Key Stats for Humana Stock

- 52-Week Range: $163 to $315

- Current Price: $205

- Street Mean Target: $210

- Street High Target: $333

- TIKR Model Target (Dec. 2030): $724

What Happened?

Humana Inc. (HUM), one of the largest Medicare Advantage (MA) insurers in the United States — MA being the federally funded program through which private insurers manage care for adults over 65 — is sitting at $205.14 as the regulatory floor under its 2027-2028 earnings recovery has just been materially reinforced.

On April 7, the Centers for Medicare and Medicaid Services (CMS) finalized a 2.48% average payment rate increase for Medicare Advantage plans in 2027, far above the near-flat 0.09% hike proposed in January that sent the entire managed care sector into freefall.

Including a 2.5% adjustment to risk assessment payments tied to member health status, the effective total rate increase reached approximately 5%, translating to more than $13 billion in additional payments to the industry in 2027 and removing the most bearish funding scenario from the table.

Wells Fargo upgraded Humana stock to Equal Weight from Underweight on the news, raised its price target to $227 from $206, and lifted its 2027 profit estimates by approximately 27%, specifically noting that Medicare Advantage margin recovery would contribute roughly 40% of Humana earnings in 2027.

Chief Executive Officer Jim Rechtin stated on the Q4 2025 earnings call that “we are committed to delivering a stable and compelling MA margin and unlocking the earnings potential of the business by 2028,” tying the recovery thesis to a specific three-year operational runway that now carries a more favorable funding foundation.

The CMS relief arrives as Humana absorbs an approximately $3.5 billion Stars headwind in 2026 — Stars being the CMS quality rating system that determines bonus payments to insurers — a headwind management has explicitly guided will reverse as Humana returns to top-quartile ratings by contract year 2028.

Humana grew its Medicare Advantage membership by approximately 1 million members (around 20%) during the most recent annual enrollment period, with over 70% of new sales coming from switchers from competitor plans, creating a compounding earnings base as that cohort matures and marketing costs normalize in year two.

Wall Street’s Take on HUM Stock

The CMS rate finalization does not merely relieve near-term pressure on Humana stock — it restructures the credibility of the $25-plus normalized EPS the company has outlined for 2028, converting a speculative recovery thesis into one with a regulatory foundation.

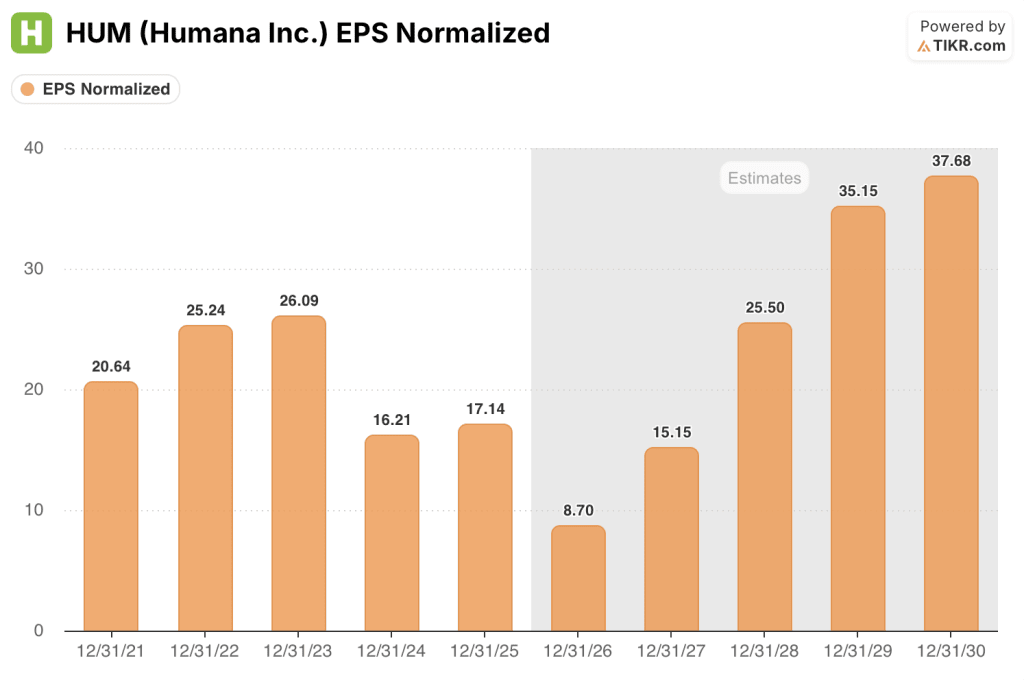

Humana normalized EPS of $17.14 in 2025 compresses to around $9 in 2026 under the Stars headwind, but the consensus recovery to around $15 in 2027 and around $26 in 2028 now has a rate tailwind behind it: the 5% effective CMS increase reduces the depth of benefit cuts management would otherwise need to absorb to protect margins.

