Key Stats — Deere & Company (DE) | Q1 FY2026 Earnings

- Current price: ~$590

- Q1 FY2026 equipment operations net sales: $8B (+18% YoY)

- Q1 FY2026 total revenues: $9.6B (+13% YoY)

- Q1 FY2026 net income: $656M ($2.42 per diluted share)

- Q1 FY2026 equipment operations operating margin: ~6%

- FY2026 net income guidance: $4.5B–$5B (raised)

- FY2026 cash flow from equipment operations: $4.5B–$5.5B (raised)

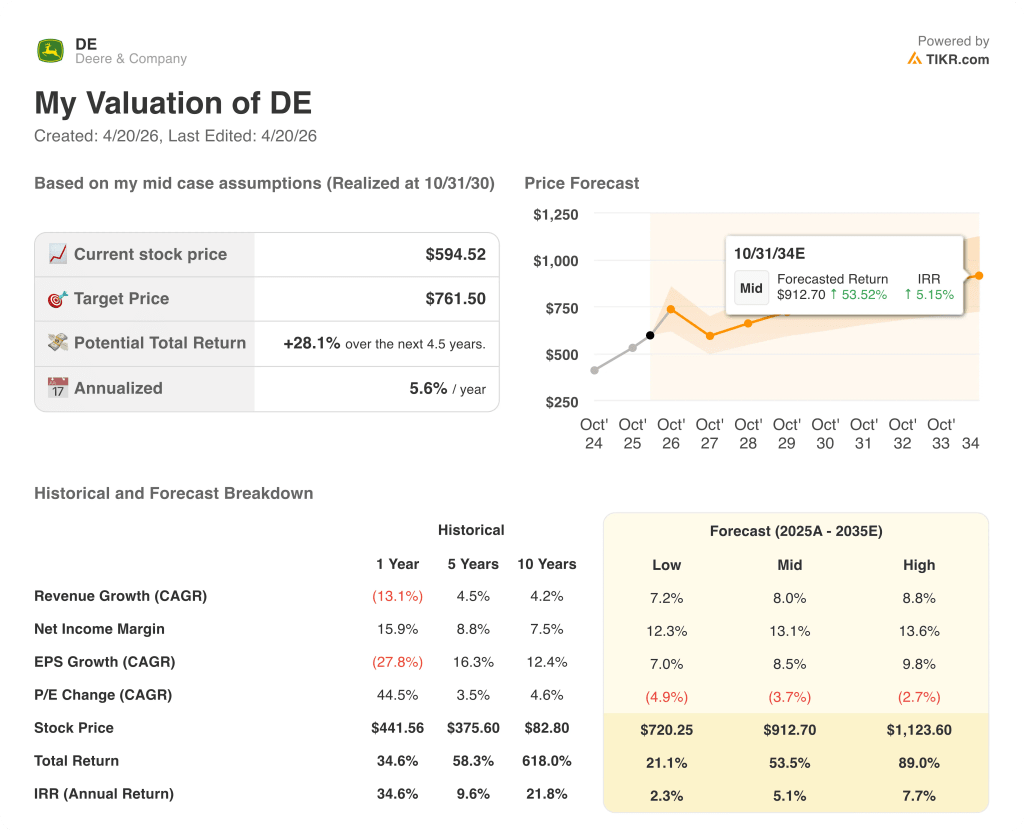

- TIKR model price target: $762

- Implied upside: ~28% total return over ~5 years (~6% annualized)

Deere Stock Beats Q1 Estimates as Construction Surges and Cycle Bottom Nears

Deere & Company (DE) stock posted equipment operations net sales of $8.0B in Q1 FY2026, up 18% year-over-year, with total revenues of $9.6B rising 13%.

Net income came in at $656M, or $2.42 per diluted share, with all three business segments executing ahead of internal forecasts.

Construction & Forestry was the standout driver, with net sales surging ~34% to $2.7B as higher shipment volumes and positive foreign currency translation boosted the top line.

C&F operating profit more than doubled year-over-year to $137M, yielding a 5.1% operating margin, as production efficiencies and favorable volumes offset the drag from higher tariffs.

According to Josh Beal, Director of Investor Relations, on the Q1 FY2026 earnings call, the C&F order bank rose by over 50% during the quarter, reaching its highest point since May 2024 and providing clear visibility into the second half of the fiscal year.

