Key Stats for Norfolk Southern Stock

- 52-Week Range: $217 to $320

- Current Price: $304

- Street Mean Target: $311

- Street High Target: $355

- TIKR Model Target (Dec. 2030): $352

What Happened?

Norfolk Southern Corporation (NSC) beat Wall Street’s Q4 2025 earnings estimate by nearly $0.50 per share, and Norfolk Southern stock barely moved.

Adjusted EPS for the quarter came in at $3.22, well ahead of the $2.76 consensus estimate, driven by $216 million in full-year productivity savings and the best safety performance the company has delivered in over a decade.

Revenue of $3 billion met estimates exactly, but total railway volumes fell 4% year-over-year as weak intermodal demand and depressed export coal markets offset record strength in merchandise and automotive freight.

Full-year 2025 free cash flow surged to $2.2 billion, an increase of nearly $500 million over the prior year, reaching the highest conversion rate since 2021.

The productivity story is the one the headline metrics have obscured. Norfolk Southern moved 3% more gross ton miles in 2025 with 4% fewer employees, a 7% headcount productivity improvement, while fuel efficiency improved 5% as the company’s locomotive conversion from DC to AC technology crossed 70% of the active fleet.

Zero reportable mainline derailments in Q4, a 31% improvement in the FRA accident rate for the full year, and an adjusted operating ratio of 65.8% collectively describe a railroad executing at a level its market price does not reflect.

CEO Mark George offered a characteristically candid note from the Q4 2025 earnings call: “As we move through 2026, the demand environment remains unclear.”

What is not unclear is the cost structure. The company raised its 2026 cost-takeout savings commitment from $100 million to $150 million, building on the $500 million already delivered over the prior two years, while cutting the capital budget by a further $300 million to $1.9 billion.

Overlaying the standalone story is the proposed combination with Union Pacific, a transaction that would create the first transcontinental freight railroad in the United States and give shippers single-line access to over 100 ports and 10 cross-border gateways.

The deal terms set cash consideration at $88.82 per Norfolk Southern stock share plus one Union Pacific common share, establishing a hard transaction floor above the current trading price when UNP is factored at current levels.

The Surface Transportation Board sent back the initial merger application in January as procedurally incomplete, not on merits, and the companies plan to file a revised application by April 30, with a close targeted for the first half of 2027.

That regulatory timeline means Norfolk Southern stock is trading with full merger uncertainty baked in but without full merger credit, a gap the hold-heavy analyst consensus has declined to close.

The near-term headwind is real: competitor responses to the merger announcement are already creating approximately 1% of revenue drag in 2026, and Q1 intermodal volumes are tracking roughly 6% below year-ago levels.

But the April 24 earnings call delivers the first hard data on whether cost discipline and merchandise momentum can hold through that pressure, and any substantive update on the April 30 STB refiling adds a binary catalyst the market is not pricing.

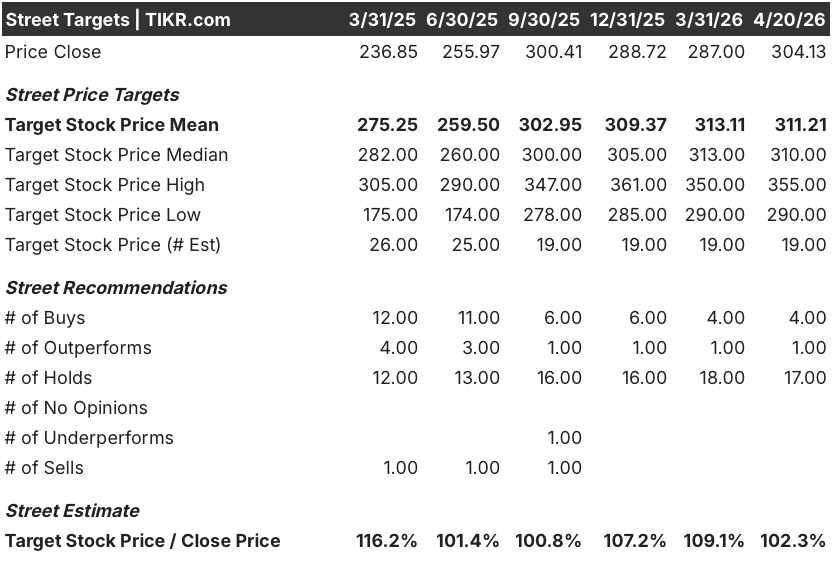

Wall Street’s Take on NSC Stock

The Q4 earnings beat did not shift conviction. Norfolk Southern stock carries one of the most hold-heavy analyst profiles in the railroad sector, and the consensus structure reflects a market waiting rather than acting.

