Key Stats for Cognizant Technology Solutions Stock

- 52-Week Range: $57 to $87

- Current Price: $61

- Street Mean Target: $83

- Street High Target: $107

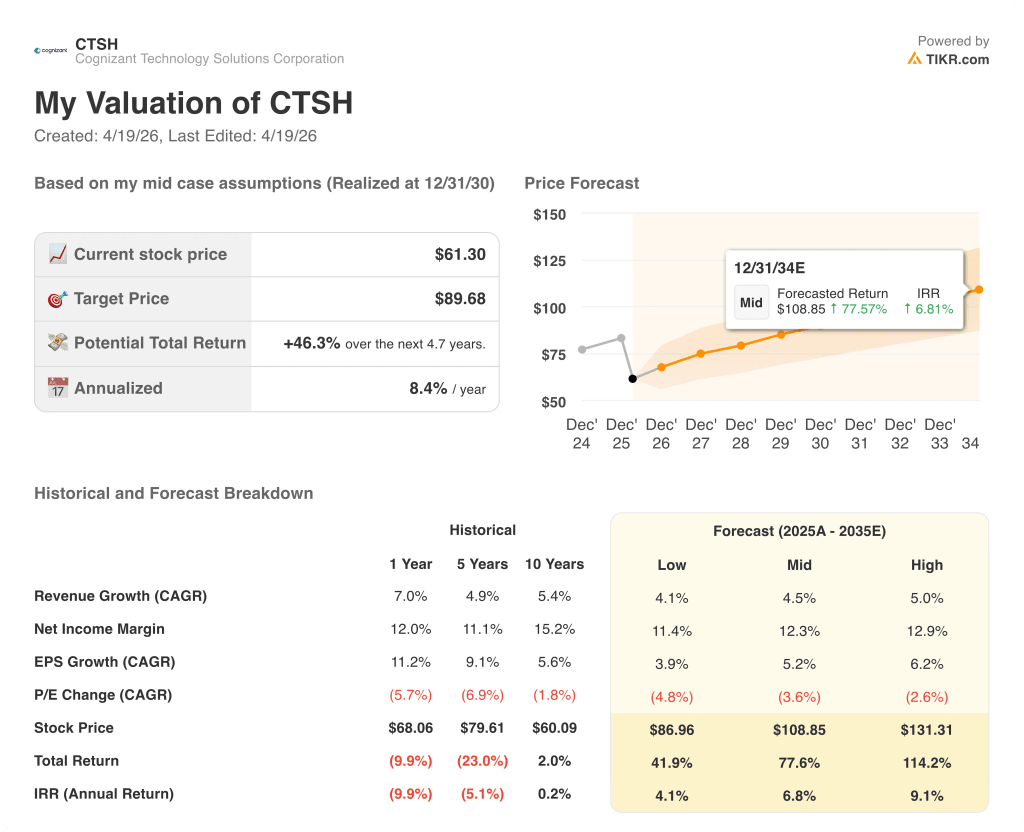

- TIKR Model Target (Dec. 2030): $90

What Happened?

Cognizant Technology Solutions (CTSH), one of the largest IT services firms in the world, has crossed the $20 billion revenue threshold for the first time while trading near its 52-week low of $57.39.

CTSH reported full-year 2025 revenue of $21.1 billion, up 6.4% in constant currency, surpassing the high end of its own guidance range for the first time in years.

