%, 10.3%, 12.3%, and 12.8% across Q1 through Q4, each quarter stepping higher as volume scaled through a largely fixed cost base.

Management guided 2026 adjusted EBITDA margin to 19.5% to 21%, with gross margin expansion toward the mid-30s cited as the primary driver alongside ongoing productivity initiatives.

Helios Technologies Stock: Valuation Model Take

The TIKR model prices Helios Technologies stock at $74, representing roughly 7.5% total upside from the current price of ~$69, or 1.5% annualized over the 5.7-year model horizon.

The mid-case assumptions are conservative: a revenue CAGR of 3% and a net income margin of ~12%, both modest relative to the 2030 organic growth targets of 5%-plus that management publicly committed to at Investor Day.

The Q4 result and 2026 guidance corridor both reinforce the bull side of the model: the business is accelerating into 2026 with Q1 guided at 22% pro forma growth, adjusted EBITDA margins expanding, and free cash flow at a second consecutive annual record.

The investment case is incrementally stronger after this report, not because the stock is obviously cheap at current levels, but because execution risk has been reduced by nine consecutive quarters of met or exceeded guidance and a first-ever dividend raise that signals management confidence in the forward earnings trajectory.

The central tension this report creates is whether Helios Technologies can sustain double-digit growth through the back half of 2026 given chip supply constraints and tough prior-year comps, or whether H2 momentum fades and the 2030 doubling target depends heavily on M&A execution that has a mixed track record.

Bull Case

- Q1 2026 guidance of 22% pro forma revenue growth and 53% EPS growth at the midpoint implies momentum has carried, not stalled, into the new year

- $60 million in new business wins secured in 2025 represent designed-in, recurring revenue streams that will ramp across 2026 and beyond

- Gross margin expanded 100 basis points in 2025 despite only 6% pro forma revenue growth; additional volume leverage toward the mid-30s target would drive earnings well above the $2.75 EPS guidance midpoint

- The Faster data center liquid cooling product (Project Polar) is under NDA with hyperscalers and represents an addressable market management described as already larger than Faster’s traditional market

Bear Case

- Full-year 2026 EPS guidance midpoint of $2.75 implies only 7% growth on a base that included a one-time $5.4 million interest rate swap benefit in 2025, making the underlying growth rate optically weaker

- Memory chip cost inflation, with some component prices reportedly rising 4x to 5x, is an unresolved headwind that management acknowledged pricing actions alone may not fully absorb

- Hydraulics pro forma growth of 27% in Q4 laps against a very weak prior-year comp; 2025 full-year pro forma Hydraulics growth was a more modest 5% at the segment midpoint guide for 2026

- The CORE 2030 revenue doubling target to $1.6 billion requires roughly $500 million from M&A, and the company has no active due diligence underway as of March 2026

Should You Invest in Helios Technologies, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Helios Technologies stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Helios Technologies stock alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze HLIO stock on TIKR for Free →