Key Stats

- Current Price: ~$325

- Q4 2025 Revenue: $6.1B, +10% YoY

- Q4 2025 Adjusted EPS: $3.40, +8% YoY

- Full-Year 2025 Revenue: $23.5B, +8% YoY

- Full-Year 2025 Adjusted EPS: $12.91, +6% YoY

- 2026 Revenue Guidance: +5% to +8% reported; +4% to +7% organic

- 2026 Adjusted EPS Guidance: $14.50 to $16.50 (+~20% YoY at midpoint)

- TIKR Model Price Target: ~$385

- Implied Upside: ~19%

WESCO International Stock Q4 2025 Earnings Breakdown

WESCO International stock (WCC) closed out 2025 with record Q4 revenue of $6.1B, up 10% year-over-year, driven by 9% organic growth and a record $1.2B quarter from data center sales alone.

Full-year adjusted EPS came in at $12.91, up 6% versus 2024, with Q4 adjusted EPS reaching $3.40, up 8% for the quarter.

The dominant story in the quarter was the Communications & Security Solutions segment, which delivered 17% reported sales growth and 14% organic growth, powered by WESCO Data Center Solutions where sales rose more than 30% in Q4.

For the full year, data center revenue hit $4.3B, up approximately 50% and representing roughly 18% of total company sales, according to David Schulz, Executive Vice President and CFO, on the Q4 earnings call.

CSS backlog ended the year at a record level, up nearly 40% year-over-year, signaling no near-term deceleration in the company’s most important growth vertical.

EES delivered Q4 reported and organic sales growth of 9%, with construction up low double digits and OEM up mid-teens, marking three consecutive quarters of growth across construction, industrial, and OEM.

UBS remained the soft spot: Q4 organic sales grew only 3%, with utility growing mid-single digits on IOU strength while broadband declined high single digits against a tough prior-year comparison.

Public power customers continued to weigh on UBS margins, with Q4 adjusted EBITDA margin down approximately 120 basis points year-over-year, driven by competitive pricing pressure on transformers and elevated customer inventory levels.

Management expects public power sales to return to growth by year-end 2026, not before.

For capital returns, WESCO announced a greater than 10% increase to its annual common stock dividend, raising it to $2 per share, or approximately $100M annualized.

The company guided 2026 adjusted EPS to $14.50 to $16.50, representing approximately 20% growth at the midpoint, with free cash flow guided to $500M to $800M versus $54M delivered in 2025.

Preliminary January 2026 sales per workday were up approximately 15% year-over-year, with segment growth mix broadly consistent with Q4 performance, according to CEO John Engel on the earnings call.