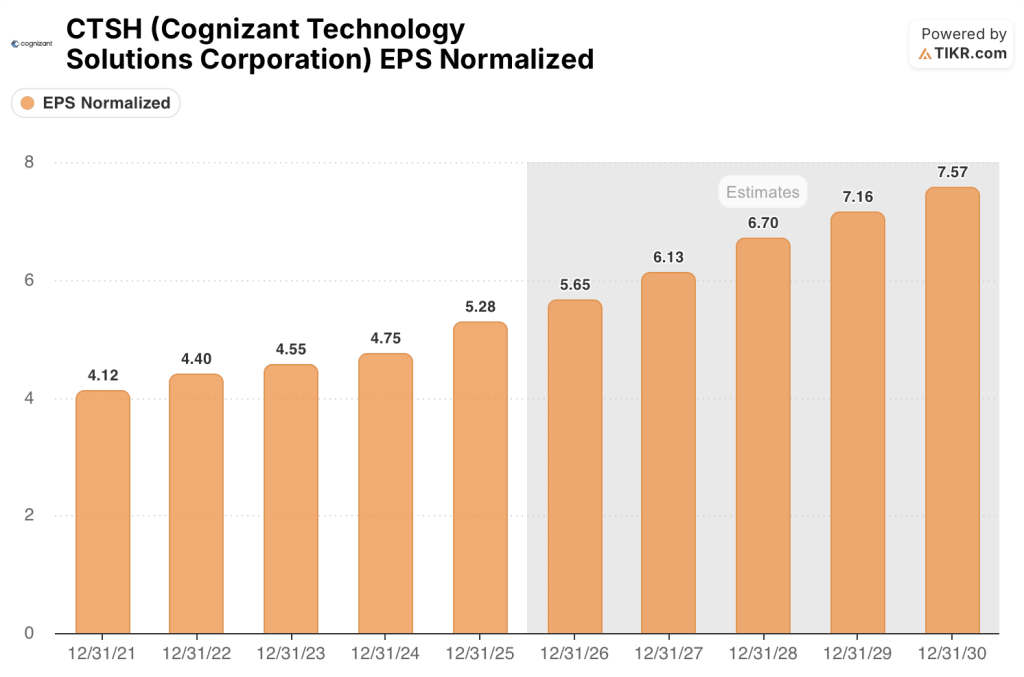

The sharpest number in the report was not revenue: adjusted EPS reached $5.28 for the year, up 11% from $4.75 in 2024, the fastest per-share earnings growth Cognizant has posted in nearly a decade.

Cognizant’s Financial Services segment, its largest vertical, grew 7% for the full year and exited Q4 at a 9% constant-currency growth rate, the best annual performance for that unit since 2016.

CEO Ravi Kumar stated on the Q4 2025 earnings call that “we arrived 2 years early” at the company’s industry winner’s circle target, then outlined a 2026 strategy built around closing the AI velocity gap, the gap between massive enterprise AI infrastructure spending and actual business value realization.

The company signed 28 large deals with total contract value above $100 million in 2025, including five deals above $500 million, with combined TCV up roughly 50% year over year, a backlog-driven pipeline that underpins 2026 guidance of 4% to 6.5% constant-currency revenue growth.

Wall Street’s Take on CTSH Stock

The market has priced Cognizant stock as though the 2022 stagnation never ended, even as the underlying earnings engine has materially re-accelerated.

CTSH’s normalized EPS grew 11% in 2025 to $5.28, more than double its 4.4% growth rate in 2024, driven by the large deal engine producing record bookings and a 50-basis-point adjusted operating margin expansion that has now compounded for two consecutive years.

