Key Stats for UPS Stock

- Current Price: $107.11

- Target Price (Mid): ~$175

- Street Target: ~$113

- Potential Total Return: ~64%

- Annualized IRR: ~11% / year

- Earnings Reaction: (3.26%) on January 27, 2026

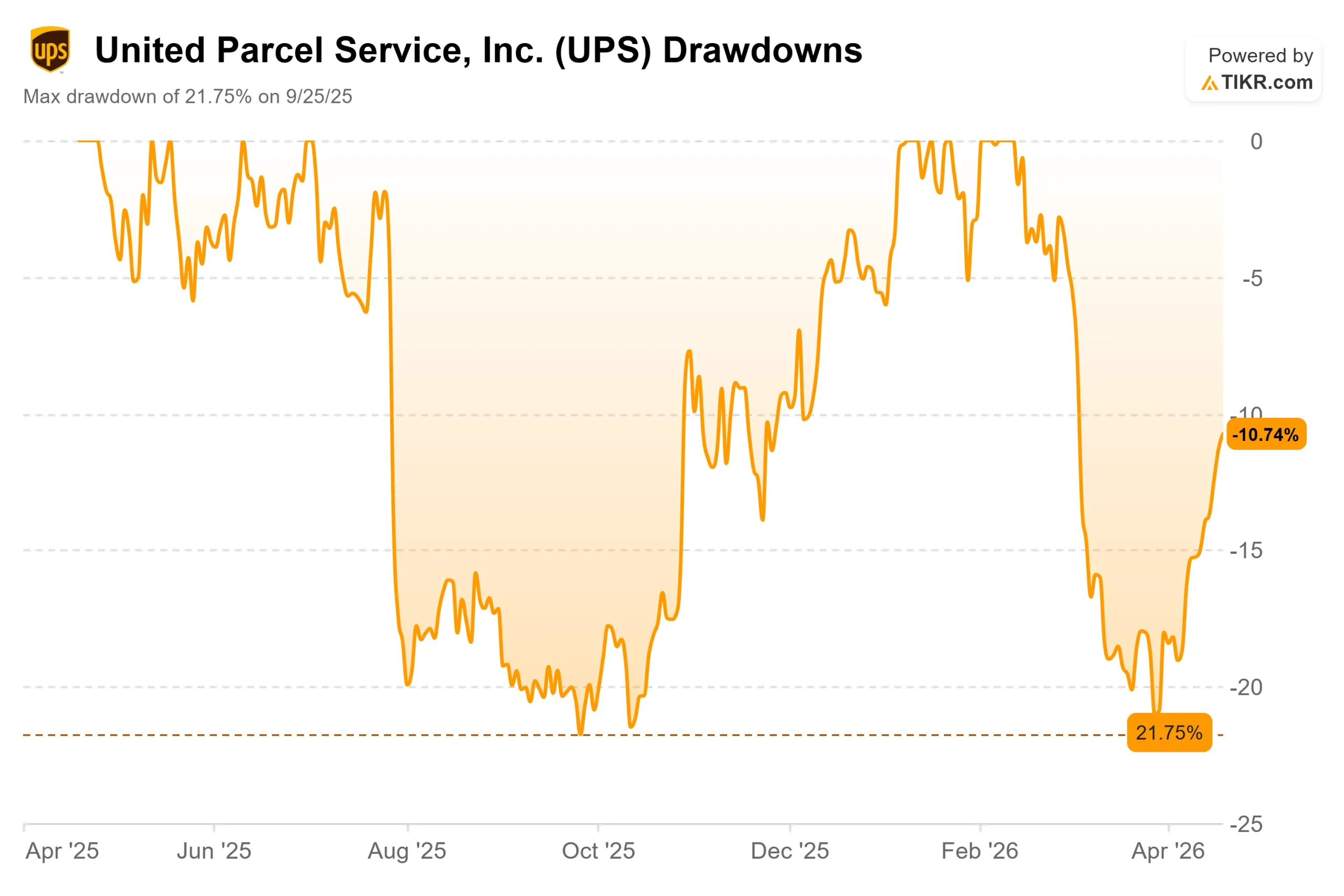

- Max Drawdown: (21.75%) on September 25, 2025

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

United Parcel Services (UPS) has lost 39% of its value over the past five years, yet it has steadily recovered from a max drawdown of 21.75% in September 2025 to close at $107.11.

The debate is simple: bulls believe the worst is structurally behind the company as the Amazon volume exit nears completion and automation compounds into unit cost savings.

Bears point to four straight years of declining or flat revenue, a 96.9% LTM payout ratio that leaves almost no buffer if earnings disappoint, and ongoing labor negotiations that could delay the second-half recovery management has promised.

Both sides are watching on April 28. That is when UPS reports Q1 2026 results, and the domestic operating margin line will either validate the turnaround thesis or push it back another quarter.

