Key Stats — GE HealthCare Technologies Q4 2025 Earnings

- Current price: ~$74

- Q4 2025 revenue: $5.7B (+7% YoY reported; +5% organic)

- Q4 2025 adjusted EPS: $1.44 (-0.7% YoY; +11% ex-tariffs)

- FY2025 revenue: $20.6B (+3.5% organic)

- FY2025 adjusted EPS: $4.59 (+2%; +12% ex-tariffs)

- FY2026 organic revenue guidance: +3% to +4%

- FY2026 adjusted EPS guidance: $4.95–$5.15 (+8% to +12%)

- TIKR model price target: $100.85

- Implied upside: ~36% over ~5 years (around 7% annualized)

GE HealthCare Stock Beats Q4 Estimates, Raises 2026 EPS Guide to $4.95–$5.15

GE HealthCare stock delivered Q4 2025 revenue of $5.7B, up 7.1% on a reported basis and 4.8% organically, exceeding internal expectations.

Adjusted EPS came in at $1.44 for the quarter, down 0.7% year-over-year but up 11% excluding approximately $0.17 per share in tariff impact.

Pharmaceutical Diagnostics was the standout segment, posting Q4 organic revenue growth of 12.7%, driven by global contrast media demand, pricing execution, and adoption of the company’s U.S. radiopharmaceutical MPI portfolio.

Imaging delivered Q4 organic growth of 5.3%, supported by strong execution in EMEA and nuclear medicine, while Advanced Visualization Solutions grew 4.2% organically with continued momentum in cardiovascular ultrasound.

Patient Care Solutions was the drag on the quarter, with organic revenue declining 1.1% year-over-year due to weakness in Life Support Solutions, though EBIT margin recovered 530 basis points sequentially following the resolution of a prior-period product hold.

GE HealthCare stock exited the quarter with a record backlog of $21.8B, up $2B year-over-year and $600M sequentially, with a book-to-bill ratio of 1.06x.

According to CFO Jay Saccaro on the Q4 2025 earnings call, FY2025 tariff impact totaled approximately $245M to EBIT and $0.43 to adjusted EPS; excluding those headwinds, adjusted EBIT margin would have expanded 20 basis points and adjusted EPS would have grown 12%.

For FY2026, management guided organic revenue growth of 3%–4%, adjusted EPS of $4.95–$5.15, and free cash flow of approximately $1.7B, representing 13% growth year-over-year.

The company repurchased $200M in shares at an average price of about $71 since its board-authorized buyback program began in April 2025.

Management flagged a cautious outlook on China as a deliberate headwind baked into the guidance, while citing strong order pipelines in the U.S. and EMEA as the primary supports for the 2026 revenue outlook.

GE HealthCare Stock Financials: Tariffs Compress Margins, Recovery Path Points to 2027

