Key Stats: Astera Labs (ALAB) — Q4 2025 Earnings

- Current Price: $174

- Full-Year 2025 Revenue: $852.5M (+115% YoY)

- Q4 2025 Revenue: $271M (+92% YoY; +17% QoQ)

- Q4 2025 Non-GAAP EPS: $0.58

- Q1 2026 Revenue Guidance: $286M–$297M (+6% to +10% QoQ)

- Q1 2026 Non-GAAP EPS Guidance: $0.53–$0.54

- TIKR Model Price Target: $647 (mid case)

- Implied Upside: +272% from current price

Astera Labs Stock Posted 115% Revenue Growth in 2025. Here’s What the Numbers Show

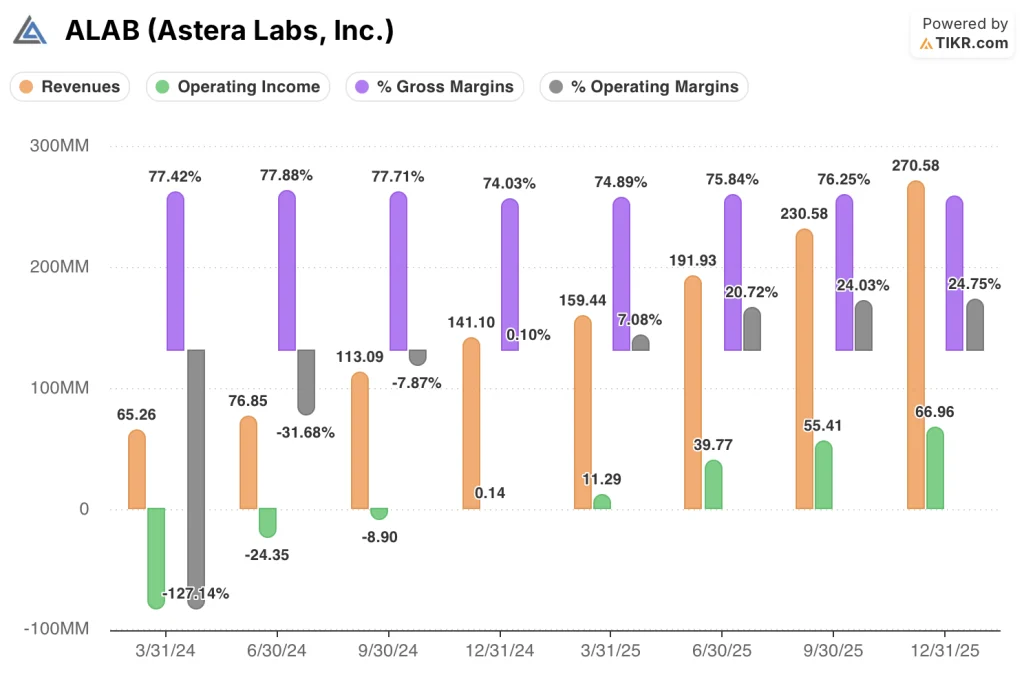

Astera Labs stock (ALAB) reported Q4 2025 revenue of $271 million, up 92% year-over-year and up 17% from the prior quarter, capping a full year in which revenue reached $852.5 million, more than doubling from 2024.

Taurus was the strongest-performing product family in Q4, with full-year Taurus revenue growing more than 4x year-over-year on the ramp of 400-gig programs for scale-out connectivity across AI and general purpose platforms.

Scorpio P-Series crossed 15% of full-year revenue, surpassing the original 10% target, while remaining the only PCIe 6 fabric shipping in volume globally.

Scorpio X-Series shipped preproduction quantities in Q4, with high-volume production targeted for the second half of 2026 and a volume ramp set for 2027.

Aries grew nearly 70% year-over-year in 2025, driven by deployments of custom AI accelerators at large hyperscalers, with PCIe 6 solutions contributing meaningfully in Q4.

CEO Jitendra Mohan stated that Astera Labs has secured design wins for Scorpio P-Series at two additional major U.S. hyperscalers, with revenue contributions expected in 2027.

Astera also announced its first publicly disclosed CXL memory deployment, a partnership with Microsoft, Intel, and SAP to enable CXL memory expansion evaluation within Microsoft Azure M-series virtual machines, with initial production volumes expected in the second half of 2026.

The company also disclosed a new warrant agreement with Amazon covering up to $6.5 billion in cumulative purchases of Smart Fabric Switches, signal conditioning products, and optical engine solutions, with warrants vesting upon achievement of performance conditions through 2033.

