Key Stats for Colgate-Palmolive Stock

- 52-Week Range: $75 to $99

- Current Price: $86

- Street Mean Target: $95

- Street High Target: $105

- TIKR Model Target (Dec. 2030): $128

What Happened?

Colgate-Palmolive (CL), the consumer products company behind the world’s most penetrated toothpaste brand — present in nearly 60% of global households — is trading at $85.81, roughly 9% below its level a year ago, even as the business just delivered record cash flow and formally launched its growth blueprint through 2030.

The company’s Q4 2025 results came in stronger than expected, with Colgate-Palmolive posting organic sales growth across all four of its business categories — oral care, personal care, home care, and pet nutrition — for the first time in the year, alongside sequential volume improvement in every division except North America.

Hill’s Pet Nutrition, the science-based premium pet food division that expanded from roughly $3 billion in sales in 2020 to just over $4.5 billion in 2025, posted over 5% underlying growth in Q4 after stripping out the planned wind-down of its private-label contracts.

CEO Noel Wallace stated on the Q4 2025 earnings call that “the flexibility and resilience we have built into our operating model is working effectively to drive value for our shareholders,” pointing to dollar-based EPS growth delivered in a year of tariff headwinds, above-expected raw material inflation, and U.S. category growth that fell below historical levels.

For the full year, Colgate-Palmolive generated $4.2 billion in operating cash flow — a company record — while maintaining over 60% gross profit margins and funding a 63rd consecutive year of dividend increases.

The 2030 strategy, launched alongside Q4 results, centers on AI-powered innovation, omnichannel demand generation, and a Strategic Growth and Productivity Program (SGPP) targeting $200 million to $300 million in restructuring charges that will fund reinvestment in capabilities and margin expansion across the business.

Wall Street’s Take on CL Stock

The market is pricing Colgate-Palmolive stock as a stalled staple, but what the data actually shows is a business that delivered earnings growth through one of the more volatile consumer environments in recent memory and is now entering a five-year investment cycle with stronger capabilities than it has ever had.

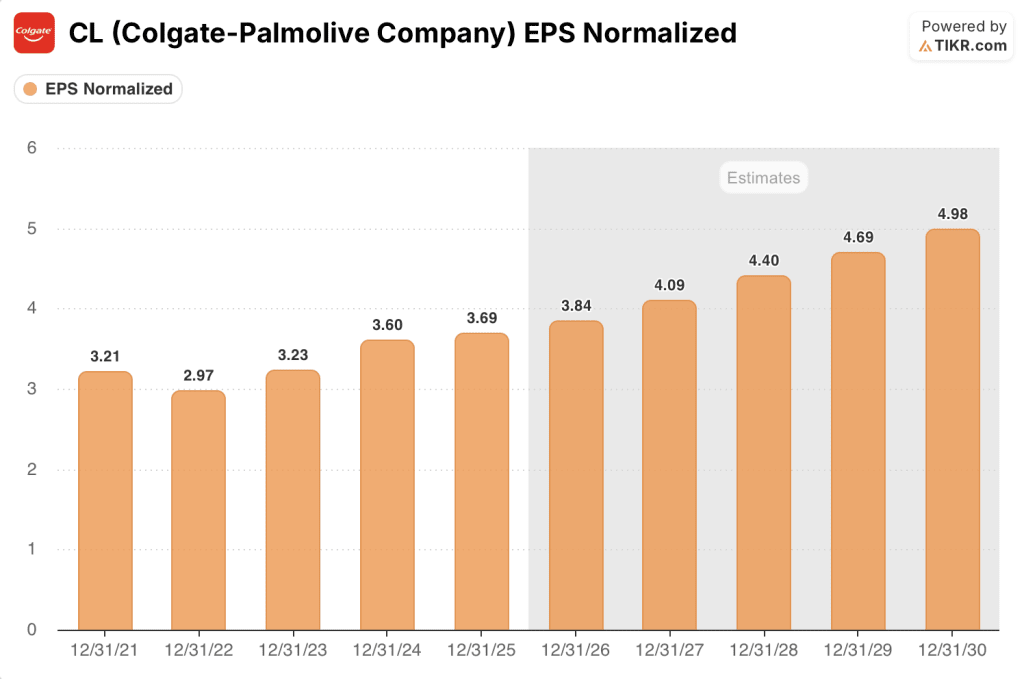

Colgate-Palmolive’s normalized EPS grew from $3.6 in 2024 to $3.69 in 2025 and is expected to reach around $4 in 2026, then compound toward around $5 by 2030, a trajectory supported by the Hill’s growth engine that doubled its advertising ROI through AI-driven data clean rooms and posted its highest-ever media conversion rate in 2025.

