Key Stats for Vulcan Materials Stock

- 52-Week Range: $237 to $331

- Current Price: $295

- Street Mean Target: $323

- Street High Target: $365

- TIKR Model Target (Dec. 2030): $547

What Happened?

Vulcan Materials Company (VMC) — the largest producer of construction aggregates in the United States — delivered a Q4 2025 earnings report that missed Wall Street estimates on every headline metric, then used its March 12 Investor Day to explain why Vulcan Materials stock is worth more than that miss suggests.

Fourth-quarter revenue came in at $1.91 billion against a consensus estimate of $1.96 billion, and adjusted EPS landed at $1.70, well below the $2.11 analysts had expected.

Weak residential construction was the primary drag, as elevated mortgage rates continued to suppress housing starts and new project launches across Vulcan’s 23-state footprint.

Vulcan Materials stock fell more than 7% in premarket trading after the report, a reaction that reflected the headline gap but not the operational reality underneath it.

Full-year 2025 operating cash flow surged 29% to $1.8 billion, and free cash flow surpassed $1.1 billion — more than double the level from three years prior.

The number that reframes the narrative is $11.33: Vulcan’s aggregates cash gross profit per ton for 2025, a 45% improvement since 2022 and the achievement of a target the company originally expected to reach on 260 million to 270 million tons of shipments.

Vulcan shipped just 227 million tons.

That gap is the thesis. The company extracted more profitability per unit than the original model required, which means the demand recovery still ahead arrives as pure operating leverage on a cost structure already proven.

At its Investor Day in New York City, CEO Ronnie Pruitt set the next target: $20 of aggregates cash gross profit per ton on those same 260 million to 270 million tons, implying adjusted EBITDA of $4.5 billion to $5 billion — roughly double where the company stands today.

Pruitt framed the demand assumptions conservatively: “We’re not talking about double-digit growth that we need to get there.”

The cost discipline behind that confidence runs through two proprietary platforms. The Vulcan Way of Operating, centered on a process intelligence system now deployed across 75% of aggregate production, delivered less than 1% year-over-year production cost increases at PI-enabled plants in 2025, versus 2.6% at plants without the technology — a spread that compounds directly into per-ton profitability as volume grows.

On the commercial side, the Vulcan Way of Selling platform followed up on over 14,000 jobs, converted 38,000 quotes to orders, and processed more than $2 billion in customer portal payments in 2025, producing aggregate price growth that outpaced both peers and the broader industry.

Three tailwinds support demand recovery through the multi-year forecast window: IIJA infrastructure funding with roughly 50% still unspent provides public construction visibility well into 2027; data center construction is converting from quote to shipment in 2 to 3 months versus the historical 6-month lag, accelerating near-term aggregate intensity; and Vulcan’s footprint is concentrated in 35 of the 50 fastest-growing metropolitan statistical areas in the country, where population and employment growth structurally outpace national averages.

Vulcan also raised its quarterly dividend 6% to $0.52 per share, signaling balance sheet confidence with net leverage sitting at 1.8x inside the company’s 2x to 2.5x target range.

The setup heading into Q1 2026 is a business with the strongest per-ton economics in its history, a conservative demand recovery thesis, and a stock trading at a level that prices in the Q4 miss rather than the operational step-change underneath it.

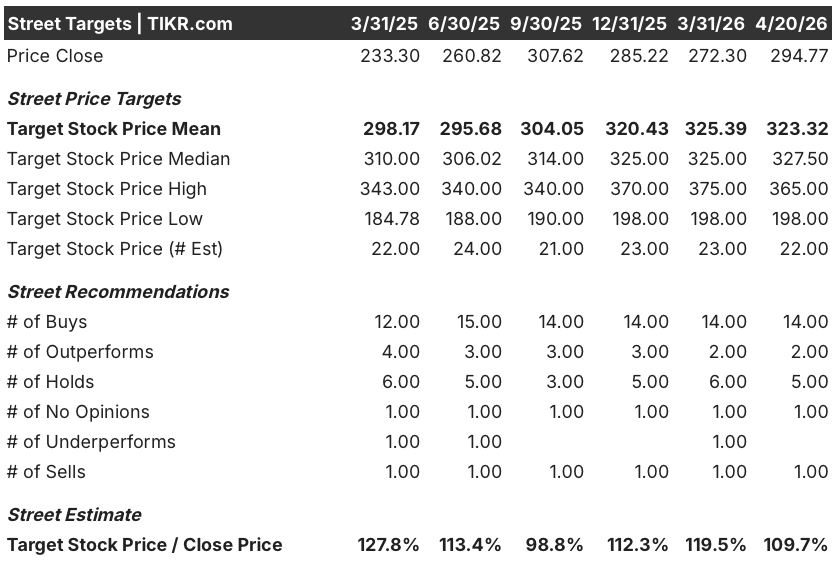

Wall Street’s Take on VMC Stock

The Q4 miss sent VMC lower, but the underlying thesis has not changed: this is a structurally more profitable aggregates business than the market was modeling three years ago, and the demand environment that constrained it is beginning to turn.

