Key Takeaways:

- Datadog is still growing quickly, with revenue up 28% in 2025, free cash flow above $1 billion, and a large net cash position.

- The stock is moving on two forces at once: strong execution in cloud monitoring and security, but also investor concern that AI could pressure software valuations across the sector.

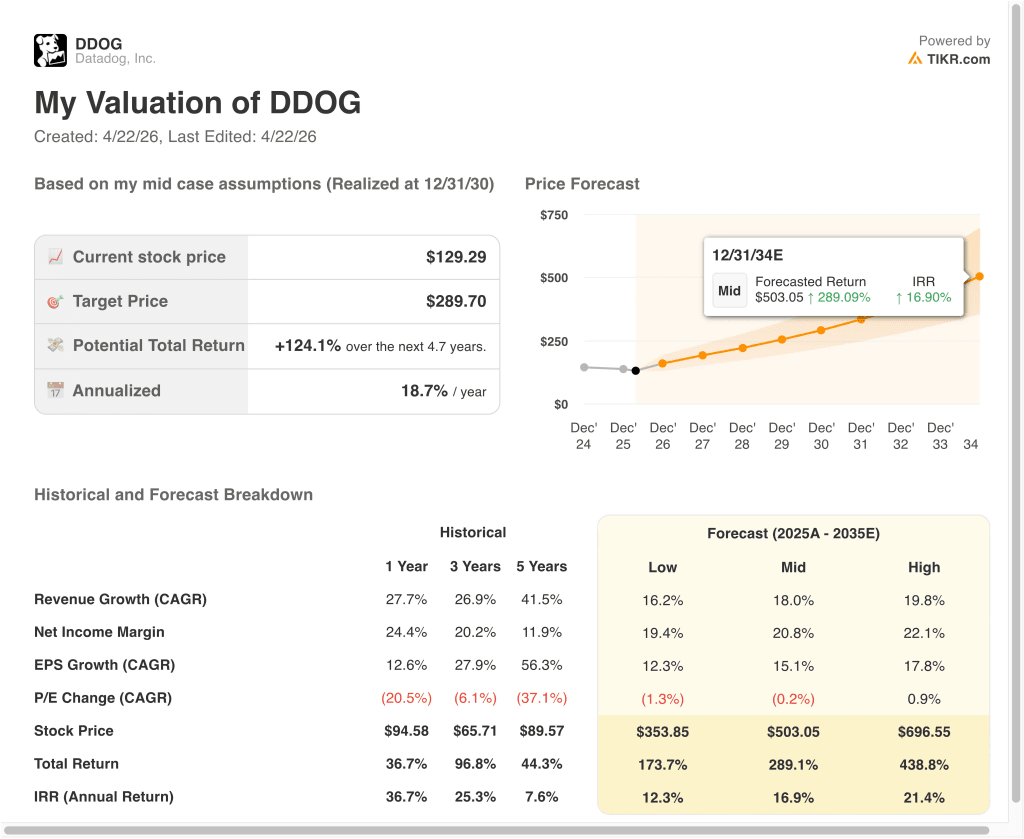

- Datadog stock could reasonably reach around $217 per share by late 2028, based on the valuation model.

- That implies a roughly 68% total return from today’s price of $129, or about 21% annualized over the next 2.7 years.

What Happened?

Datadog (DDOG) is in focus this week because investors are balancing strong company execution against a more fragile mood around software and AI. On April 21, the company published its State of AI Engineering 2026 report, which said about 5% of AI model requests fail in production and that nearly 60% of those failures are tied to capacity limits.

That matters for the stock because Datadog sells observability tools. In plain English, observability software helps companies watch how applications, infrastructure, logs, and security systems behave in real time so engineers can find problems faster. As AI workloads become more complex, Datadog is trying to position its platform as essential infrastructure rather than optional software.

The market is also still reacting to Datadog’s February results. The company reported fourth-quarter revenue of $953 million, up 29% year over year, with non-GAAP EPS of $0.59, above the Reuters-cited consensus of $0.55.

Datadog also said it launched Bits AI SRE Agent, Storage Management, Feature Flags, and Data Observability for general availability, which shows management is pushing product breadth while demand remains healthy.