The Q4 2025 result gave bulls something to work with. As detailed in UPS’s Q4 2025 earnings press release, the company closed 195 operations, including 93 buildings, removed 26.9 million labor hours, and cut 48,000 operational positions in 2025, delivering $3.5 billion in total savings.

Domestic revenue per piece still grew 8.3% in the quarter, and non-GAAP adjusted operating margin came in at 10.2%, ahead of internal targets, even as volume fell. The stock dropped 3.26% on the reporting day after management guided 2026 full-year revenue to approximately $89.7 billion and non-GAAP adjusted operating margin to approximately 9.6%, confirming the first half would be a headwind before improvement arrived in the second half.

“Looking ahead, upon completion of the Amazon glide-down, 2026 will be an inflection point in the execution of our strategy to deliver growth and sustained margin expansion,” said Carol Tomé, UPS Chief Executive Officer.

One week ago, UPS added a fresh operational catalyst. The company announced a full nationwide RFID rollout, deploying radio frequency identification (RFID) sensing, a technology that replaces manual barcode scanning with automatic package tracking, across every U.S. delivery vehicle, facility, and more than 5,500 UPS Store locations.

The rollout, backed by more than $100 million in investment, eliminates nearly 20 million manual scans daily and makes UPS the first major logistics provider to deploy RFID at this scale. The stock has moved higher in each session since.

See historical and forward estimates for UPS stock (It’s free!) >>>

Is UPS Undervalued Today?

At $107.11, UPS trades at 9.24x NTM EV/EBITDA and 15.29x NTM P/E. Those are near the low end of its recent range, which tells you the market is pricing the stock close to the trough. The key question is whether trough valuation is the right entry point or a value trap.

The peer comparison is instructive. FedEx trades at 11.05x NTM EV/EBITDA, a nearly two-turn premium to UPS’s 9.24x. Deutsche Post trades at 6.95x, a discount that reflects its more international, lower-margin mix.

UPS sitting below FedEx is not unusual, but the gap is wider than historical norms and reflects investor preference for FedEx’s cleaner near-term margin story, particularly ahead of the FedEx Freight spin-off.

The question is whether UPS closes that gap as its Amazon exit clears and margin recovery becomes visible in reported numbers.

Wall Street is evenly split. There are 13 Buys, 14 Holds, 2 Underperforms, and 1 Sell across 30 analysts, with a mean target of $112.64, only about 5% above where the stock trades today. The high target of $135 prices in a clean second-half recovery, the low of $75 prices in a prolonged tariff disruption, and a dividend that cannot be sustained at a 96.9% payout ratio.

The long-term thesis rests on UPS deliberately trading lower-margin freight for higher-margin work. The volume being exited is Amazon’s short-haul residential parcel business, which Amazon now handles itself.

What stays is stickier: UPS’s healthcare logistics push, accelerated by the $1.6 billion acquisition of Andlauer Healthcare Group in November 2025, targets approximately $20 billion in healthcare revenue by late 2026.

As CFO Brian Dykes said on the Q4 2025 call, “Healthcare, high-value goods, complex supply chains are really sticky. When you’re 99.99% on-time delivery for clinical trial drugs, they don’t care if you put a 5% price increase through.” That is the margin profile UPS is building toward.

The risk is execution timing. The 2026 first half faces transition headwinds from the Amazon glide-down, additional facility closures, and 30,000 planned job reductions, all of which are facing an active Teamsters legal challenge. If any of those slip by a quarter, the recovery narrative gets pushed out, and the dividend durability question, anchored by that 96.9% payout ratio, becomes the dominant story.

See how UPS performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $107.11

- Target Price (Mid): ~$175

- Potential Total Return: ~64%

- Annualized IRR: ~11% / year

See analysts’ growth forecasts and price targets for UPS stock (It’s free!) >>>

The TIKR mid-case target of approximately $175 by December 31, 2030 is built on around 4% annualized revenue growth, led by healthcare logistics expansion and small business volume recovery, and net income margin recovering to around 8%, up from 7.3% in 2025, as workforce reductions and a leaner network reduce fixed cost per unit over time.

The upside requires the Amazon transition to close cleanly by June, Teamsters negotiations to proceed without court disruptions, and the RFID investment to translate into measurable customer retention and lower operational error rates. The downside is a delayed recovery that stretches the payout ratio further and forces a dividend conversation rather than a margin expansion story.

At ~11% annualized IRR through 2030, the model rewards patience. The 6.1% dividend yield compensates investors while they wait, provided the payout holds.

Conclusion

Watch the domestic operating margin in UPS’s Q1 2026 results on April 28. If it holds relatively flat against volume declines, the H2 recovery thesis gains credibility, and the stock likely moves toward the $113 Street consensus. If it compresses materially, the first half becomes worse than guided, and the dividend sustainability question dominates. UPS is executing the right strategic pivot at real cost, trading at trough valuation with a 6.1% yield, and April 28 is the first hard data point that will tell investors whether June’s promised inflection is real.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in UPS?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up UPS, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track UPS alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!