WESCO International Stock: What the Financials Show

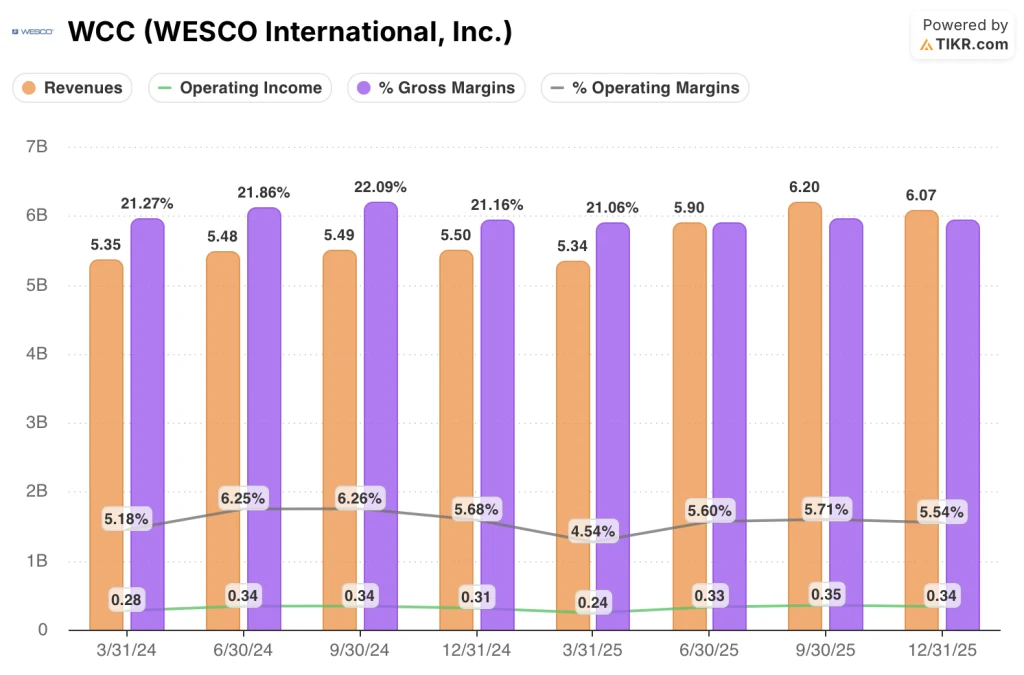

The Q4 income statement tells a steady-state story on margins: WESCO International stock is generating leverage off a rising revenue base, but gross margin expansion remains elusive given mix and competitive pressure in utility.

Q4 revenue of $6.1B came in 10.3% above the prior-year period, the strongest YoY growth rate across the eight quarters visible in the income statement.

Gross margin was 21.2% in Q4, flat versus Q4 2024 and consistent with the 21.1% to 21.3% range that has persisted across most of the trailing eight quarters.

Operating income was $340M in Q4, up 7.6% year-over-year, recovering from a trough of $240M in Q1 2025 when operating income fell 12.4%.

Operating margin came in at 5.5% in Q4, up from 4.5% in Q1 2025 but still below the 5.7% to 6.3% range the company achieved in the first three quarters of 2024.

The operating margin trajectory across the last four quarters: 4.5%, 5.6%, 5.7%, 5.5% — a recovery arc that stalled slightly in Q4 relative to Q3.

Valuation Model Take

The TIKR model prices WESCO International stock at a target of approximately $385, implying roughly 19% upside from the current price near $325.

The mid-case model assumes a revenue CAGR of 4.4% and a net income margin of 3.5% through 2035, representing a modest step up from the 2.8% net income margin WESCO delivered over both the trailing one-year and ten-year historical periods.

The Q4 report strengthens the investment case on the top line: 10% revenue growth with record backlog across all three segments is the exact setup the model needs to reach even its low-case assumptions.

The risk to the thesis is not the revenue line. It is whether WESCO can finally convert volume growth into sustainable gross margin expansion, something that did not materialize in 2025 despite a 9% organic sales year.

With 20% EPS growth guided for 2026 and a 15% January workday sales print, WESCO International stock looks more attractively positioned than the 3.7% annualized IRR in the mid-case model suggests, but that only holds if gross margin begins moving in the right direction.

The central tension this earnings report creates: WESCO International delivered record revenue and record backlog in Q4, yet gross margin has remained essentially flat for eight consecutive quarters, and the market is waiting to see if scale finally translates into margin.

What Has to Go Right

- Data center revenue sustains mid-teens growth in 2026 on a $4.3B base, adding incremental scale to the CSS segment where adjusted EBITDA margin already expanded 50 basis points year-over-year to 9.1%

- IOU momentum, which accelerated from low single digits in Q2 to double digits in Q4, continues into 2026 and offsets the remaining public power drag, driving UBS back toward its historical EBITDA margin range

- The 2026 price increase cycle (Q4 notifications up 125% year-over-year in count, average mid-single digits) actually passes through to revenue and gross margin, unlike 2025 when only 2 points of pricing materialized from similar expectations

- Free cash flow converts from $54M in 2025 to the guided $500M to $800M range as receivables normalize and working capital grows at half the rate of sales

What Could Still Go Wrong

- Gross margin has been range-bound between 21.1% and 21.3% for eight straight quarters; if project mix and public power competitive pressure persist through 2026, the 20% EPS growth guide gets harder to deliver from the top of the income statement

- Public power customers are not expected to return to sales growth until year-end 2026, meaning UBS will remain a margin drag for at least three more quarters

- The $4.3B data center business now faces tougher year-over-year comparisons in the first half of 2026, with data center sales up 70% in Q1 2025; Schulz noted on the call that dollars are expected to be “relatively consistent by quarter” in 2026, implying the growth rate will compress sharply even if absolute volume holds

- The 2026 EPS guide of $14.50 to $16.50 explicitly excludes any future tariff impact, and WESCO operates a large, globally sourced distribution model that is directly exposed to supplier cost increases

Should You Invest in WESCO International, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up WCC stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track WESCO International, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze WCC stock on TIKR for Free →