Key Stats

- Current price: $602

- Full-year 2025 revenue: $28.5 billion, +20% YoY

- Full-year 2025 adjusted diluted EPS: $10.75, +20% YoY

- Q4 2025 revenue: $7.8 billion (record quarter)

- Q4 2025 adjusted diluted EPS: $3.16 (record quarter)

- Full-year 2026 revenue guidance: double-digit growth expected

- Full-year 2026 adjusted EPS guidance: opportunity for over 20% growth

- TIKR model price target: $846

- Implied upside: +41% over 5 years (~8% annualized)

Quanta Services Stock Delivers a Record Year Across Every Major Metric

Quanta Services stock (PWR) capped 2025 with full-year revenue of $28.5 billion, up 20% year-over-year, while adjusted diluted EPS grew 20% to $10.75, both records for the company.

Q4 alone produced $7.8 billion in revenue and $3.16 in adjusted diluted EPS, both fourth-quarter records.

Cash generation matched the earnings story: full-year cash flow from operations hit $2.2 billion and free cash flow reached $1.7 billion, each a record.

CEO Duke Austin framed the result plainly: “2025 was another year of significant achievement and advancement for Quanta. Again, we delivered record results as we generated double-digit growth in revenues, adjusted EBITDA and adjusted earnings per share, along with record free cash flow and backlog.”

Adjusted EBITDA for the full year reached $2.9 billion, another record, with Q4 EBITDA of $845 million.

The company’s total backlog ended the year at $44 billion, with data center and large load customers representing the fastest-growing segment of that backlog, currently running at roughly 10% of the total.

Quanta completed three acquisitions in Q4 alone: Tri-City Group, Wilson Construction Company, and Billings Flying Service, for aggregate upfront consideration of approximately $1.7 billion funded through cash and stock.

Despite that capital deployment following the earlier Q3 acquisition of Dynamic Systems, the company maintained a leverage ratio below 2x.

For 2026, management guided to continued double-digit growth in revenues, net income, and adjusted EBITDA, with the opportunity to deliver over 20% growth in adjusted EPS.

Free cash flow guidance for 2026 stands at $1.8 billion at the midpoint, which includes $250 million to $350 million in capital expenditures tied to the company’s vertical supply chain expansion into high-voltage transformers and breakers.

At its March 2026 Investor Day, management raised the long-term target: adjusted EPS of $21.60 to $26.75 by 2030, representing a 15% to 20% CAGR off the 2025 base, with organic revenue CAGR of 7% to 10%.

Quanta Services Stock: What the Income Statement Says

Quanta Services stock is backed by an income statement showing consistent revenue acceleration throughout 2025, with quarterly YoY growth rates of 24%, 21%, ~18%, and about 20% across the four quarters.

Gross margin held in a tight band across the year, ranging from ~13% in Q1 to 16% in Q3, with Q4 gross margin landing at around 16%.

Gross profit grew about 15% YoY in Q4 to $1.22 billion, consistent with the 20%-plus gross profit gains seen in Q1 through Q3.

