Key Stats for Marathon Petroleum Corporation Stock

- 52-Week Range: $124 to $256

- Current Price: $214

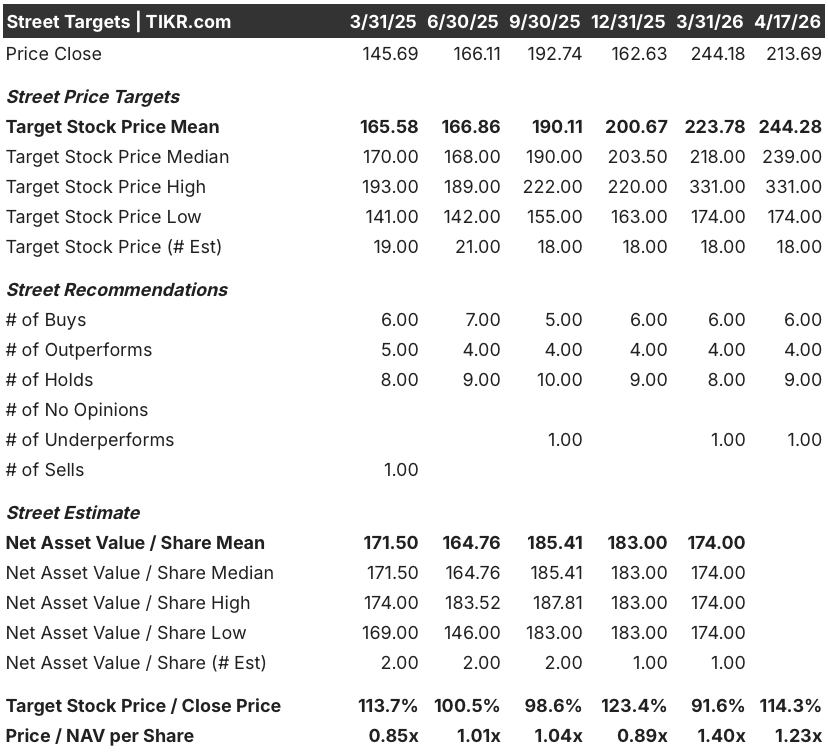

- Street Mean Target: $244

- Street High Target: $331

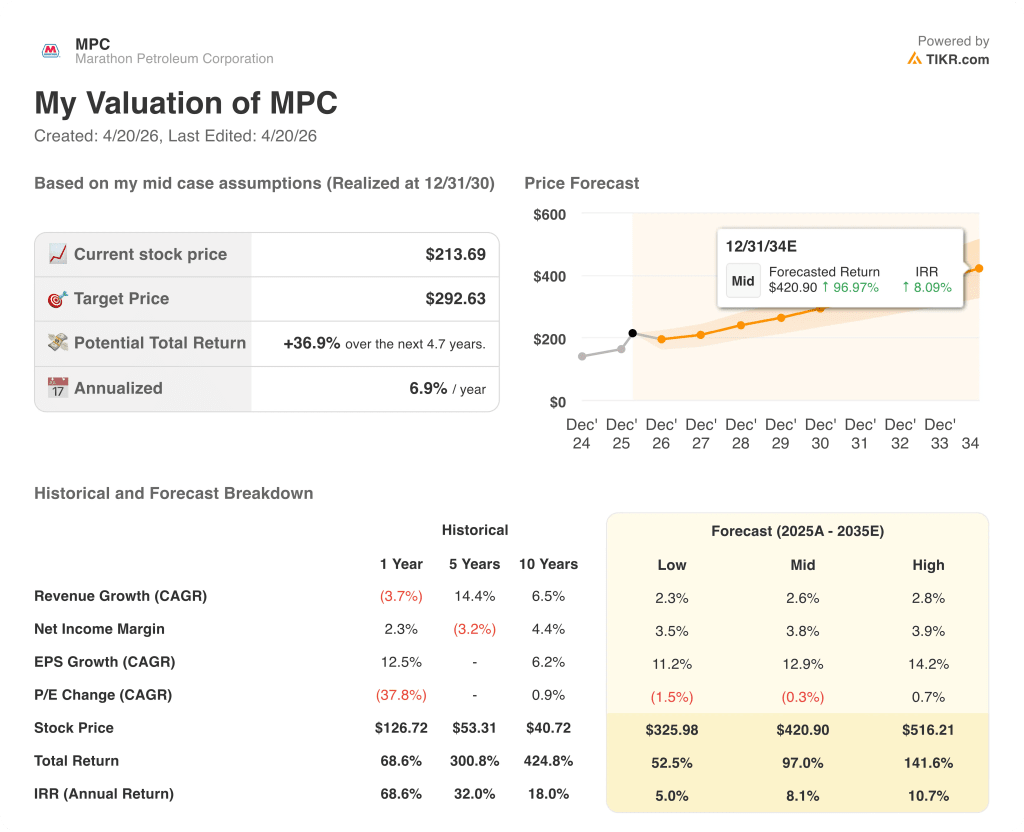

- TIKR Model Target (Dec. 2030): $293

What Happened?

Marathon Petroleum (MPC), the largest independent petroleum refiner in the United States with roughly 3 million barrels per day of throughput capacity, fell 5.55% to $213.69 on April 17 after Iran’s foreign minister declared the Strait of Hormuz open to all commercial vessels, deflating the refining margin premium that had lifted MPC over 47% in the prior quarter.

The selloff reverses part of one of the sharpest sector runs in recent memory: MPC gained over 20% in March alone as Iran’s blockade of the strait — the chokepoint through which roughly 20% of global oil trade flows — starved Asian and European refiners of feedstock, forcing run cuts and redirecting demand toward U.S. Gulf Coast fuel exports.

Gulf Coast refinery utilization had climbed to above 95% in that environment, compared to a five-year seasonal average of roughly 82%, while the U.S. ultra-low sulfur diesel futures premium over WTI crude surged to over $72 per barrel, nearly double the pre-war level, turning MPC into one of the primary beneficiaries of the supply dislocation.

The company had already reported a blowout Q4 2025, posting adjusted EPS of $4.07 against a consensus estimate of $2.88, with full-year refining margin capture of 105% and $8.3 billion in cash from operations — a result CEO Maryann Mannen attributed to the company’s planning and commercial execution rather than a purely windfall environment.

Mannen stated on the Q4 2025 earnings call that “with integrated value chains and a geographically diverse asset base, MPC is well positioned to lead in capital return,” pointing to MPLX, the company’s midstream pipeline subsidiary, which reached a record of nearly $7 billion in adjusted EBITDA in 2025 and is targeting 12.5% distribution growth over the next two years.

