Key Stats for Charter Communications Stock

- 52-Week Range: $180 to $437

- Current Price: $237

- Street Mean Target: $275

- Street High Target: $455

- TIKR Model Target (Dec. 2030): $418

What Happened?

Charter Communications (CHTR) stock has fallen more than 46% from its 52-week high as the Spectrum brand, serving roughly 32 million customers across broadband, mobile, and video in 41 states, absorbs peak capital expenditure and sustained broadband subscriber losses simultaneously.

The Q4 2025 results captured both the problem and the pivot in one quarter: Charter lost 119,000 internet customers, but added 428,000 mobile lines, grew video customers by 44,000 for the first time in years, and delivered full-year EBITDA growth of 0.6% while spending $11.66 billion in capital expenditure — the acknowledged peak of a two-generational network investment cycle.

That $11.66 billion peak figure is the number the bear case is built on, and it is also the number that is about to disappear: management guided capital expenditures below $8 billion annually by 2028, a reduction equivalent to roughly $28 per share in annual free cash flow at the current share count.

The mechanism behind that cash release is two large build programs reaching completion: the rural fiber expansion targeting 1.7 million new subsidized passings will be largely finished by end of 2026, and the network evolution upgrading the existing plant to symmetrical multi-gigabit speeds will hit 50% completion this year before finishing in 2027.

CEO Chris Winfrey stated on the Q4 2025 earnings call that “free cash flow will take off from an already significant amount,” linking the CapEx decline directly to a step-change in cash generation that management believes the current stock price fails to reflect.

The Cox Communications acquisition, which would extend Spectrum’s reach to more than 70 million U.S. households, has cleared FCC and DOJ review and awaits final California CPUC approval, with management maintaining a midyear 2026 close timeline where mobile and video penetration in the Cox footprint are both materially lower than Charter’s existing base.

Charter also hired Nick Jeffery, the former CEO of Frontier Communications who drove a documented Net Promoter Score turnaround there, as incoming Chief Operating Officer starting September 2026, targeting the two specific areas management identified as holding back broadband recovery: value messaging and customer service reputation.

Wall Street’s Take on CHTR Stock

Charter Communications stock has been repriced as a value trap by a divided analyst base, but the repricing has overshot: the market is discounting the business at roughly 9.5x forward free cash flow at the precise moment the FCF inflection it has been waiting years to see is finally arriving.

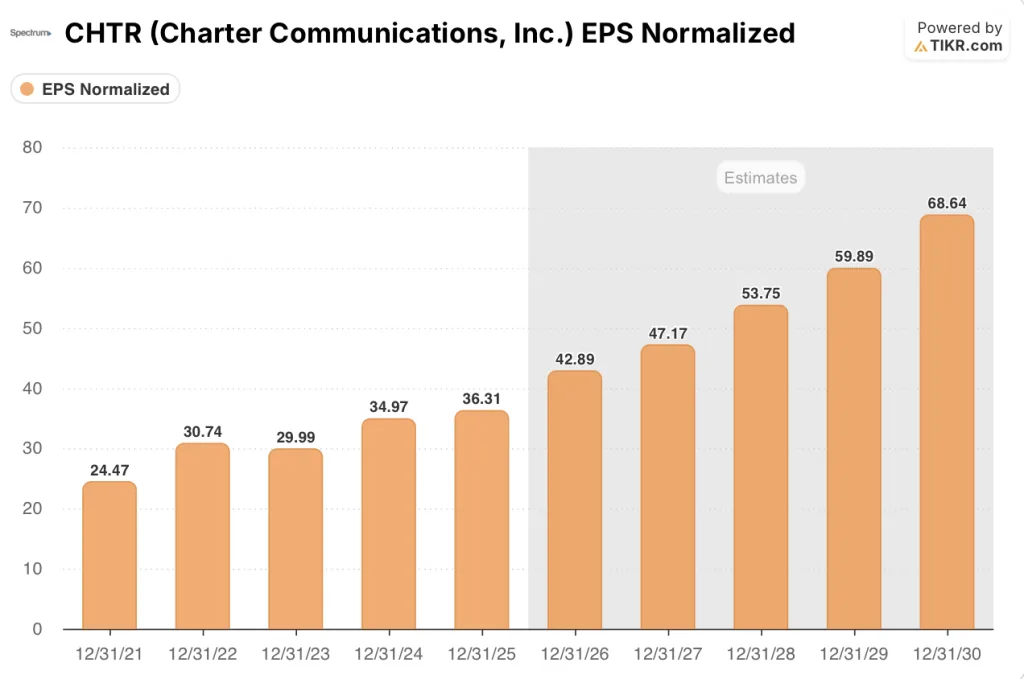

Charter’s normalized EPS is consensus-projected to grow 18% to $42.9 in 2026 and another 10% to around $47 in 2027, powered entirely by share buybacks and cost discipline rather than revenue growth, while FCF is forecast to accelerate from $5 billion in 2025 to around $6.8 billion in 2027 and approximately $7.9 billion in 2028 as the CapEx glide path executes on schedule.

