Key Stats for TransDigm Stock

- Current Price: ~$1,206

- Q1 FY2026 Revenue: $2,285M, +14% YoY

- Q1 FY2026 Adjusted EPS: guidance midpoint raised to $38.38 for full year

- Q1 FY2026 Organic Growth: ~7%

- Full-Year FY2026 Revenue Guidance (midpoint): $9.94B, +~13% YoY

- Full-Year FY2026 EBITDA As Defined Guidance (midpoint): $5.21B, +~9% YoY; ~52% margin

- Full-Year FY2026 Adjusted EPS Guidance (midpoint): $38.38

- TIKR Model Price Target: ~$1,892

- Implied Upside: ~57%

TransDigm Stock Q1 FY2026 Earnings Breakdown

TransDigm stock (TDG) opened fiscal 2026 with Q1 revenue of $2,285M, up 14% year-over-year, and promptly raised full-year sales and EBITDA guidance on the back of results that ran ahead of internal expectations.

Organic growth came in at around 7% for the quarter, with all three market channels contributing: commercial OEM up approximately 17% on a pro forma basis, commercial aftermarket up approximately 7%, and defense up approximately 7%.

Commercial OEM was the standout on the top line, with Boeing and Airbus production ramp-ups driving growth and the prior-year period providing a favorable comparison after Boeing’s production disruptions in late 2024.

Commercial aftermarket grew 7% overall, though commercial transport aftermarket, which excludes the business jet submarket, came in at 8%, with solid contributions across freight, interiors, engine, and passenger submarkets.

CEO Mike Lisman noted on the Q1 earnings call that distributor inventory destocking created a headwind of a couple of percentage points on aftermarket revenue in Q1, but that the dynamic is expected to shift from a drag to a tailwind as the year progresses.

Defense revenue grew approximately 7%, supported by new business wins across domestic and international markets, with bookings running ahead of expectations and significantly outpacing sales.

EBITDA As Defined margin came in at 52.4%, which includes approximately 200 basis points of dilution from recent acquisitions. Lisman stated the margin performance in the base businesses improved more than expected in Q1.

Management raised the full-year revenue guidance midpoint by $90M and the EBITDA As Defined guidance midpoint by $60M, bringing the revenue midpoint to $9.94B and EBITDA midpoint to $5.21B.

Full-year adjusted EPS guidance midpoint was raised to $38.38.

On capital allocation, TransDigm announced three pending acquisitions during the quarter: Stellant Systems for approximately $960M and Jet Parts Engineering plus Victor Sierra Aviation together for approximately $2.2B, adding roughly $580M of combined 2025 revenue across the three businesses.

TransDigm stock also repurchased just over $100M of common stock opportunistically during Q1 when the share price dipped.

Free cash flow for Q1 was just under $900M, with full-year free cash flow guidance unchanged at approximately $2.4B.

TransDigm Stock: What the Financials Show

TransDigm stock’s income statement is a study in structural margin durability: the company absorbed acquisition dilution, a lower-margin commercial OEM mix, and distributor channel headwinds in Q1 while still printing at around 46% operating margin.

Gross margin was 59.2% in Q1 FY2026 (period ending 12/27/25), down modestly from the 60.3% posted in Q3 FY2025 but consistent with the 59% to 61% band that has persisted across all eight quarters in the income statement.

Gross profit grew about 10% year-over-year to $1,352M, a deceleration from the ~16% gross profit growth posted in Q3 FY2025, reflecting the acquisition dilution and OEM mix pressure Lisman flagged.

Operating income was $1,042M in the most recent quarter, up 7.0% year-over-year, against a Q1 FY2025 comp of $997M.

Operating margin came in at 45.6%, down from 47.6% in the prior quarter and down from 46.4% in Q1 FY2025, continuing a modest compression trend as OEM mix and acquisition dilution work their way through the income statement.

The operating margin trajectory across the trailing four quarters: 46.4%, 46.8%, 47.6%, 45.6% — a step down in the most recent period that is consistent with management’s own disclosure of acquisition-related dilution.

