Key Takeaways:

- Shopify is still growing quickly, but the stock has been pressured because investors are debating whether AI will disrupt software platforms or expand e-commerce’s total addressable market. Reuters reported that Shopify slid 6.5% on April 9 as software names sold off on renewed AI disruption fears.

- The business fundamentals remain strong. Revenue rose 30.1% to $11.6 billion in 2025, operating margin reached 16.4%, and free cash flow climbed to $2.0 billion, while Shopify still held $6.6 billion in net cash.

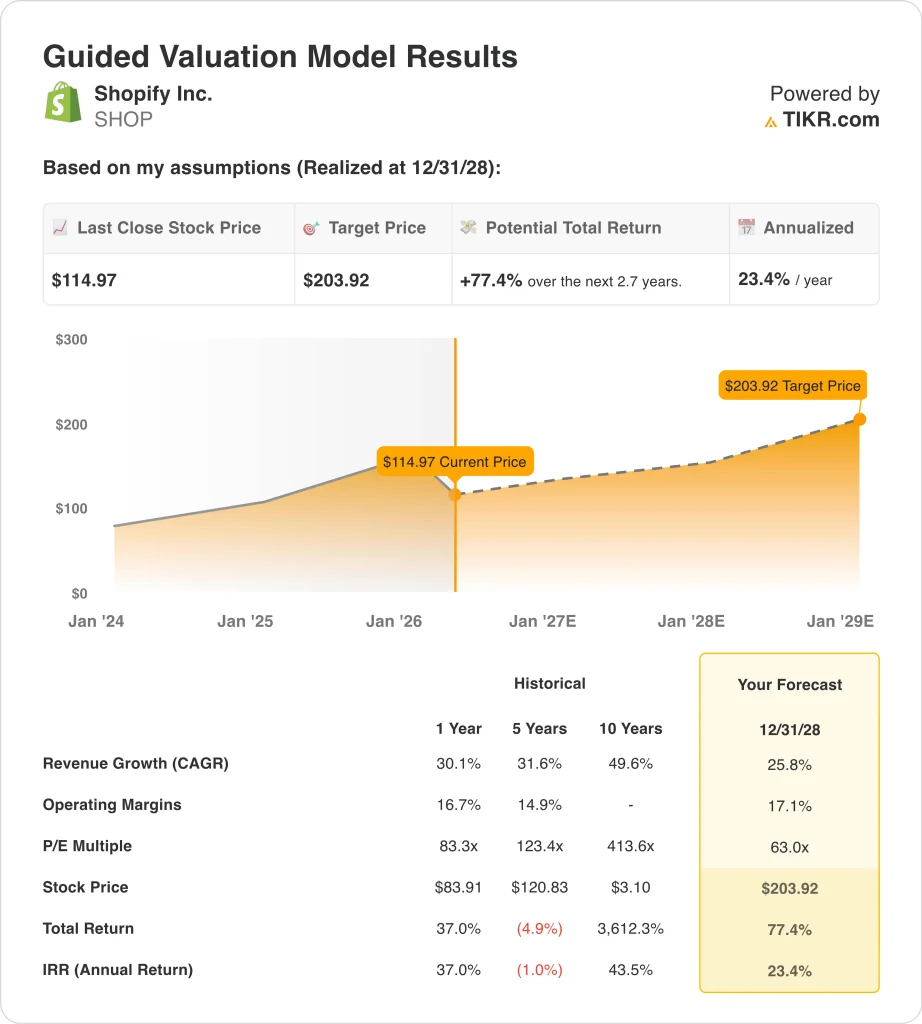

- Shopify stock could reasonably reach $204 per share by December 2028, based on our valuation assumptions.

- This implies a total return of 77.4% from today’s price of $115, with an annualized return of 23.4% over the next 2.7 years.

What Happened?

Shopify (SHOP) is relevant right now because the market is trying to decide whether AI is a threat to software companies or a new growth engine for commerce. That debate has hit Shopify especially hard because it sits between merchants, payments, search, and online storefronts. The stock is down 31.3% over the past three months, even after closing at $115 on April 13.