Still, sentiment around software has been uneven. Reuters reported on April 9 that software stocks tumbled after a new Anthropic update revived fears that AI could disrupt established vendors, and Reuters also noted in February that similar worries had already dragged software names lower across the sector.

Datadog’s next big catalyst is its May 7, 2026, earnings call, which should give investors a fresh read on growth, margins, and how much AI demand is actually helping the business.

Here’s why Datadog stock could keep moving sharply from here: the company is tied to two powerful themes at once, cloud infrastructure complexity and AI spending.

What the Model Says for DDOG Stock

We analyzed the upside potential for Datadog stock using valuation assumptions based on its strong revenue growth, expanding product suite, and improving scale.

Based on estimates of around 20% annual revenue growth, around 22% operating margins, and a normalized P/E multiple of around 60x, the model projects Datadog stock could rise from $129 to $217 per share.

That would be a 67.9% total return, or a 21.2% annualized return over the next 2.7 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for DDOG stock:

1. Revenue Growth: 20%

Datadog has grown revenue from about $1.0 billion in 2021 to $3.4 billion in 2025. Even after that scale-up, revenue still increased 28% last year, which is much faster than most large software peers. That tells us demand is still broad enough to support a premium valuation framework.

The key driver is product expansion inside the customer base. Datadog said it had about 32,700 customers at the end of 2025, up from about 30,000 a year earlier, and it continues to grow the number of larger accounts spending at least $100,000 and $1 million annually.

Based on analysts’ consensus estimates, we use around 20% annual revenue growth. That fits the guided model, and it also reflects a company that is still benefiting from cloud migration, higher product adoption, and new AI-related use cases. It is a slower pace than Datadog delivered in its earlier years, but it is still strong enough to support an above-market valuation.

2. Operating Margins: 22%

Datadog’s margin story is more complicated than its revenue story. On a GAAP basis, operating margin was 1% in the fourth quarter, but it was negative for the full-year 2025 because the company kept spending heavily on product development and stock-based compensation.

Still, the underlying economics are attractive. Gross margin was about 80% in 2025, and the company produced more than $1 billion in operating cash flow and about $1.0 billion in free cash flow. Those numbers suggest Datadog has room to scale margins over time if revenue keeps compounding and expense growth moderates.

Based on analysts’ consensus estimates, we use around 22% operating margins. That aligns with the valuation model and assumes Datadog can convert more of its revenue growth into operating profit as the business matures. It also leaves room for continued investment in AI, security, and go-to-market expansion.

3. Exit P/E Multiple: 60x

The exit multiple stays high because Datadog is still a premium growth company. The market continues to value the business on future earnings power, not on today’s GAAP EPS alone, and Datadog’s current valuation still reflects that view.

Even after the recent volatility, analysts tracked by the platform still show a mean target price of about $178, well above the current share price.

There are reasons to be disciplined, though. Reuters reported that software stocks have sold off more than once this year on fears that AI could disrupt established business models, and Datadog is not immune to that broader reset.

Based on analysts’ consensus estimates, we use an exit P/E multiple of around 60x. That is still a growth multiple, but it is not assuming a return to the most aggressive software valuations of past cycles. In other words, the model assumes Datadog keeps executing, but it does not assume the market becomes euphoric again.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for Datadog stock through 2035 show varied outcomes based on AI observability demand, margin execution, and valuation discipline (these are estimates, not guaranteed returns):

- Low Case: AI demand helps, but growth slows more than expected, and the valuation compresses further -> 12.3% annual returns

- Mid Case: Datadog keeps expanding across observability, security, and AI monitoring while margins improve gradually -> 16.9% annual returns

- High Case: product adoption stays strong, larger customers keep expanding, and valuation holds up better than expected -> 21.4% annual returns

Going forward, Datadog stock will likely move with each new read on AI demand, enterprise spending, and margin discipline. The business is strong enough to support a constructive long-term valuation debate, but the share price will probably stay volatile because the whole software sector is being repriced around AI.

See what analysts think about DDOG stock right now (Free with TIKR) >>>

Should You Invest in Datadog, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DDOG, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track DDOG alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Datadog stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!