Whether the Hormuz opening is durable or a fragile ceasefire interval matters enormously for near-term crack spreads, but the structural case for Marathon Petroleum stock rests on something the geopolitical calendar does not control: three Garyville refinery expansion projects adding 30,000 barrels per day of crude throughput and 10,000 barrels per day of export-grade premium gasoline capacity, both targeted for completion by end-2027.

Wall Street’s Take on MPC Stock

Today’s pullback punishes Marathon Petroleum stock for the Hormuz headline, but the market is pricing in a scenario where the Iran war premium fully evaporates, a thesis that ignores a company that, per its 2025 annual report, delivered 105% full-year margin capture, a 41% Q4 EPS beat, and $8.3 billion in operating cash flow in a year when crack spreads were already compressing heading into Q4.

MPC’s normalized EPS is expected to nearly double from $10.70 in 2025 to around $21 in 2026, driven by the Gulf Coast refining margin environment, Venezuelan crude optionality that widens sour differentials by an estimated $500 million for every $1 move, and MPLX distributions that are targeted to exceed $3.5 billion annually within two years.

Ten of 20 analysts rate Marathon Petroleum a buy or outperform, with a mean price target of $244.28 implying 14% upside from today’s close; the high target of $331 reflects what the bull case looks like if Gulf Coast utilization stays elevated, while the $174 floor prices in a full crack spread normalization back toward pre-war levels.

That $157 spread between the bull and bear targets captures the exact debate today’s Hormuz news opens: the $331 camp believes structural capacity tightness — refined product demand growing 1% to 1.2% annually through 2030, limited new non-petchem capacity coming online, and the Pierce California refinery closure further tightening the West Coast — keeps margins elevated well beyond any ceasefire, while the $174 camp models a rapid return to oversupply conditions.

