Key Stats for Fortinet Stock

- 52-Week Range: $70 to $109

- Current Price: $82

- Street Mean Target: $89

- Street High Target: $120

- TIKR Model Target (Dec. 2030): $125

What Happened?

Fortinet, Inc. (FTNT) is a global cybersecurity platform company that delivered Q4 2025 billings growth of 18% and revenue growth of 15%, and Fortinet stock now trades at $81.84, nearly 25% below its 52-week high of $109.33.

The quarter’s sharpest signal came from Unified SASE billings, which grew 40% year over year, making Fortinet one of the fastest-growing SASE providers at scale in the $79 billion unified SASE total addressable market.

That 40% SASE billings growth came with product revenue acceleration of 20%, a figure that matters because Fortinet’s 16-year track record shows product revenue growth is the primary leading indicator of service revenue growth in subsequent quarters.

Christiane Ohlgart, CFO, stated on the Q4 2025 earnings call that “our strong performance reflects solid global execution and broad-based demand for our solutions, with product revenue growth accelerating in the second half of the year,” anchoring management confidence in the 2026 full-year revenue guidance of $7.5 billion to $7.7 billion.

Fortinet reaffirmed its midterm targets at the Accelerate 2026 event, pointing to billings and revenue CAGR above 12%, a seventh consecutive year achieving the Rule of 45 (the sum of revenue growth and non-GAAP operating margin), and a $9 billion capital return to shareholders since the company’s IPO.

A memory chip shortage affecting hardware costs represents a near-term input pressure, but Fortinet has maintained roughly six months of inventory and began implementing product-specific price increases of 5% to 20% in March, using a supply chain playbook that produced outsized market share gains during the 2021 COVID-era component crunch.

Wall Street’s Take on FTNT Stock

The product revenue acceleration in Q4, combined with 40% Unified SASE billings growth, shifts the forward earnings trajectory for Fortinet stock from a deceleration narrative to a re-acceleration story tied to three structurally expanding markets.

Fortinet’s normalized EPS reached $2.76 in FY2025, up ~17%, and consensus estimates project around $3 per share for FY2026, supported by the $7.6 billion in billings generated last year and the 21% ARR growth in SecOps that continues to compound the recurring revenue base.

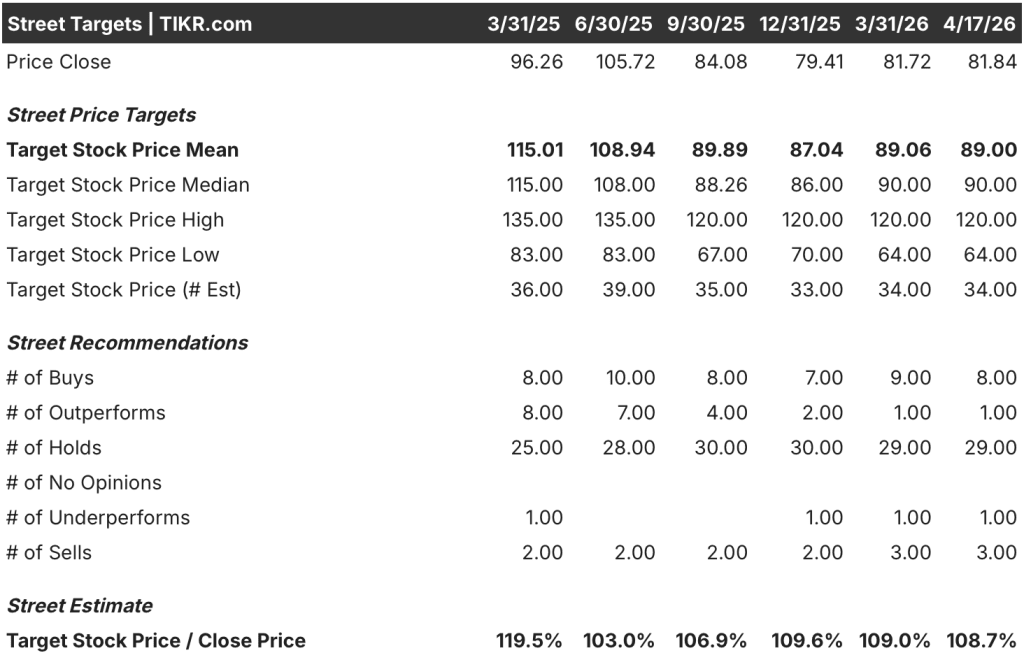

Nine analysts rate FTNT a buy or outperform against 29 holds, with a mean price target of $89 and a street high of $120; Wall Street’s consensus posture reflects hesitation on whether Unified SASE growth can offset decelerating secure networking billings expansion, a question the Q4 40% result has now started to answer.

