Key Stats for Extra Space Stock

- 52-Week Range: $126 to $155

- Current Price: $147

- Street Mean Target: $152

- Street High Target: $178

- TIKR Model Target (Dec. 2030): $200

What Happened?

Extra Space Storage (EXR), the second-largest self-storage REIT in the country with more than 4,200 properties, is showing its first real signs of a cycle turn, and Extra Space Storage stock is finally starting to price it in.

The company’s Q4 2025 earnings report delivered core FFO (funds from operations, the standard earnings metric for real estate investment trusts) of $2.08 per share, beating analyst estimates of $2.04 and posting 2.5% year-over-year growth.

The data point investors had been waiting for: 16 of EXR’s top 20 markets turned positive on new customer move-in rates in Q4, compared to just 2 of 20 markets clearing that threshold a year earlier.

CEO Joe Margolis stated on the Q4 2025 earnings call that “we feel better with regard to our positioning going into 2026 than we did heading into 2025, and in our ability to gradually accelerate performance as fundamentals continue to improve through 2026,” citing both strengthening move-in rates and moderating new supply as the twin drivers.

The recovery thesis is not without friction: EXR’s 2026 core FFO guidance midpoint sits essentially flat year-over-year, same-store occupancy slipped to 92.6% from 93.3%, and New York City filed a consumer protection lawsuit in February alleging “predatory” pricing practices across EXR’s 60 New York locations, adding a regulatory overhang to an already cautious setup.

Extra Space Storage stock has recovered roughly 17% off its 52-week low of $126 but remains about 5% below the 52-week high of $155, leaving the valuation in a zone where the recovery thesis and execution risk are priced in roughly equal measure.

Wall Street’s Take on EXR Stock

The Q4 beat matters less than the directional signal underneath it: EXR’s operating trajectory is inflecting in the direction that justifies a meaningful re-rating, even if management set 2026 guidance conservatively.

EXR’s EBITDA is expected to grow around 10% in 2026 to roughly $2.42 billion, a sharp acceleration from the ~5% growth posted in 2025, as property tax normalization and moderating new supply allow operating leverage to flow through more cleanly.