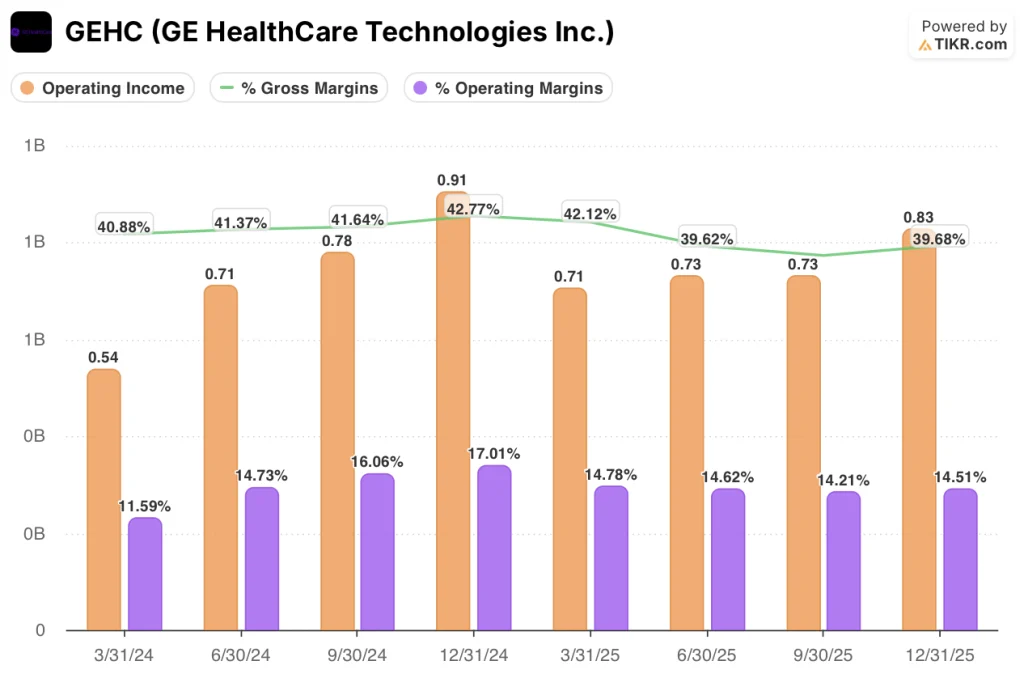

GE HealthCare stock’s Q4 income statement tells a story of solid volume growth running into a tariff wall that has pushed margins well below where they should be for a business with this backlog.

Gross margin came in at ~40% in Q4 2025, down from ~43% in Q4 2024, as tariff costs and mix weighed on the cost structure despite improved volume and pricing execution.

Operating income was $0.83B, with an operating margin of 14.5%, compared to 17% in Q4 2024, a 250-basis-point decline year-over-year.

The trend across 2025 shows operating margin compressing each quarter from ~15% in Q1 to 14.5% in Q4, a meaningful step back from the 17% level the business was running at a year earlier.

Management guided FY2026 adjusted EBIT margin of 15.8%–16.1%, representing 50–80 basis points of expansion from the 15.3% full-year 2025 figure, with tariff mitigation work and Heartbeat-driven productivity gains cited as the primary drivers.

Is GE HealthCare Stock Undervalued? What the TIKR Model Shows

The TIKR model prices GE HealthCare stock at a target of $100.85, implying ~36% total return over 4.7 years from the current price near $74, or about 6.8% annualized.

The mid-case assumptions are a revenue CAGR of 3.6%, a net income margin of 11.6%, and EPS CAGR of 5.1%, reflecting a business in the early stages of a product-cycle-driven reacceleration.

The Q4 report reinforces the setup: record backlog, raised EPS guidance, and a tariff burden that is declining rather than growing in 2026 all support the forward earnings path the model is built on.

GE HealthCare stock is priced for a company still working through a tariff-depressed trough, not for what the innovation pipeline unlocks in 2027 and 2028.

The central tension for GE HealthCare stock: the investment case hinges on whether 9 major product launches convert from order pipeline to revenue at scale in 2027, or whether China pressure, tariff uncertainty, and slower-than-expected Flyrcado ramp prevent the margin step-up the model requires.

Thesis Intact

- Record backlog of $21.8B (up $2B YoY) provides multiyear revenue visibility independent of near-term order fluctuations, with Q4 book-to-bill of 1.06x and trailing 12-month orders growth in the mid-single digits

- Tariff headwind is shrinking: FY2025 impact was ~$245M to EBIT; management guided 2026 tariff expense below that level, with Heartbeat-driven supply chain shifts already repositioning PET/CT and surgery lines to more tariff-efficient geographies

- Pharmaceutical Diagnostics continues to outperform with 12.7% Q4 organic growth, and Flyrcado dose delivery reached ~220 weekly doses as of January 23, with management reaffirming $500M+ revenue potential by end-2028

- FY2026 adjusted EPS guidance of $4.95–$5.15 implies 8%–12% growth, with about $0.30 from volume growth and $0.30 from cost and productivity initiatives even before the new product revenue wave

Thesis at Risk

- Operating margin has compressed from 17.0% in Q4 2024 to 14.5% in Q4 2025, and the FY2026 adjusted EBIT guide of 15.8%–16.1% still sits well below the company’s medium-term target range of high teens to 20%-plus

- China, approximately 10% of total sales, is budgeted down in 2026 after a Q4 2025 that management described as the most challenging comparison quarter of the year; VBP tender win improvements have not yet translated into order flow

- Photon-counting CT (Photonova) and total body PET are not expected to contribute meaningfully to revenue until 2027, meaning the 2026 guide carries limited innovation upside relative to the product launches investors are underwriting

- Amneal has begun launching generic codes of iohexol, the core Omnipaque contrast agent product; while management expressed confidence in supply consistency and portfolio breadth as differentiators, the entry introduces pricing pressure into the highest-growth segment

Should You Invest in GE HealthCare Technologies Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up GEHC stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track GE HealthCare Technologies Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze GEHC stock on TIKR for Free →