Small Ag & Turf net sales grew 24% to $2.2B, driven by higher shipment volumes and positive price realization of 2 points, with operating profit reaching $196M for a 9% margin.

Production & Precision Ag net sales rose 3% to $3.2B, with most of the gain attributable to favorable currency translation; the segment’s operating margin contracted to 4.4%, weighed down by higher tariffs, unfavorable sales mix, and elevated warranty expenses.

Financial Services contributed $244M in net income, up year-over-year on favorable financing spreads and lower provision for credit losses.

Deere raised its FY2026 net income outlook to $4.5B–$5.0B and lifted its cash flow from equipment operations guidance by $500M at both ends to a range of $4.5B–$5.5B.

The company returned ~$750M to shareholders in Q1 through dividends and share repurchases.

Tariff costs remain a full-year headwind of ~$1.2B pretax, though price and cost are expected to be roughly neutral for the year, including tariff coverage.

Deere Stock Financials: Margin Pressure Persists, But Recovery Path Is Forming

Deere stock’s Q1 income statement reflects a business running with operational discipline while absorbing tariff costs that are still compressing margins below mid-cycle norms.

Gross margin came in at around 22% in Q1 FY2026, down from 25.5% in the year-ago quarter, as tariffs, unfavorable regional mix in large agriculture, and elevated warranty costs weighed on the Production & Precision Ag segment.

Operating income was $0.89B, with an operating margin of around 9%, compared to ~11% in Q1 FY2025.

The compression continues a trend visible across the past several quarters: gross margin reached 31% as recently as Q2 FY2024 and has contracted steadily as large ag volumes declined and cost pressures built.

C&F’s operating margin recovery to 5% is a meaningful data point in the picture, as the segment’s sharply higher volumes are beginning to restore operating leverage across the equipment business.

Management guided full-year PPA margins of 11%–13%, SAT margins of 13.5%–15%, and C&F margins of 9%–11%, pointing to meaningful recovery through the back half of the fiscal year.

Is Deere Stock Still Undervalued? What the TIKR Model Shows

The TIKR model prices Deere stock at a target of $7612, implying ~28% total return over ~5 years from the current price near $590, or about 6% annualized.

The mid-case assumptions are a revenue CAGR of 8%, a net income margin of 13%, and EPS CAGR of 8.5%, all consistent with a business recovering from a cyclical trough toward a normalized earnings run rate.

The Q1 result makes the investment case incrementally stronger: all three segments beat internal plans, management raised guidance, and the C&F and small ag order book data signals a demand inflection rather than a one-quarter pull-forward.

Deere stock is not priced for a near-term earnings boom, but the TIKR model reflects a mid-cycle normalization path that this Q1 report begins to credibly support.

The central tension for Deere stock: whether the order momentum in construction and small ag translates into a sustained large agriculture recovery, or whether tariffs and soft row crop economics cap the rebound well below prior-cycle peaks.

What Has to Go Right

- Large agriculture demand in North America stabilizes at the low end of the down 15%–20% industry forecast, with tractor order velocity already extending into Q4 and combines tracking better than that range at roughly down 10%–15%

- C&F sustains its order bank growth (up 50%+ in Q1) through H2, with the CONEXPO excavator launch adding competitive differentiation in a segment that represents ~40% of the North American construction equipment market

- SAT holds its upgraded net sales guide of up 15% and margin guide of 13.5%–15%, supported by continued dairy/livestock profitability and normalizing turf demand

- Tariff mitigation on Section 232 steel progresses through the year, with management already reporting some relief and price/cost neutral as the confirmed full-year baseline

What Could Still Go Wrong

- PPA operating margin contracted sharply to 4.4% in Q1, with South America facing high interest rates, an appreciated real, and softer commodity prices that have already prompted combine inventory buildups in Brazil

- Full-year tariff exposure of ~$1.2B pretax remains elevated, and the IEEPA portion (just under half of total) is subject to ongoing Supreme Court proceedings and broader trade policy uncertainty

- C&F pricing was slightly negative in Q1, with price increase actions delayed as backlog built faster than anticipated; management trimmed the full-year C&F price realization guide by 0.5 point

- Global large agriculture fundamentals remain challenged, with the USDA’s 2026 net cash farm income forecast showing most of the gain driven by government payments rather than crop cash receipts

Should You Invest in Deere & Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DE stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Deere & Company alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DE stock on TIKR for Free →