Twenty-six analysts cover Humana stock with cautious conviction: 6 Buys, 2 Outperforms, 16 Holds, and 2 Sells, against a mean target of $210 that implies roughly 2% upside at current levels — a consensus that prices in uncertainty about the pace of margin normalization, not a view that the 2028 earnings power is broken.

The spread from the $333 high target to the $146 low encodes the genuine debate: bulls anchor on $25-plus 2028 EPS and a return to 3%-plus MA margins as Stars normalize; bears price in the risk that 2026 membership growth, with approximately 30% concentrated in 3.5-star contracts, delays the Star recovery and keeps margins suppressed through 2027.

Priced at roughly 8x consensus 2028 EPS of around $26 against a historical forward P/E that has averaged well above 15x during periods of stable MA margins, Humana stock appears deeply undervalued for investors with a two-year horizon and the patience for a trough year in 2026 to play out.

Management’s early 2026 operational reads confirm the recovery is tracking as guided: member complaints to Medicare fell year over year in January despite absorbing a million new members, Health Risk Assessment completion rates improved, and transactional Net Promoter Scores rose — all Star-relevant metrics that directly feed into the 2027 bonus payment cycle.

If medical utilization trends accelerate above the high-single-digit cost growth embedded in guidance, the MA margin deepens below breakeven in 2026 and compresses free cash flow needed to fund the membership ramp.

Q1 2026 earnings on April 29 are the first hard data point: the benefit ratio relative to the 90.4% full-year 2025 figure is the number to watch, alongside any revision to 2026 membership or margin guidance that would signal the Stars trough is running deeper than management has indicated.

What Does the Valuation Model Say?

TIKR’s mid-case model prices Humana stock at around $724 by the end of 2030, underwritten by an approximately 9% revenue CAGR and an EPS CAGR of approximately 13% as MA margins normalize off the 2026 trough — assumptions that carry materially more support today than they did when the January rate proposal threatened to compress benefits across the entire MA sector.

With the mid-case implying a total return of approximately 253% from current levels and an annualized IRR of approximately 21%, a recovery in MA margins to the 3%-plus range Rechtin committed to at the 2025 Investor Day makes Humana stock deeply undervalued at roughly 8x 2028 consensus EPS.

The question is not whether the recovery happens — management has committed to it, the rate environment now supports it, and the operational data is tracking. The question is speed: does the $3.5 billion Stars headwind reverse cleanly in 2027, or does it drag into 2028, pushing the trough deeper than the current $9 2026 EPS estimate?

What Has to Go Right

- The 5% effective CMS rate increase for 2027 allows Humana to stabilize benefit structures, reducing the member attrition risk that benefit cuts historically create

- Stars performance returns to the top quartile by contract year 2028 per management guidance, converting the $3.5 billion 2026 headwind into a tailwind over the 2027-2028 period

- The 2026 cohort of approximately 1 million new members matures through the economic curve: acquisition costs normalize in year two, MLR (medical loss ratio, the share of premium paid in claims) improves as care management programs engage, and risk scores adjust upward as chronic conditions are captured

- CenterWell, Humana’s primary care and pharmacy segment, generates incremental accretion from the expanded member base, with pharmacy specifically cited by management as a “significant tailwind” in 2026

What Could Go Wrong

- Medical utilization in 2026 trends above the high-single-digit cost growth embedded in guidance, deepening the MA margin below breakeven and straining the capital efficiency improvements management has built into the 2026 funding plan

- Stars improvement lags beyond contract year 2028: every additional cycle below the 75th percentile extends the earnings trough and pressures the 2028 EPS target that the current 8x multiple depends on

- Approximately 30% of new 2026 members in contracts below 4-star carry undetected chronic conditions not yet reflected in risk scores, producing worse-than-expected MLRs in the near term and delaying the cohort economic improvement management has outlined

- The CMS risk model concession — which Wells Fargo specifically flagged as the removal of a major earnings overhang — is reversed or phased in, resetting 2027 estimate trajectories and reopening the discount to January lows

Should You Invest in Humana Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up HUM stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Humana Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze HUM stock on TIKR for Free →