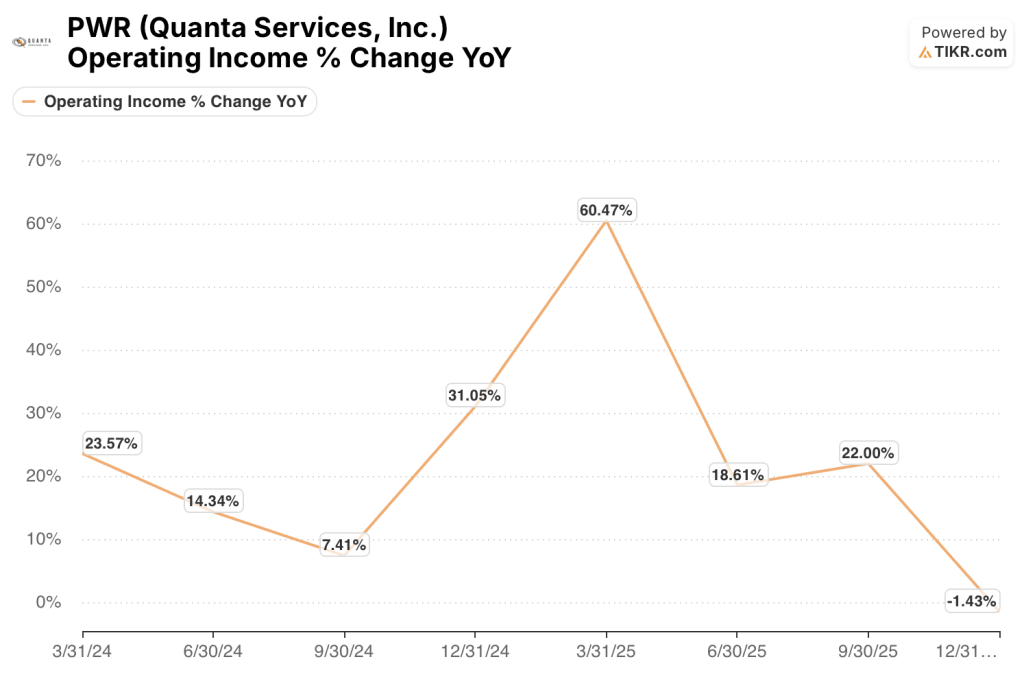

Operating income for Q4 came in at $410 million, a slight year-over-year decline of around 1% from Q4 2024’s $420 million.

Q4 operating margin contracted to ~5% from ~6% in the prior-year quarter, reflecting higher SG&A of $660 million versus $510 million a year earlier, driven in part by acquisition-related activity.

The full-year operating trajectory remains strong: operating income grew ~61%, ~19%, and 22% in Q1 through Q3, with Q4 absorbing the one-quarter drag from the concentrated acquisition spend.

Management guided to 10% to 11% adjusted EBITDA margins by 2030, representing up to 80 basis points of expansion from the 2026 guidance midpoint, citing performance improvements in underground operations, Canadian operations, and growing contribution from fabrication and MEP capabilities.

Valuation Model Take

The TIKR model prices Quanta Services stock at $846, implying roughly 41% total upside from the current price of $602 over the next 5 years, or ~8% annualized.

The mid-case model runs on an 12% revenue CAGR and a 7% net income margin, assumptions that sit inside the range management reaffirmed at its March 2026 Investor Day.

The Q4 result and the full-year 2025 delivery reinforce both pillars of that model: revenue growth came in at exactly 20% for the full year, and the company’s cash generation profile shows free cash flow conversion improving, with management targeting 55% to 60% adjusted EBITDA conversion by 2030.

With a $44 billion backlog, a 9-year consecutive record on adjusted EPS, and a freshly issued 5-year plan that management has framed as a personal commitment, the Quanta Services stock investment case enters 2026 in a stronger position than it did a year ago.

The central tension for Quanta Services stock is whether the market will re-rate the multiple faster than earnings grow, or whether a 30x-plus P/E already prices in the next several years of compounding.

Bull Case

- Record $44 billion backlog with data center and large load representing the fastest-growing segment, with management projecting that pocket alone scales to a $5 billion to $7 billion opportunity per NiSource-type customer

- Management’s 5-year EPS target of $21.6 to $26.75 by 2030 implies the company doubles 28 years of earnings in five, supported by 7% to 10% organic revenue CAGR

- $500 million to $700 million vertical supply chain investment in high-voltage transformers and breakers creates a differentiated, in-house sourcing advantage no competitor can replicate quickly

- Free cash flow of $10 billion to $12 billion projected over the 5-year plan period, giving management significant flexibility to acquire, return capital, and compound ROIC toward 12% to 15%

Bear Case

- Q4 operating margin contracted to ~5% from ~6% a year earlier, with SG&A creeping toward $660 million per quarter as acquisition integration costs pressure near-term margins

- Data center remains only 10% of total backlog today; if large load bookings disappoint in 2026 or hyperscaler capex cycles slow, the fastest-growing segment narrative deflates quickly

- The 765-kilovolt transmission build that management expects to drive a “full stack” upside scenario is not yet in backlog and is not expected to start in 2026, creating a multi-year wait for one of the clearest catalysts

- Leverage below 2x post-acquisition looks healthy but reflects $1.7 billion in Q4 acquisition spend; any acceleration of the deal pipeline toward $10 billion over 5 years again demands sustained free cash flow execution with no misses

Should You Invest in Quanta Services, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up PWR stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Quanta Services, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze PWR stock on TIKR for Free →