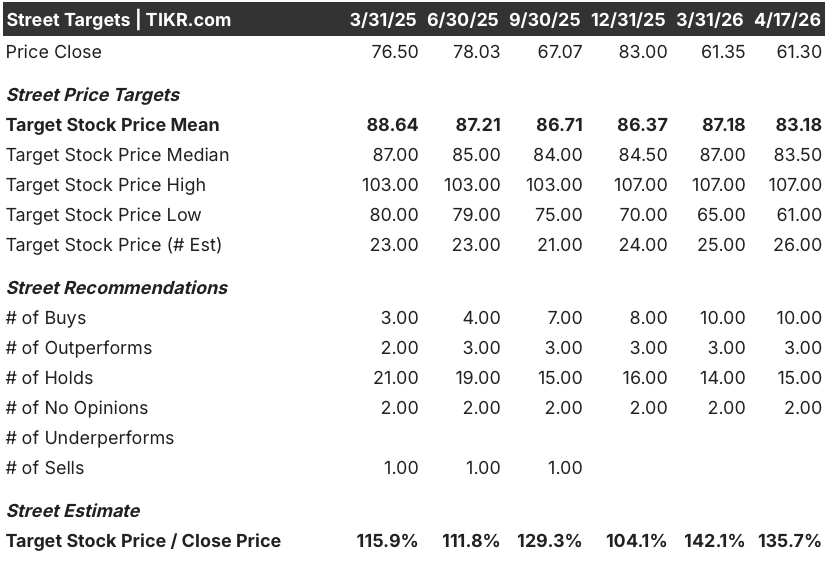

Ten analysts rate Cognizant stock a buy or outperform, 15 hold, and the mean target of $83.18 implies roughly 36% upside from current levels, with Wall Street specifically watching whether the 2026 guidance midpoint of around 5% organic growth holds amid softening discretionary spend in communications and media.

The target spread is worth examining: the high sits at $107, anchored by bulls expecting AI-led agentic deals to scale meaningfully in the second half of 2026, while the low of $61 reflects bears who see discretionary spend remaining frozen outside Financial Services.

Priced at roughly 10.8x forward 2026 earnings against a consensus EPS growth forecast of around 7% and a five-year historical forward P/E that has typically ranged from 15x to 18x, Cognizant stock appears undervalued at a multiple that implies virtually no credit for the AI builder strategy already showing up in bookings and per-share earnings acceleration.

CFO Jatin Dalal confirmed at the Morgan Stanley Technology, Media and Telecom Conference in March that the portfolio of fixed-price deals, now more than 50% of revenue, is tracking within percentage points of planned margins on both revenue and profitability, removing the execution risk the Street embedded after the fixed-price pivot began.

If discretionary spending stalls outside Financial Services through 2026, the 3.8% organic growth midpoint gets tested and EPS growth decelerates toward the low end of the 5% to 8% guidance range.

Q2 2026 revenue and large-deal bookings are the specific numbers to watch: management guided for stronger sequential growth in Q2 and Q3, and any shortfall against that trajectory would challenge the bull case that 2025 bookings are ramping on schedule.

What Does the Valuation Model Say?

The TIKR model’s mid-case target of around $90 per share, built on a revenue CAGR of roughly 5% and net income margins expanding toward around 12%, implies a 46% total return from current levels over roughly five years, a return profile that does not require AI to be a home run, only for the large-deal pipeline to keep ramping at its current pace.

At roughly 10.8x 2026 consensus EPS against a five-year EPS CAGR of around 5%, Cognizant stock appears undervalued for a business that has just posted its fastest earnings growth rate in nearly a decade.

Cognizant’s investment case hinges on a single question: whether the AI velocity gap strategy captures genuinely new addressable spend or simply accelerates a transition to higher-productivity, lower-headcount contracts that limits the revenue ceiling over time.

What Has to Go Right

- Financial Services holds at 7% to 9% growth, keeping the largest vertical from reverting to 2023-level stagnation and anchoring full-year organic growth at the midpoint of the 4% to 6.5% guidance range

- Fixed-price deals, now more than 50% of revenue, continue to deliver within planned margin parameters, as confirmed by the bid-versus-did tracking process Dalal described at the March Morgan Stanley conference

- The 28 large deals signed in 2025, with combined TCV up roughly 50%, ramp on schedule in Q2 and Q3, driving the stronger sequential growth management has explicitly guided for

- The 3Cloud acquisition, closed January 1 and adding more than 1,200 Azure specialists, expands addressable market in AI application innovation without diluting near-term margins

What Could Go Wrong

- Discretionary spending fails to recover in Products and Resources and Communications and Media through 2026, capping organic growth at the low end of the guidance range and pushing EPS toward the bottom of the 5% to 8% growth band

- The productivity pressure embedded in fixed-price deals, where Cognizant underwrites AI-led throughput gains to clients, outpaces internal cost savings before scale catches up, compressing gross margins

- The India primary listing and secondary listing process, still in progress with no committed timeline, creates shareholder uncertainty or produces a structure with unintended consequences for U.S.-listed holders

- Macro softness in North America outside Financial Services limits the discretionary recovery that the $107 high-end analyst target depends on

Should You Invest in Cognizant Technology Solutions Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CTSH stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Cognizant Technology Solutions Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CTSH stock on TIKR for Free →