Key Stats for Circle Internet Group Stock

- 52-Week Range: $50 to $299

- Current Price: $96

- Street Mean Target: $128

- Street High Target: $280

- TIKR Model Target (Dec. 2030): $471

What Happened?

Circle Internet Group (CRCL) is the world’s largest regulated stablecoin issuer, operating the USDC network: a fully reserved, dollar-pegged digital currency that circulates across more than 30 blockchain networks and is used by financial institutions, enterprises, AI developers, and payment platforms worldwide.

Circle Internet Group delivered Q4 2025 total revenue and reserve income of $770 million, up 77% year-over-year, beating analyst consensus of $739.5 million by roughly $31 million.

USDC in circulation closed the year at $75.3 billion, up 72% year-over-year, with Q4 on-chain transaction volume hitting $11.9 trillion, a 247% increase that reflects the growing velocity of digital dollars across global payment, settlement, and DeFi applications.

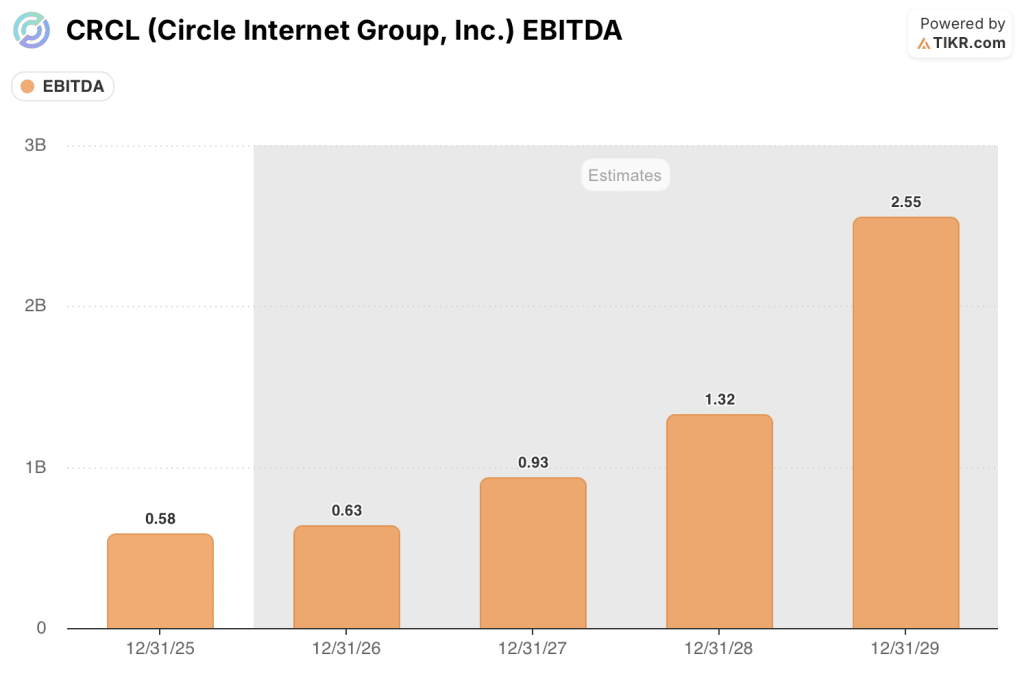

Q4 adjusted EBITDA reached $167 million, up 412% year-over-year, with an adjusted EBITDA margin of 54%, as the operating leverage embedded in the reserve income model became visible at scale.

For full-year 2025, total revenue and reserve income was $2.7 billion, up 64%, and full-year adjusted EBITDA was $582 million, up 104%, though a net loss from continuing operations of $70 million reflected $424 million in stock-based compensation tied to IPO vesting conditions that has no bearing on the underlying cash economics of the business.

CEO Jeremy Allaire framed the broader opportunity on the Q4 2025 earnings call: “USDC adoption continued to expand globally as more enterprises, developers, and public institutions integrated digital dollars into real-world payments, treasury, and onchain financial workflows.”

Circle’s Circle Payments Network, a stablecoin-based cross-border settlement utility for financial institutions, reached 55 enrolled partners as of the earnings call, up from 29 in Q3, with annualized transaction volume of $5.7 billion based on trailing 30-day activity.

Circle Internet Group stock fell sharply on March 25 after CoinDesk reported that a new draft of the CLARITY Act would prohibit yield-bearing rewards on stablecoin balances, with shares declining roughly 19% intraday; the subsequent recovery has been partial, as legislative uncertainty remains the primary near-term overhang.

The CLARITY Act debate is distinct from the structural opportunity: Circle received conditional approval from the OCC in December to establish a national trust bank charter, a development that would deepen its integration into the regulated banking system regardless of where the rewards question lands.

On the platform side, Circle’s Arc blockchain network completed its public Testnet with over 100 major institutions including Goldman Sachs, Deutsche Bank, Visa, and Mastercard actively testing, with Mainnet launch targeted for 2026, a development that opens an entirely new layer of transaction-based revenue.

Wall Street’s Take on CRCL Stock

The 2025 earnings print settled one debate: Circle is not a crypto trading company whose economics rise and fall with Bitcoin, but a reserve income platform where USDC circulation compounds revenue independent of market sentiment, and where the operating leverage on that model delivered 412% EBITDA growth in a single quarter.

