Key Stats

- Current price: ~$152 (April 17, 2026)

- Q1 FY2026 net revenues: $3.7B (+6% YoY, record)

- Q1 FY2026 adjusted EPS: $2.86

- Q1 FY2026 pretax margin: 20% (adjusted)

- Q1 FY2026 PCG client assets: $1.71T (record, +15% YoY)

- Q1 FY2026 net new assets: ~$31B (8% annualized growth rate)

- FY2026 guidance: No specific revenue or EPS dollar guidance provided; management guided non-compensation expenses of approximately $2.3B for the fiscal year

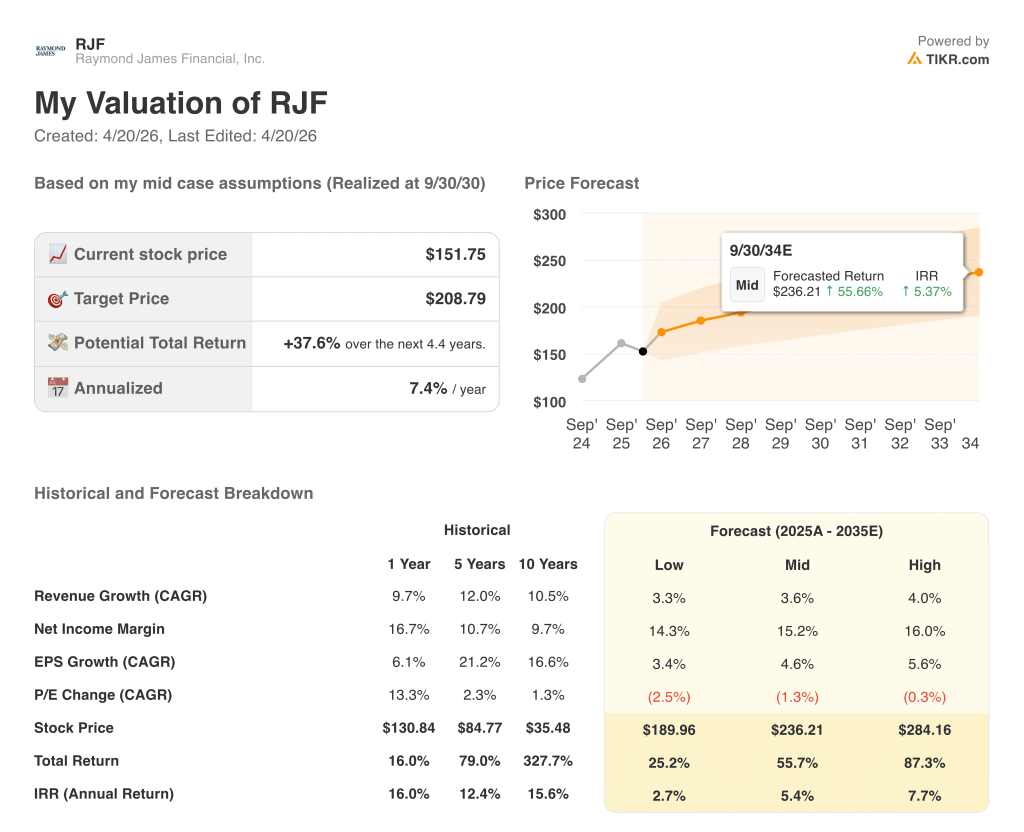

- TIKR model price target: ~$209

- Implied upside: ~38%

Raymond James Financial Stock Posts Record Revenue as Wealth Momentum Offsets Rate and Banking Drag

Raymond James Financial stock (RJF) opened fiscal 2026 with record quarterly net revenues of $3.7B, up 6% year over year, as Private Client Group and Asset Management strength masked a weaker quarter in Capital Markets and rate headwinds in the bank.

Adjusted earnings per diluted share came in at $2.86, with adjusted pretax margin hitting exactly 20%, the firm’s stated target, despite a 125-basis-point decline in short-term rates since early November 2024, according to CFO Jonathan Oorlog on the Q1 FY2026 earnings call.

The Private Client Group drove the quarter, generating record net revenues of $2.77B with client assets under administration reaching a record $1.71T, up 15% year over year.

Domestic net new assets of nearly $31B represented an 8% annualized growth rate, which CEO Paul Shoukry noted on the Q1 FY2026 earnings call would rank as the firm’s second-best quarter ever for that metric.

Recruiting remained a clear differentiator: financial advisers joining during the trailing 12 months carried $460M of trailing 12-month production from their prior firms, a figure Shoukry characterized as equivalent to a meaningful acquisition.

Asset Management delivered a record quarter, with pretax income of $143M on record net revenues of $326M, driven by managed fee-based inflows in PCG annualizing at nearly 10%.