The analyst target spread from $64 to $120 captures that exact debate: the low end prices in a reversion to single-digit billings growth as SASE competition intensifies, while the $120 target assumes Fortinet’s sovereign SASE differentiation sustains share gains and the product cycle extends through 2027.

Trading at roughly 27x forward earnings versus a historical average closer to 38x, while projecting around 9% EPS CAGR and free cash flow of around $2.5 billion in FY2026, Fortinet stock appears undervalued relative to a business whose three core markets collectively represent over $300 billion in total addressable market and where the company holds less than 20% share in each.

Scotiabank’s warning that Fortinet is “near-term nervous” and may be less well-placed to capture new cybersecurity spending areas represents the key reframing risk the Street is watching.

Memory cost inflation that compresses the 80%+ gross margin profile would break the Rule of 45 commitment and force a guidance reset.

The Q1 2026 earnings call on May 6 is the first data point that will confirm whether the Unified SASE 40% billings growth was a one-quarter inflection or the start of a durable acceleration; watch the billings guidance versus consensus and any commentary on SASE win rates against Palo Alto and Zscaler.

Fortinet Stock Financials

Fortinet generated $6.8 billion in revenue for FY2025, up ~14% year over year, maintaining a steady multi-year compounding trajectory from $3.34 billion in FY2021 at a four-year CAGR above 19%.

Operating income reached $2.07 billion in FY2025, reflecting an operating margin of around 31%, a 40-year high watermark for the company and the sixth consecutive year of Rule of 45 achievement driven by disciplined cost management alongside accelerating product revenue.

Gross margins held at ~81% in FY2025 despite a 20% product revenue quarter in Q4, where hardware mix typically pressures gross margin; the stability signals that service revenue’s contribution at 67% of total revenue is providing a durable margin floor even as hardware accelerates.

Total operating expenses reached $3.40 billion in FY2025, but operating leverage remains intact: operating expenses grew 13% versus revenue growth of 14%, meaning the incremental revenue dollar continues to flow through at a higher margin than the existing base.

What Does the Valuation Model Say?

TIKR’s mid-case model projects a target price of around $125 for Fortinet by the end of 2030, built on a revenue CAGR assumption of around 11% and a net income margin of around 30%, both grounded in the company’s reaffirmed midterm targets and the recurring revenue flywheel now driving 67% of total revenue from services.

With around $126 in mid-case fair value against today’s $81.84 share price, representing around 53% total upside and a roughly 10% annualized return, Fortinet stock is undervalued for patient investors who believe the Unified SASE acceleration is structural rather than cyclical.

The investment hinges on one question: whether Fortinet’s three-in-one FortiOS advantage (network security, SD-WAN, and SASE on a single operating system) translates into sustained SASE share gains or whether Palo Alto and Zscaler close the feature gap and slow FTNT’s momentum in the segment where all near-term re-rating potential lives.

The Opportunity

- Unified SASE billings grew 40% in Q4 2025, more than double the market growth rate, with ARR for FortiSASE up over 90% year over year, establishing a high-velocity installed base

- Sovereign SASE represents a market opportunity Ken Xie estimates could be equal to or larger than the public cloud SASE market, where Fortinet has no major competitor offering an equivalent solution

- Product revenue at 20% growth in Q4 2025 serves as a historical leading indicator for service revenue acceleration; management guided for service revenue growth to pick up in H2 2026 directly tied to this data point

- Fortinet has returned $9 billion since its IPO through buybacks and has $1.3 billion of remaining authorization at current prices, providing per-share earnings support that has already increased EPS roughly 40% since the IPO

The Risk

- Memory cost inflation is real and active: Fortinet implemented price increases of 5% to 20% in March, and if customer pushback on higher hardware prices slows deal conversion, product revenue momentum stalls before the service revenue inflection materializes

- Scotiabank’s cycle analysis suggests the current billings upcycle is roughly five of six quarters through, raising the risk that Q1 2026 billings disappoint and the multiple compresses further from the current 27x forward earnings

- SecOps billings grew only 6% in Q4 2025 on a quarterly basis despite 22% full-year growth, signaling potential volatility in the third pillar that could dampen blended billings growth expectations if SASE momentum normalizes at the same time

Should You Invest in Fortinet, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up FTNT stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Fortinet, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze FTNT stock on TIKR for Free →