The biggest recent earnings event came on February 11. Shopify reported fourth-quarter revenue growth of 31%, guided for first-quarter revenue to grow at a low-thirties rate, and authorized a $2 billion share repurchase program.

Even so, Reuters said the stock fell because adjusted earnings missed estimates and the company forecast a lower free cash flow margin as it kept investing in AI, international expansion, and marketing.

Since then, investors have focused on what AI means for Shopify’s moat. On March 3, Reuters reported that Shopify’s president said agentic commerce could increase e-commerce’s total addressable market, and on March 25, Reuters reported that Shopify merchants could sell to ChatGPT users through agentic storefronts.

That story is why the stock has moved both with company news and with broader software sentiment. Reuters reported that Canadian tech shares, including Shopify, were hit in early April by renewed fears that rapid AI progress could pressure software business models.

Here’s why Shopify stock could stay volatile from here: investors want proof that AI tools like Sidekick, Catalog, and agentic storefronts can deepen merchant adoption faster than AI changes buyer behavior.

What the Model Says for SHOP Stock

We analyzed the upside potential for Shopify stock using valuation assumptions based on rapid revenue growth, expanding profitability, and the company’s position as a core commerce platform for merchants of all sizes.

Based on estimates of 25.8% annual revenue growth, 17.1% operating margins, and a normalized P/E multiple of 63.0x, the model projects Shopify stock could rise from $115 to $204 per share.

That would be a 77.4% total return, or a 23.4% annualized return over the next 2.7 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for SHOP stock:

1. Revenue Growth: 25.8%

Shopify’s top-line growth has remained exceptional. Revenue rose from $4.6 billion in 2021 to $11.6 billion in 2025, and 2025 revenue growth accelerated to 30.1% from 25.8% in 2024. That is one reason the market still treats Shopify as a premium growth business.

The latest quarter reinforced that story. Shopify said Q4 revenue grew 31%, while CFO Jeff Hoffmeister said the company closed 2025 with “strong top-line growth and disciplined cash generation.” Management also guided for first-quarter 2026 revenue to grow at a low-thirties percentage rate, similar to Q4 2025.

Based on analysts’ consensus estimates, we use a 25.8% revenue growth forecast. That matches the valuation model and sits below Shopify’s 30.1% growth in 2025, so it does not require acceleration from already strong levels. It reflects continued gains in merchant solutions, payments penetration, and AI-assisted commerce tools.

2. Operating Margins: 17.1%

Margins have improved sharply as Shopify has scaled. Operating margin moved from 3.7% in 2023 to 14.0% in 2024 and then to 16.4% in 2025. Free cash flow margin also reached 17.4% in 2025, which shows stronger operating discipline alongside growth.

Management has been clear that it is still investing. Reuters reported that profitability was pressured by spending on international expansion, AI, and marketing, and Shopify’s first-quarter outlook called for operating expenses to be 37% to 38% of revenue. That helps explain why the stock sold off after earnings despite the strong revenue guide.

Based on analysts’ consensus estimates, we use 17.1% operating margins. That is only modestly above the current 16.4% level, so it assumes continued execution rather than a dramatic jump. It reflects a business that can keep gaining scale while still funding product development and go-to-market investment.

3. Exit P/E Multiple: 63x

The multiple is the part of the model that carries the most debate. Shopify’s market data shows an NTM P/E of 63.0x and an LTM P/E above 122x, while the valuation model uses 63.0x as the exit multiple. That is below the 1-year historical P/E of 83.3x in the model, but it is still far above the broader market.

That premium reflects how investors see Shopify’s role in the commerce stack. The company is benefiting from AI enthusiasm, payments growth, and rising merchant adoption, but it is also exposed to swings in software sentiment. Reuters reported that software stocks sold off in April on fears that AI could upend some business models, which is why multiple compressions remain a real risk even when fundamentals are strong.

Based on analysts’ consensus estimates, we maintain a 63.0x exit P/E multiple. That keeps the model aligned with Shopify’s current premium positioning, but it does not assume a return to the much higher multiples seen in prior years.