The Bank segment posted record pretax income of $173M, with securities-based loan balances reaching a record $53.4B, up 28% annually in SBL specifically and 10% sequentially, as lower floating rates accelerated client borrowing demand.

Capital Markets was the one weak spot, generating net revenues of $380M and pretax income of just $9M, reflecting tough year-over-year comparables from a strong M&A period and lower sequential M&A and debt underwriting activity.

Shoukry was direct about the drag but pointed to a strong pipeline: “We would be disappointed for the rest of the year if the revenue in the Capital Markets segment doesn’t improve meaningfully above the $380 million level,” according to his remarks on the Q1 FY2026 earnings call.

The firm returned $511M to shareholders in the quarter through dividends and repurchases, buying back $400M of common stock at an average price of $162.

Raymond James Financial stock also announced the acquisitions of boutique investment bank GreensLedge and asset manager Clark Capital Management, which brings over $46B in combined discretionary and nondiscretionary assets, with both deals framed as cultural and strategic fits rather than synergy-driven transactions.

Management guided Q2 FY2026 asset management fees to be approximately 1% higher than Q1 levels, partially offset by two fewer billing days, while aggregate net interest income and RJBDP fees were guided down approximately 3% sequentially from Q1.

Raymond James Financial Stock: What the Income Statement Shows

The Q1 FY2026 income statement tells a margin resilience story: the firm held its adjusted pretax target of 20% in a quarter simultaneously pressured by lower rates, a soft Capital Markets result, and rising recruiting-related compensation.

Total revenues of $3,738M grew approximately 6% year over year, up from $3,537M in the prior-year December quarter.

Net interest income of $566M grew 7% year over year, a reversal from the negative trajectory seen across each quarter of the prior fiscal year, when YoY NII changes ran from -16.2% in the March 2024 quarter through -1.5% in the March 2025 quarter.

Operating income of $738M declined 2.6% year over year from $758M in the prior-year December quarter.

Operating margin for Q1 FY2026 was 19.7%, down from 21.4% in the year-ago period, a contraction driven by rate compression and Capital Markets revenue mix rather than structural cost deterioration.

The firm’s noncompensation expense guidance of approximately $2.3B for the full fiscal year implies roughly 8% growth over the prior year’s adjusted base, which management attributed primarily to technology investment and growth-variable costs including recruiting support and FDIC premiums.

Valuation Model Take

The TIKR model prices Raymond James Financial stock at approximately $209, representing about 38% total upside over the next 4.4 years from the current price near $152, or about 7.4% annualized.

The mid-case assumptions are conservative relative to the firm’s historical track record: a revenue CAGR of 3.6% against a 1-year historical rate of 9.7% and a 5-year rate of 12.0%, with a net income margin of 15.2% against the current trailing 1-year margin of 16.7%.

The Q1 result strengthens the investment case modestly: holding a 20% adjusted pretax margin through a quarter with meaningful rate and Capital Markets headwinds demonstrates the business mix is more durable than a rate-sensitivity-only framework would suggest.

Raymond James Financial stock looks like a steady compounder priced for slower growth than it has historically delivered, and the model’s conservatism means the upside case does not require an optimistic macro scenario to materialize.

The central tension for Raymond James Financial stock is whether the Capital Markets recovery arrives fast enough in FY2026 to offset the NII compression from lower rates and justify a re-rating above current levels.

What Has to Go Right

- Capital Markets revenues recover meaningfully above the $380M Q1 floor, as management guided and pipeline commentary supports, closing the gap to prior-year levels exceeding $500M

- Securities-based loan growth, which added close to $2B in a single quarter, continues to expand the interest-earning asset base, offsetting NII per-dollar compression from lower yields

- PCG fee-based assets, up 19% year over year to $1.04T, drive sustained asset management fee growth, with Q2 guidance already pointing to a 1% sequential increase

- Clark Capital and GreensLedge close and integrate without meaningful disruption, adding $46B+ in AUM and expanded securitization capability

What Could Still Go Wrong

- NII and RJBDP fees guided down 3% sequentially in Q2, and any additional Fed rate cuts would extend that compression for the full year without immediate offset

- Capital Markets timing risk is real: management explicitly declined to guide on closing timing, and a second consecutive soft quarter would pressure the full-year margin target

- Recruiting-related compensation, newly broken out this quarter, is rising as a direct result of $460M in recruited production over the past 12 months, and sustained recruiting activity implies this line does not revert

- PCG pretax income fell 5% year over year despite record client assets, a signal that rate-driven revenue pressure inside the segment is not yet fully behind the firm

Should You Invest in Raymond James Financial, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up RJF stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Raymond James Financial, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze RJF stock on TIKR for Free →