Norfolk Southern stock’s adjusted EPS of $11.85 for full-year 2025 demonstrated that cost discipline can compound earnings even when top-line growth stalls, and with productivity compounding expected to deliver around $150 million more in 2026, the earnings floor looks better-supported than the hold-heavy consensus implies.

With 4 buys, 1 outperform, and 17 holds across 19 analysts, the Street is not bearish on Norfolk Southern stock: it is anchored to a mean price target of around $311 that implies just 2.3% upside, while the Union Pacific deal terms sit above current price levels and carry timeline optionality the consensus has not repriced.

The $355 bull target reflects full merger execution credit; the $290 floor essentially prices in a deal collapse and a standalone re-rating lower, a spread that is less about fundamental disagreement on the railroad’s quality and more about binary outcome distribution on regulatory approval.

Trading at roughly 26x forward normalized EPS against a backdrop of compounding productivity delivery and deal-floor support at current levels, Norfolk Southern stock appears undervalued relative to a market that has priced in the merger uncertainty without pricing in the merger optionality.

The risk is intermodal attrition: if competitive losses tied to the merger announcement accelerate beyond the guided 1% revenue headwind in 2026, the standalone earnings bridge to deal close compresses and the margin between current price and transaction value narrows.

The catalyst is the April 24 Q1 2026 earnings call: merchandise volume momentum and operating ratio trajectory will determine whether standalone execution holds through the uncertainty window, while any clarity on the April 30 STB refiling status adds deal-close optionality the current price does not include.

What Does the Valuation Model Say?

TIKR’s mid-case model prices Norfolk Southern at around $352, implying roughly 16% total return from the current price of $304 and an annualized IRR of around 3%, anchored to a mid-case EPS CAGR of around 4% through 2030 and net income margins expanding toward around 24%.

That standalone return profile understates the actual investment case: the Union Pacific deal terms implying roughly $319 in combined cash and stock value per NSC share create a floor above the TIKR mid-case target, which means Norfolk Southern stock is undervalued relative to either the transaction economics already on the table or the quality of the standalone railroad the market is discounting through merger-related noise.

The argument for owning NSC today resolves to one question: whether the merger closes or the standalone railroad re-rates, and at $304, both paths carry upside. The risk is the path where neither happens fast enough to matter.

The Standalone Case: Cost Discipline Has Already Done the Work

- Q4 2025 adjusted EPS of $3.22 beat the $2.76 consensus estimate by 17%, driven by $216 million in productivity savings that surpassed the original $200 million target raised mid-year.

- The 3-year cumulative cost-takeout total stands at roughly $650 million, with around $150 million more targeted in 2026, compounding an earnings floor independent of volume recovery.

- FY2025 FCF of $2.2 billion, up nearly $500 million year-over-year, at the highest conversion rate since 2021, creates balance sheet flexibility through the deal uncertainty window.

- Zero reportable mainline derailments in Q4 2025 and a 31% improvement in the FRA accident rate confirm the safety and service foundation required for any growth scenario, merger or standalone.

The Merger Optionality Case: The Floor Is Real

- Deal terms set cash consideration at $88.82 per NSC share plus one Union Pacific common share, establishing a hard transaction floor that compares directly to NSC’s 52-week low of $217.33 and the current price of $304 when UNP trades near recent levels.

- The STB’s return of the initial application was a procedural completeness determination, not a merits denial; UP CEO Jim Vena confirmed deal timing and both companies plan a revised filing by April 30.

- CEO Mark George described the integration as clicking “the Lego set together,” with joint integration planning and cultural alignment already underway across both organizations.

- A combined transcontinental network addresses what George identified as the primary structural barrier to U.S. rail volume growth: the geographic split at the Mississippi River that forces interchanges and kills the single-line service advantage that captures freight from trucking.

- Opposition from BNSF, CSX, and other Class I railroads signals that the deal’s competitive disruption potential is real, which is a case for, not against, long-term earnings accretion for NSC shareholders.

Should You Invest in Norfolk Southern Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up NSC stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Norfolk Southern Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze NSC stock on TIKR for Free →