Circle’s EBITDA grew 104% in 2025 to $582 million, and while consensus projects a more modest 8.8% step to around $630 million in 2026 as the company invests $570 to $585 million in platform capabilities and global partnerships, the 2027 acceleration to around $930 million in EBITDA, representing 47% growth, reflects a model where revenue scales with USDC adoption while the cost base grows more slowly.

Twenty-four analysts cover Circle Internet Group stock, with 9 Buys and 2 Outperforms against 11 Holds and 2 Sells; the mean target of $128 implies a 33% premium to the current price, while the high target of $280 sits nearly 3x above current levels, a spread that maps directly to whether Circle converts its USDC circulation lead into durable platform monetization through CPN and Arc.

The $280 high target versus the $55 low target captures the debate in full: bulls are underwriting the Arc Mainnet launch, CLARITY Act passage, and USDC’s growing share of on-chain transaction volume (now over 50% of all bridge volume via CCTP); bears are anchoring to EPS compression in 2026 and the regulatory reward uncertainty.

Trading at approximately 31x 2026E EBITDA compressing to approximately 21x 2027E EBITDA as the platform investment cycle pays off, Circle Internet Group stock appears undervalued relative to the 40% USDC circulation CAGR management guided and the EBITDA acceleration already visible in the consensus trajectory.

The clearest signal in the data is USDC’s transaction volume market share: USDC and Tether together account for more than 99% of all on-chain stablecoin transactions, and USDC’s share of that duopoly grew from 39% in Q3 to nearly 50% in Q4, a momentum shift that Mizuho flagged when raising its price target after USDC surpassed Tether in transaction volume for the first time since 2019.

The key risk is distribution cost structure: Circle’s revenue less distribution cost (RLDC) margin is guided at 38% to 40% for 2026, and any deterioration in its Coinbase distribution arrangement, which is the single largest cost line in the model, would compress that margin before the Arc and CPN monetization layers have reached meaningful scale.

The catalyst is the CLARITY Act: passage on a bipartisan basis would remove the regulatory overhang that drove the March sell-off, unlock institutional participation in yield-adjacent stablecoin products, and confirm the legal framework under which Circle’s national trust bank charter becomes commercially operational.

What Does the Valuation Model Say?

TIKR’s mid-case model prices Circle at $471 by December 2030, anchored to a 19.3% revenue CAGR from 2025 through 2035 and a 14.7% net income margin — a target that is driven by USDC circulation compounding at scale rather than by any assumption of an elevated rate environment, meaning the model holds even if reserve return rates compress further from the current 3.81%.

With $390 million in potential total return implied by the mid-case and a high-case target of $1,039, the current price of $96 leaves Circle Internet Group stock undervalued for investors who can hold through the 2026 investment year into the 2027 EBITDA inflection, where consensus projects growth of 47% on the back of a USDC network that is compounding adoption faster than the cost base is growing.

Circle Internet Group stock’s investment case hinges on a single question: does the 2026 operating expense investment, designed to scale Arc, CPN, and global partnerships, translate into durable platform revenue in 2027 and beyond, or does it simply widen a cost structure in a business still dependent on interest rate-sensitive reserve income?

The Opportunity:

- USDC circulation grew 72% in 2025 to $75.3 billion and is guided to compound at a 40% CAGR through the cycle, with Q4 on-chain transaction volume of $11.9 trillion representing 247% growth that is independent of reserve rate moves

- Circle Payments Network enrolled 55 financial institutions as of February 20, up from 29 in Q3, with annualized volume growing 68% sequentially to $5.7 billion, providing the first proof point of platform monetization beyond reserve income

- Arc Mainnet launch in 2026 with 100-plus institutions in Testnet, including Goldman Sachs, Deutsche Bank, Visa, and Mastercard, opens transaction-based revenue that does not exist in the current financial model

- USDC’s CCTP protocol crossed 50% of all cross-chain bridge volume in January, including assets beyond USDC, establishing Circle as the dominant interoperability infrastructure for the Internet financial system

The Risk:

- 2026 normalized EPS is projected to fall 49% to $1.20 from $2.35 in 2025 as adjusted operating expenses step up to $570 to $585 million, a $62 to $77 million increase, creating a clear near-term earnings headwind that keeps institutional buyers cautious

- RLDC margin is guided at 38% to 40% for 2026, flat to slightly down from 39.4% in 2025, meaning USDC growth is currently being absorbed by distribution partners rather than falling to Circle’s bottom line; the Arc buildout is the structural path toward reducing that third-party dependency over time, but that transition remains multi-year

- CLARITY Act passage is not guaranteed, and the March 25 sell-off showed how sensitive Circle Internet Group stock is to regulatory headlines, with the yield-bearing rewards question unresolved as of the last available reporting date

- Reserve return rate fell 68 basis points year-over-year to 3.81% in Q4, and any further interest rate declines would compress the reserve income that currently drives the majority of Circle’s revenue

Should You Invest in Circle Internet Group, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CRCL stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Circle Internet Group, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CRCL stock on TIKR for Free →