Five buys, nine holds, two underperforms, and three sells across 15 analysts reflects genuine Street disagreement: the bull camp underwrites the FCF normalization while the bear camp prices in broadband subscriber deterioration and Cox integration risk arriving simultaneously.

The spread between the $455 high target and $150 low target captures the full range of that debate, anchored at each end by whether the CapEx reduction is real and whether the Cox acquisition creates scale or compounds leverage risk.

Priced at roughly 9.5x forward free cash flow against a five-year historical range of 15 to 20x and with consensus FCF growing 34% in 2027, Charter Communications stock appears deeply undervalued for investors who believe the CapEx cycle has genuinely peaked and the cash generation inflection is credible.

If broadband subscriber losses accelerate in 2026 rather than stabilizing, the EBITDA growth commitment breaks before the FCF normalization arrives, and the leverage ratio at 4.15x leaves limited room for error.

Q1 2026 results on April 24 are the first test: watch internet net subscriber additions, where any trajectory improvement directly challenges the perpetual-decline narrative currently embedded in the stock price.

What Does the Valuation Model Say?

The TIKR model builds three distinct paths from the current price: the low case targets around $504, a ~113% total return built on a 0.8% revenue CAGR and ~12% net income margins, where CapEx normalization alone justifies a valuation more than double today’s.

The mid case targets approximately $418, a ~77% total return, where rural build and network evolution spending conclude and free roughly $3.5 billion in annual cash; and the high case targets around $746, a ~215% return, where Cox synergies, mobile growth, and broadband stabilization reaccelerate the top line precisely as network building costs drop away.

Across all three scenarios, the gap between today’s price and even the conservative target is the same story: a business forecast to generate approximately $8 billion in free cash flow in 2028 sitting near $45 billion in market cap. At roughly 6x 2028 FCF even in the mid case, Charter Communications stock is undervalued — and the low case makes that verdict hold even if revenue never meaningfully grows again.

The entire case collapses if the CapEx reduction does not materialize on schedule, because without it the FCF inflection that drives all three scenarios never arrives.

What Has to Go Right

- CapEx executes on the guided glide path from $11.4 billion in 2026 to under $8 billion by 2028, releasing the ~$28 per share in annual FCF that management has explicitly flagged as the primary shareholder value driver

- Cox closes midyear 2026 and Charter successfully deploys Spectrum pricing and packaging into the Cox footprint, where mobile penetration is significantly lower than Charter’s existing base, creating immediate revenue per household uplift without additional network CapEx

- Broadband internet subscriber losses stabilize as fixed wireless access competition plateaus, housing starts recover from multi-year lows, and the symmetrical multi-gig network gives Charter a product differentiation it is not yet marketing at scale

- Spectrum Mobile sustains double-digit line growth, with mobile service margins continuing to expand from 34% as the ~90% traffic offload onto Charter’s own WiFi and CBRS network drives ongoing cost efficiencies at scale

What Could Go Wrong

- Fixed wireless competition from T-Mobile and AT&T does not plateau, and broadband subscriber losses accelerate through 2026 and into 2027, preventing EBITDA from growing even as CapEx declines and breaking the financial model before the FCF normalization can arrive

- California CPUC delays or blocks Cox acquisition close, pushing Cox integration synergies out by 12 to 18 months and leaving Charter absorbing transition costs against flat revenue with no offsetting scale benefit

- The 4.15x leverage ratio leaves limited flexibility if EBITDA disappoints, and the commitment to delever to 3.5 to 3.75x within three years post-close constrains share buyback pace at exactly the moment the stock sits near multi-year lows

- Nick Jeffery’s operational improvements, targeting NPS recovery and value messaging clarity, take longer to manifest than the September 2026 start date implies, delaying the customer experience gains management identifies as the missing link between product superiority and broadband retention

Should You Invest in Charter Communications, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CHTR stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Charter Communications, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CHTR stock on TIKR for Free →