Trading at roughly 10x the 2026 consensus EPS estimate on a business with record midstream cash flow, Garyville expansion projects targeting 25%-plus returns, and buybacks that reduced shares outstanding by 6.5% in 2025 alone, Marathon Petroleum stock appears undervalued relative to both the earnings trajectory and the capital return capacity the data supports.

MPLX’s 12.5% distribution growth target over the next two years implies expected annual cash distributions to MPC of over $3.5 billion, effectively flooring the capital return program regardless of where crack spreads settle — a structural feature of the thesis the market consistently underweights when refining sentiment turns negative.

If the Hormuz ceasefire holds and Gulf Coast crack spreads normalize rapidly, the 2026 EPS consensus of around $21 would prove too optimistic, compressing multiples and breaking the near-term earnings thesis before the Garyville investments come online to support a structural case.

Q1 2026 earnings on May 5 will be the first real data point on how quickly the margin windfall is fading; the capture rate figure — 114% in Q4 2025 — is the specific number to watch for signs that MPC’s commercial edge is holding despite a softer crack spread environment.

What Does the Valuation Model Say?

The TIKR model’s mid-case scenario, which assumes around 13% EPS compounding annually and modest revenue growth of around 3% through 2030, produces a target price of around $293 for Marathon Petroleum — a 37% total return from current levels — with the Garyville capacity additions and MPLX distribution growth as the two inputs that most directly determine whether the mid-case or high-case assumptions prove accurate.

At roughly 10x forward earnings on a refiner generating $8.3 billion in annual operating cash flow, returning capital at a pace that cut shares outstanding by 6.5% in a single year, and sitting at the origin point of the Colonial Pipeline with direct access to Gulf Coast marine export terminals, Marathon Petroleum stock is undervalued for investors who believe the structural refining thesis outlasts the Hormuz headline.

The bull and bear cases for Marathon Petroleum stock hinge on a single variable: how much of the current refining margin environment is structural tightness versus geopolitical premium, and how fast the geopolitical premium evaporates.

The Opportunity

- Global refined product demand is expected to grow 1% to 1.2% annually through 2030, while net new non-petchem refinery capacity coming online in 2026 is minimal — a backdrop management believes supports elevated margins well beyond the Iran conflict

- Two Garyville refinery projects targeting 25%-plus returns will add 30,000 bpd of crude throughput and 10,000 bpd of export-grade premium gasoline capacity by end-2027, with $160 million of capital deployed in 2026 alone

- MPC runs roughly 50% sour crude across its system — approximately 10% above its closest peer — meaning every $1 widening in sour differentials generates roughly $500 million in annual earnings benefit, a structural advantage that grows with Venezuelan crude re-entry into global markets

- MPLX’s distribution growth of 12.5% over the next two years creates a $3.5 billion-plus annual cash floor for MPC that funds dividends and standalone capital spending independently of refining margins, enabling full excess free cash flow return to shareholders in 2026

- West Coast competitive dynamics shifted permanently with the closure of the Pierce facility in California, leaving Marathon as the primary supplier in the LA region and Pacific Northwest, with management calling the region “short several refineries”

The Risk

- A durable Hormuz reopening compresses U.S. ultra-low sulfur diesel premiums from the $72-per-barrel war-era level back toward the $40 pre-conflict baseline, directly deflating the 2026E EPS of around $21 that underpins the current valuation thesis

- The $157 spread between the Street high and low targets reflects genuine analyst disagreement about the durability of Gulf Coast margin tailwinds; the $174 floor implies a rapid and complete normalization that would leave Marathon Petroleum stock only modestly discounted at current prices

- MPC’s total refining and turnaround capital spend remains above $2 billion in 2026, and while the company guides for reductions in 2027 and 2028, execution risk on the Garyville projects — both targeting year-end 2027 — could delay the production capacity that supports the structural earnings case

- Consensus revenue estimates actually decline in 2027 and 2029, reflecting the Street’s uncertainty about whether near-term margin strength translates into durable revenue growth or simply proves a cycle-peak pull-forward

Should You Invest in Marathon Petroleum Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MPC stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Marathon Petroleum Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MPC stock on TIKR for Free →