With 6 buys, 6 outperforms, 7 holds, and 1 sell among 19 analysts, Wall Street’s conviction is positive but split: the mean price target of $95.42 implies just 11% upside from current levels, which understates the bull case for investors who believe the 2030 strategy generates a premium P/E re-rating as category trends normalize.

The target range, from $79 to $105, captures exactly that debate: the low end reflects a scenario where U.S. category softness persists and organic sales stay pinned at the bottom of the 1%-to-4% 2026 guidance range, while the high end prices in North America recovering and the AI productivity program delivering ahead of expectations.

Trading at roughly 22x forward earnings against a 5-year historical average multiple closer to 26x for a compounder of this quality, with EPS set to grow at around 6% annually through 2030 and 63 consecutive years of dividend growth as proof of capital discipline, Colgate-Palmolive stock appears undervalued relative to both its own history and the earnings trajectory the data supports.

Hill’s data clean rooms, which routed 70% of U.S. media spend through retailer data partnerships in 2025 and doubled marketing conversion rates, have already demonstrated the ROI model management is now scaling into Colgate’s core oral care and personal care categories globally — a capability the market has not yet priced.

If U.S. category growth remains soft through 2026 and the private-label lap at Hill’s delays volume recovery, consensus EPS estimates could drift lower and the re-rating thesis stalls; the free cash flow dip expected in 2026, down around 10% from the 2025 record, is the number to watch for early signs of model stress.

North America innovation launches in Q2 2026, including new Optic White and Max Fresh variants, will be the first real test of whether the 2030 strategy’s premium innovation push can stabilize the company’s weakest region; organic growth in North America in Q2 is the specific figure that confirms or denies the inflection.

What Does the Valuation Model Say?

The TIKR model’s mid-case scenario, which assumes around 3% annual revenue growth and around 6% EPS compounding through 2030, produces a target price of around $128 for Colgate-Palmolive — a 49% total return from current levels — with Hill’s international expansion and SGPP productivity delivery as the two inputs most likely to determine whether the mid-case or high-case assumptions prove accurate.

At roughly 22x forward earnings on a business generating $4.2 billion in annual operating cash flow, with 63 consecutive years of dividend increases and an AI productivity program just entering its execution phase, Colgate-Palmolive stock is undervalued for investors willing to hold through a transitional year.

The argument for Colgate-Palmolive stock hinges on one question: does the 2030 strategy change the growth rate, or is this still a low-single-digit compounder trading at a discount because the market correctly sees limited re-rating potential?

The Opportunity

- Hill’s grew nearly 60% over the 2025 strategy period, carries high single-digit U.S. market share, and operates in European, Latin American, and Asian markets where its penetration remains a fraction of its U.S. position

- The SGPP productivity program, funded by $200 million to $300 million in restructuring charges, is designed to reduce organizational complexity and redirect savings toward brand investment and capabilities — with management guiding for gross margin expansion in 2026 despite continued cost pressure

- AI clean rooms covering 70% of Hill’s U.S. media spend doubled marketing conversion rates in 2025, and management is actively scaling the model into Colgate’s core oral care and personal care categories across 220+ countries

- Colgate Purple toothpaste, developed and validated through AI in China and rolled to every global division within 12 months, demonstrates a new innovation velocity the business did not have five years ago

- Record $4.2 billion in 2025 operating cash flow, low leverage, and 131 consecutive years of dividend payments provide the balance sheet flexibility to pursue bolt-on M&A or accelerate buybacks if category trends remain weak

The Risk

- North America remains the company’s most visible vulnerability: nine core categories were down in volume in October 2025, consumer confidence in the region is fragile, and management explicitly avoided building a material recovery into its 2026 guidance midpoint

- The 2026 free cash flow estimate declines around 10% from the 2025 record as SGPP charges and capability investment weigh on near-term conversion, limiting the financial flexibility that has historically been a buffer against earnings misses

- Organic sales guidance of 1% to 4% for 2026 leaves the stock exposed to a downward estimate revision if U.S. categories do not stabilize by mid-year, and the unusually wide guidance range itself is a signal that management has limited forward visibility

- Hill’s private-label exit created a 360-basis-point volume headwind in Q4 2025 and will not fully lap until Q2 2026, masking the division’s true underlying momentum and making the first half of the year a difficult period to read accurately

Should You Invest in Colgate-Palmolive Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CL stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Colgate-Palmolive Company alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CL stock on TIKR for Free →