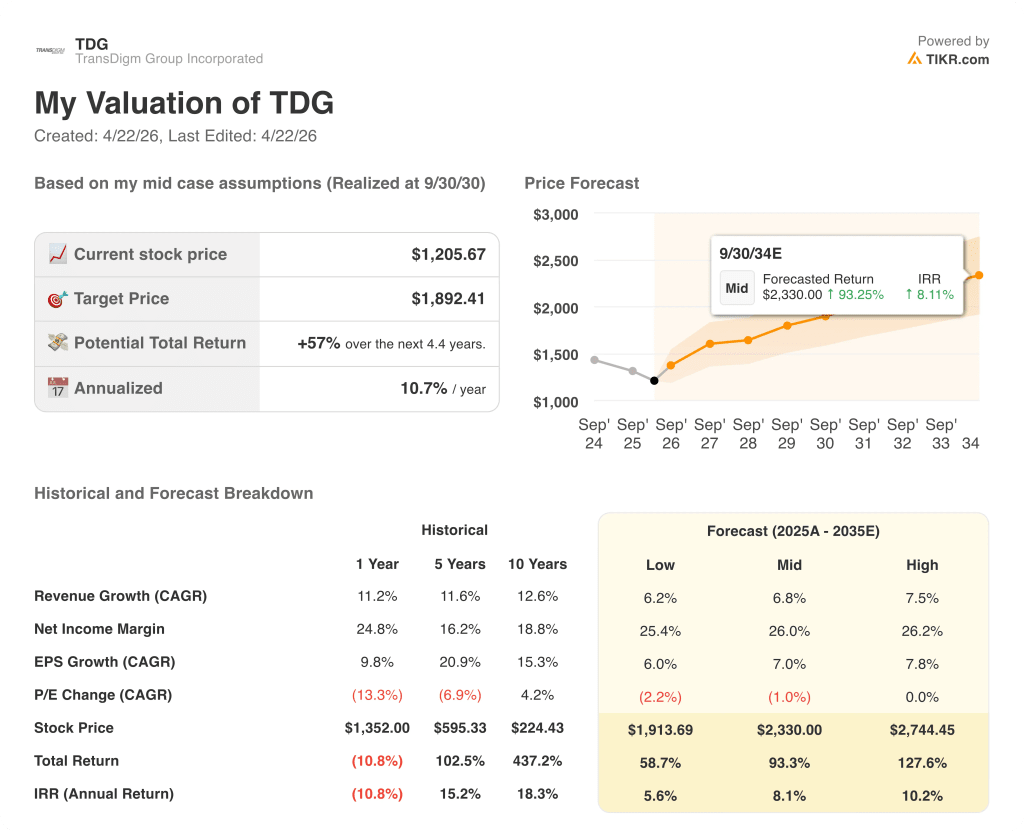

What Does the Valuation Model Say?

The TIKR model prices TransDigm stock at approximately $1,892, implying roughly 57% upside from the current price near $1,206, with an annualized IRR of about 11% over the next 4.4 years in the mid-case.

The mid-case model assumes a revenue CAGR of 6.8% and a net income margin of 26%, representing a step up from the 24.8% net income margin TransDigm delivered over the trailing one-year period and broadly in line with the 18.8% ten-year historical average as profitability has expanded.

The Q1 report reinforces the investment case: raised guidance in the first quarter, margin performance ahead of internal expectations, and bookings running ahead of sales across all three market channels are exactly the inputs the model needs to stay on the mid-to-high case trajectory.

The risk to the thesis is not operational. It is valuation: TransDigm stock has de-rated from $1,352 a year ago to $1,206 today, and the model’s mid-case IRR of 8.1% assumes P/E multiples compress slightly over the forecast period, meaning the return depends almost entirely on earnings growth rather than re-rating.

With a 57% implied upside and a business that just raised guidance after one quarter, TransDigm stock looks attractively positioned for investors willing to hold through the near-term acquisition digestion period.

The central tension this earnings report creates: TransDigm delivered above-expectation Q1 results and raised full-year guidance, yet the stock fell 5.4% on the day of the report, and the question is whether $3.2B in pending acquisitions and a 57% upside gap to TIKR’s target finally unlock a re-rating or extend the overhang.

Bull Case

- Commercial OEM grew 17% pro forma in Q1 and management’s full-year guide of high single-digit to mid-teens growth appears conservative given the bookings outpacing sales and Boeing and Airbus actively ramping production rates

- Base business margins improved more than expected in Q1 at ~52% EBITDA As Defined, with Lisman explicitly acknowledging conservatism in the full-year margin guide, creating room for upside as commercial OEM mix normalizes

- Defense bookings were robust in Q1, running ahead of expectations and significantly outpacing sales, supporting the unchanged mid-to-high single-digit defense growth guide and building a backlog that de-risks the back half of fiscal 2026

- The three pending acquisitions (Stellant, Jet Parts, Victor Sierra) add approximately $580M of 2025 revenue at a targeted 20% IRR, and TransDigm’s track record of margin expansion post-acquisition suggests the 200 basis point dilution from recent deals is temporary, not structural

Bear Case

- Commercial aftermarket grew only 7% against a market that is running 5 to 6 percentage points faster, and distributor destocking that pressured Q1 by a couple of percentage points has not yet fully resolved, creating uncertainty around the pace of the expected channel tailwind

- The $3.2B in pending acquisitions will be funded through a combination of cash and new debt on a balance sheet already at 5.7x net debt-to-EBITDA, and the three new operating units were explicitly modeled at margins well below TransDigm’s current 52% EBITDA level, adding dilution on top of existing dilution

- Business jet aftermarket came in at approximately 1% growth in Q1, well below the broader commercial aftermarket rate, and with biz jet representing a meaningful submarket within commercial aftermarket, continued softness there caps near-term CAM upside

- The stock’s 10.8% negative one-year total return signals the market is pricing in execution risk on the OEM ramp and acquisition integration simultaneously, and the full-year EPS guide of $38.38 at the midpoint assumes no incremental contribution from acquisitions that have not yet closed

Should You Invest in TransDigm Group Incorporated?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up TDG stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track TransDigm Group Incorporated alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze TDG stock on TIKR for Free →