Consensus EBITDA for 2026 is around $2.48 billion, growing to around $2.76 billion in 2027 — a compounding trajectory that prices in none of the $4.5 billion to $5 billion long-range target, which means the market is not yet paying for execution that has already been demonstrated on far fewer tons than anyone expected.

With 14 buys, 2 outperforms, 5 holds, and 1 sell across 22 analysts, the Street holds strong conviction on Vulcan Materials stock, and a mean price target of around $323 implies roughly 9% upside from current levels, with the bull end of the range reaching $365 on full execution of the Investor Day roadmap.

The bear camp anchors near $198, pricing in a prolonged demand stall and no material progress toward $20 per ton; the $365 bull camp prices in Investor Day execution plus a resumption of residential construction activity — two scenarios whose probability weights look asymmetric given IIJA tailwinds and the process intelligence cost advantage already in the numbers.

Priced at a meaningful discount to what the EBITDA compounding trajectory and $20/ton target imply for intrinsic value, Vulcan Materials stock appears undervalued against a backdrop of improving public construction demand and an operational cost structure that has already outperformed its own assumptions.

The risk is timing: residential construction remains suppressed, and if private-sector recovery runs materially later than the 2026-2027 window embedded in consensus, the path to 260 million tons extends along with the EBITDA growth timeline.

The catalyst is the Q1 2026 earnings call, scheduled for early May: shipment volume tracking to the guided 1% to 3% growth range will confirm the demand recovery thesis is on schedule, while any shortfall invites a reassessment of when the EBITDA inflection arrives.

What Does the Valuation Model Say?

TIKR’s mid-case model prices Vulcan Materials at around $547, implying roughly 86% total return from the current price of $295 and an annualized IRR of around 14%, driven by a mid-case EPS CAGR of around 10% through 2030 paired with net income margins expanding toward around 21%.

Against a company that has already demonstrated the cost discipline and pricing power required to sustain that compounding — delivering the original $11 to $12 per ton target on 33 million fewer tons than the model assumed — Vulcan Materials stock is undervalued at a price that reflects the Q4 miss more than it reflects the structural earnings engine underneath it.

The central tension is whether volume recovers fast enough to meet the time horizon the model assumes. Vulcan has proven it can expand per-ton profitability through muted demand; reaching $4.5 billion to $5 billion in EBITDA still requires shipment tons to grow from 227 million toward 260 million to 270 million, and that growth depends on construction cycles that are not fully in management’s control. The 2026 guidance for 1% to 3% shipment growth is the first data point that will confirm or challenge the compounding timeline.

Bull Case: Execution Meets Recovery

- Process intelligence deployed across 75% of production delivered sub-1% production cost growth in 2025 versus 2.6% at non-PI plants, a structural cost advantage that widens as volume grows and operating leverage kicks in.

- IIJA contract awards at record levels with roughly 50% of funding still unspent, providing public construction visibility through 2027 and into 2028 before any reauthorization debate becomes a material headwind.

- Data center projects are converting from quote to shipment in 2 to 3 months versus the historical 6-month lag, adding near-term aggregate intensity ahead of what guidance assumes; Vulcan cited one Meta facility project alone at 600,000 tons of shipments.

- Free cash flow surpassed $1.1 billion in 2025, more than double three years earlier, funding an M&A pipeline targeting 350 million annual identified-candidate tons — adding volume upside outside of organic demand recovery.

- The 2026 EBITDA guidance midpoint of around $2.5 billion and the forward consensus trajectory toward around $2.76 billion by 2027 represent a compounding base that reaches $4.5 billion well before requiring heroic demand assumptions.

Bear Case: Volume Timeline Slips

- Q4 2025 adjusted EPS of $1.70 missed the $2.11 consensus estimate by 19%, confirming that weak residential starts create real near-term earnings volatility independent of operational execution quality.

- Housing starts have failed to keep pace with household formations in 3 of the last 5 years; a persistent rate environment could push residential recovery past 2027, extending the timeline to 260 million tons materially beyond the model’s base case.

- The $20/ton target carries no fixed year, meaning the approximately 4.7-year horizon in TIKR’s mid-case model is not a company commitment; if unit profitability compounding moderates from its recent 13% CAGR, the $547 implied price is farther out than the model projects.

- Competitor adoption of operational technology similar to process intelligence could gradually compress the per-ton cost and pricing advantages that currently anchor Vulcan’s leadership position in aggregates pricing.

Should You Invest in Vulcan Materials Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up VMC stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Vulcan Materials Company alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze VMC stock on TIKR for Free →