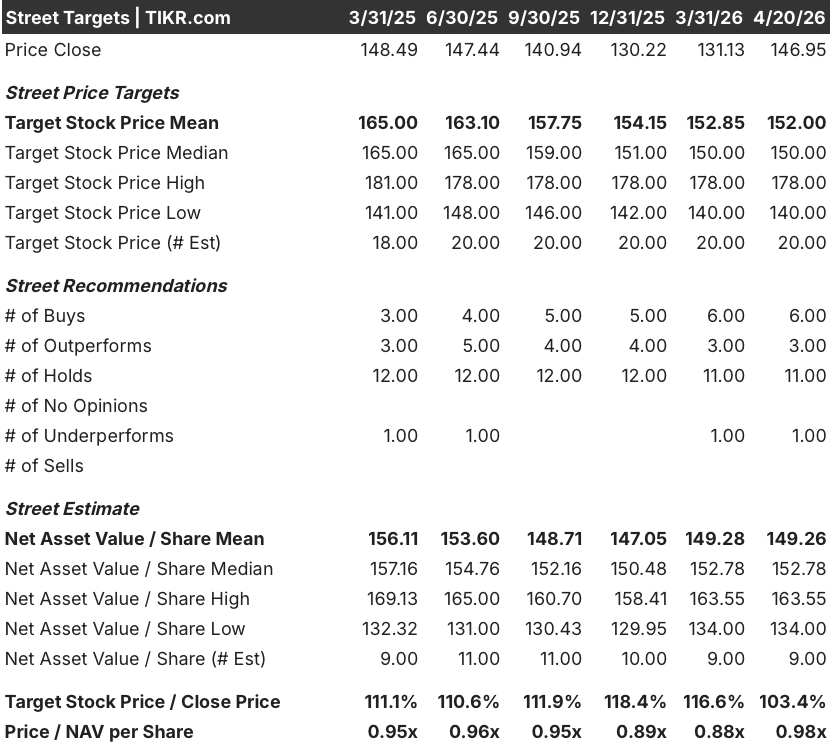

The current analyst consensus reflects deep uncertainty rather than conviction: with 9 bullish ratings, 11 holds, and 2 bearish calls across 21 analysts, the mean price target of $152 implies only around 3% upside from current levels, with the debate anchored squarely to whether the 2026 leasing season delivers the same-store revenue acceleration that two prior years failed to produce.

The street high target of $178 and street low of $140 span a 27% range, and that spread is not noise: it maps to two discrete outcomes for the leasing season, one where move-in rate momentum carries through occupancy stabilization, and one where macro softness and continued oversupply in Atlanta, Phoenix, and Las Vegas extend the recovery timeline by another year.

Priced at roughly 0.98x consensus net asset value per share, Extra Space Storage stock appears undervalued given that the company has historically commanded a premium to NAV during improving operating environments, and the 16-of-20-market move-in rate recovery is the broadest positive signal in two years.

The NYC consumer protection lawsuit is the risk that does not show up in the EBITDA model: if it escalates into structural pricing restrictions or spreads to other jurisdictions, the existing customer rate increase program that drives rent roll monetization faces a regulatory ceiling.

Q1 2026 same-store revenue growth, due April 28, is the single number that settles the debate; any print above 1% would validate that the leasing season is tracking ahead of the flat-to-modest midpoint baked into guidance.

What Does the Valuation Model Say?

The TIKR model’s mid-case target of around $200 per share, representing roughly 36% upside from current levels, rests on a conservative 2% revenue CAGR through 2030 combined with a net income margin holding near 35%, inputs that understate what EXR has historically delivered when self-storage supply and demand normalize.

With the stock at 0.98x NAV and the cycle clearly inflecting, Extra Space Storage stock appears undervalued for investors with the patience to hold through the final leg of supply absorption.

Whether the spring and summer leasing season breaks EXR’s pattern of two consecutive years of flat-to-declining same-store revenue will determine whether the current 0.98x NAV entry is a genuine discount or a value trap.

Bull Case

- Move-in rates turned positive in 16 of 20 markets in Q4 2025, compared to just 2 of 20 a year earlier, the broadest recovery signal since the oversupply cycle peaked

- 2026 EBITDA consensus of roughly $2.42 billion implies around 10% growth, powered by property tax normalization (taxes declined 3.4% in Q4 2025) and controlled expense growth guided at 2% to 3.5%

- Management grew the bridge loan portfolio to $1.5 billion and added 281 net new third-party managed stores in 2025, providing diversified cash flows and an acquisition pipeline that peers without comparable external growth platforms cannot replicate

- Mid-February occupancy was tracking at 92.5% with move-in rates up slightly over 6%, suggesting the same-store revenue guidance midpoint is achievable with no macro tailwind required

Bear Case

- Core FFO guidance midpoint of around $8.20 per share is flat year-over-year despite a constructive operating environment, reflecting management’s own caution after two consecutive years where leasing season underdelivered

- The 40-basis-point drag from Los Angeles County pricing restrictions is a structural 2026 headwind, and the NYC lawsuit seeking over $5 million in penalties introduces reputational risk in EXR’s largest urban market

- Same-store occupancy of 92.6% at year-end 2025 trails the 93.3% posted in 2024, and any further softening in job growth, particularly in Sunbelt markets where EXR is overweight versus peers, would delay demand normalization

- New supply continues to weigh on Northern New Jersey, Las Vegas, Phoenix, and Atlanta, and while the delivery pipeline is shrinking incrementally, the historical pattern is that supply relief arrives later than models assume

Should You Invest in Extra Space Storage Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up EXR stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Extra Space Storage Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze EXR stock on TIKR for Free →