If growth and margins hold, the multiple can stay elevated, but if AI anxiety worsens, valuation could remain the stock’s main pressure point.

Build your own Valuation Model to value any stock (It’s free!) >>>

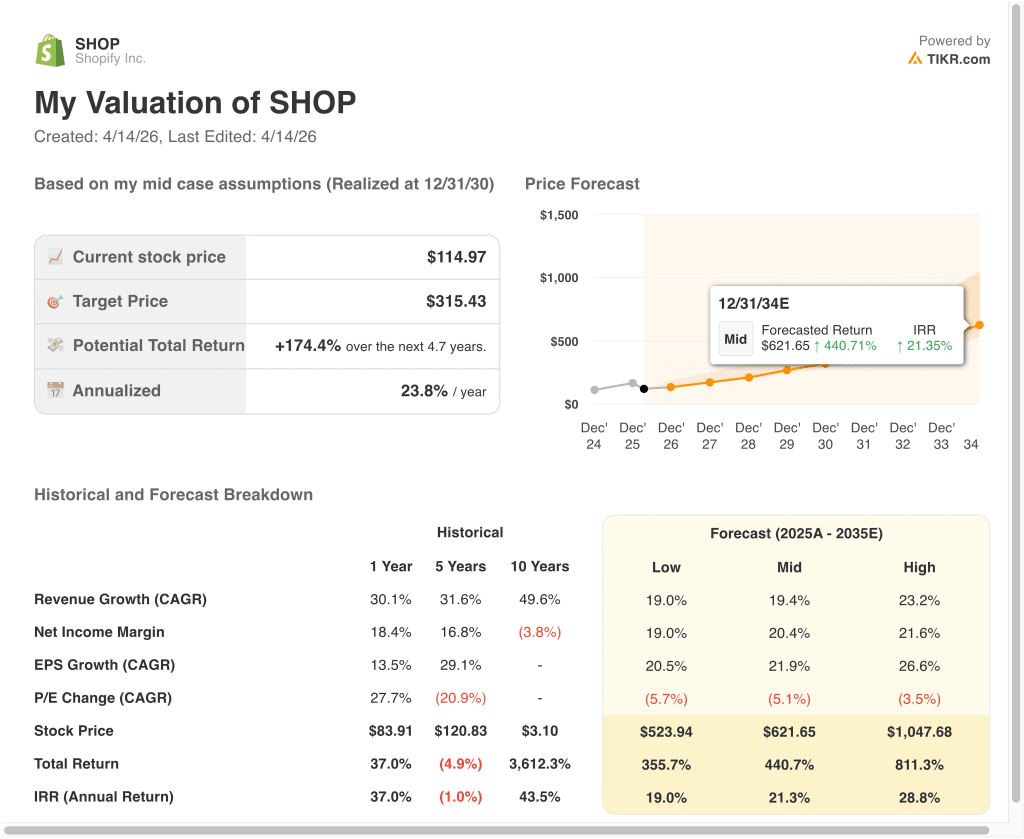

What Happens If Things Go Better or Worse?

Different scenarios for Shopify stock through 2030 show varied outcomes based on AI commerce adoption, margin execution, and valuation discipline (these are estimates, not guaranteed returns):

- Low Case: AI commerce adoption is slower, and the valuation compresses faster → 19.0% annual returns

- Mid Case: Shopify keeps expanding payments, merchant tools, and AI shopping workflows across its base → 21.3% annual returns

- High Case: Revenue, margins, and AI-driven commerce adoption remain exceptionally strong → 28.8% annual returns

The next move in the stock will likely depend on whether Shopify can keep turning AI from a market fear into a product advantage. First-quarter results on May 5 should matter because investors will want evidence that strong growth and margin discipline are both continuing.

If Shopify keeps compounding revenue while expanding its role in how merchants sell across search, chat, and payments, the stock can keep supporting a premium valuation even in a volatile software market.

See what analysts think about SHOP stock right now (Free with TIKR) >>>

Should You Invest in Shopify Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up SHOP, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track SHOP alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Shopify stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!