Q4 non-GAAP operating expenses rose to $96 million, up $16 million quarter-over-quarter, reflecting R&D expansion including the aiXscale acquisition, and Q1 2026 operating expenses are guided to $112 million–$118 million as the company scales toward optical and scale-up fabric development.

Astera Labs Stock Financials: Operating Leverage Emerging at Scale

Astera Labs stock is at an inflection point on the income statement, with operating income turning positive and expanding rapidly as revenue scale absorbs a historically heavy R&D load.

Quarterly revenue grew from $65M in Q1 2024 to $271M in Q4 2025, a more than 4x increase in four quarters, providing the scale foundation that is now flowing through to operating income.

Q4 2025 non-GAAP gross margin came in at around 76%, down 70 basis points from Q3 due to a higher mix of hardware sales, though the full-year gross margin trajectory remains robust.

Q4 non-GAAP operating margin was ~40%, down 150 basis points sequentially but a dramatic recovery from the operating losses recorded through much of 2024.

GAAP operating income in Q4 2025 reached $66.96 million with an approximately 25% operating margin, compared to $0.14 million and 0.1% in Q4 2024, representing a full operational turnaround in four quarters.

For Q1 2026, management guided non-GAAP gross margin to approximately 74%, reflecting continued hardware mix pressure as Scorpio and Taurus volume builds.

Valuation Model Take

The TIKR model prices Astera Labs stock at $647.32 on a mid-case basis, implying 271.9% total return from the current price of $174.05, with an annualized return of 32.2% over approximately 4.7 years to the end of 2030.

The mid-case model assumes a revenue CAGR of ~25% from 2025 through 2035, a net income margin of ~36%, and EPS CAGR of 23%, with P/E compression of 1% annually as the stock transitions from growth premium to scale.

This Q4 report strengthens the investment case: revenue is accelerating ahead of the Scorpio X volume ramp, the Aries portfolio is still growing, Taurus is diversifying beyond a single customer, and the Amazon warrant validates a multi-year revenue runway at the company’s largest hyperscaler relationship.

The core risk/reward question is whether the Q1 2026 opex step-up, from $96 million to $112 million–$118 million quarterly, compresses margins enough to matter against a revenue acceleration that doesn’t fully hit the income statement until the back half of 2026.

The earnings report reinforces the bull case more than it challenges it, but investors who bought Astera Labs stock expecting 2026 operating leverage to show up immediately will need patience through the investment cycle.

Astera Labs stock delivered 115% revenue growth in 2025, but the Scorpio X ramp, optical buildout, and two new hyperscaler wins are all backend-loaded — the report confirms the thesis, the question is whether execution catches up to the timeline.

What Has to Go Right

- Scorpio X must transition from preproduction to high-volume at the lead customer in H2 2026 on schedule, with 10-plus additional engagements converting to design wins by year-end to support the 2027 revenue ramp management is projecting

- Q1 2026 opex of $112M–$118M must compress as a percentage of revenue as Scorpio X and two new U.S. hyperscaler Scorpio P-Series accounts begin generating material revenue in 2027, validating the 40% non-GAAP operating margin model

- The $6.5 billion Amazon warrant must vest progressively across Smart Fabric Switches, signal conditioning, and optical engines, with the noncash 200 basis point quarterly gross margin headwind starting Q2 2026 absorbed by revenue scale rather than compressing reported profitability

- Taurus 800-gig customer diversification beyond the lead account must materialize in H2 2026 to reduce single-customer concentration that currently defines the signal conditioning revenue base

What Could Still Go Wrong

- UALink native ramp at AWS Trainium 4 and AMD MI 500 is not scheduled until 2027, leaving Scorpio X scale-up revenue entirely dependent on the lead customer’s H2 2026 deployment for any near-term income statement impact

- The NVLink Fusion revenue model remains undisclosed due to NDAs, with margin profile, ASP structure, and attach rate assumptions unverifiable until hyperscaler deployment decisions are made outside Astera’s control

- Non-GAAP opex has risen from roughly $80M quarterly a year ago to a guided $112M–$118M in Q1 2026, a step-up management has explicitly said will continue, with no defined ceiling before the revenue acceleration fully offsets it

- CXL Leo revenue remains immaterial for 2026, with the Microsoft Azure M-series private beta representing the only confirmed deployment and hyperscaler follow-on adoption still unconfirmed

Should You Invest in Astera Labs, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ALAB stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Astera Labs, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ALAB stock on TIKR for Free →