Key Stats for Hasbro Stock

- 52-Week Range: $50.6 to $107

- Current Price: $91.7

- Street Mean Target: $112.6

- Street High Target: $124

- TIKR Model Target (Dec. 2030): $127.2

What Happened?

Hasbro (HAS), the 160-year-old toymaker behind Play-Doh, Monopoly, and Magic: The Gathering (the flagship trading-card game), has completed one of the more consequential transformations in consumer discretionary, and Hasbro stock still hasn’t been fully repriced for it: the company’s Wizards of the Coast and Digital Gaming segment now generates nearly half of total revenue and virtually all of the operating profit.

That transformation became undeniable in Q4 2025, when the Wizards segment posted 86% revenue growth to $630 million, driven by Magic: The Gathering surging 141% on the strength of the Avatar: The Last Airbender and Final Fantasy holiday sets.

The number that makes the investment case concrete: the Wizards segment delivered a 46% full-year operating margin, producing over $1.0 billion in operating profit on $2.2 billion in revenue, a 45% revenue increase that no traditional toy company can replicate.

On March 19, Hasbro opened a 600,000-square-foot distribution center in Midway, Georgia, in partnership with logistics provider GXO, projecting approximately $8 million in annual productivity savings to support retail and direct-to-consumer fulfillment.

CEO Chris Cocks stated on the Q4 2025 earnings call that “adjusted operating profit exceeded $1.1 billion, also a record,” framing the result as confirmation that the Playing to Win strategy — Hasbro’s multi-year roadmap to evolve into a digital-first play and IP company — had moved from turnaround into sustainable growth.

Already in 2026, Lorwyn Eclipsed became the fastest-selling Magic: The Gathering IP premier set ever, surpassing Tarkir, confirming that the player growth flywheel driving 22% year-over-year growth in organized play participants through 2025 is carrying into the new year.

The growth architecture for the next three to five years rests on three specific pillars: a stacked 2026 Magic release slate including Teenage Mutant Ninja Turtles, Marvel Super Heroes, The Hobbit, and Star Trek; two self-published video games (EXODUS and WARLOCK) targeting a 2027 launch; and a newly secured Harry Potter primary toy license with Warner Bros. Discovery that begins building into fiscal 2027.

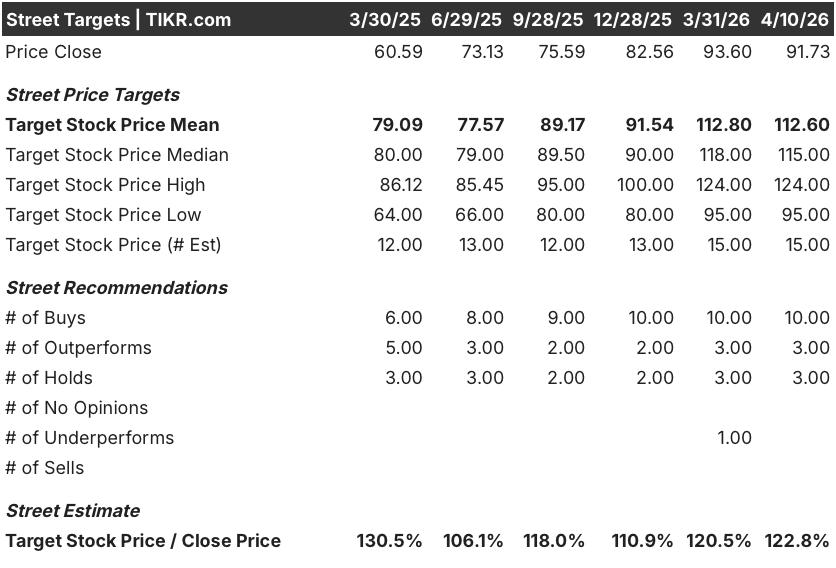

Wall Street’s Take on HAS Stock

The debate around Hasbro stock is no longer about whether the transformation worked (the fiscal 2025 numbers settled that), but whether the market has fully repriced a business that now generates record margins and record profits.

Hasbro’s normalized EPS reached $5.54 in 2025, up 38.2% year-over-year, and consensus estimates point to $5.71 in 2026 and $6.25 in 2027, the latter representing a 9.5% step-up anchored to the planned EXODUS and WARLOCK video game launches and continued Magic ecosystem expansion.

Thirteen of 16 analysts covering HAS carry buy-equivalent ratings, with a mean price target of $112.60 and a median of $115.00, implying roughly 22.8% upside from the current price, with the top of coverage reaching $124.

The spread between the $95 low target and the $124 high reflects a genuine fork: bears anchor to the Consumer Products drag and the cybersecurity incident disclosed April 1 (which took select internal systems offline and may cause order fulfillment delays for several weeks), while bulls discount those headwinds against a Magic flywheel that produced the fastest-selling IP premier set on record in Q1 2026 and a release calendar stacked with blockbuster partner IP for the rest of the year.

Priced at roughly 16x 2026 consensus EPS of $5.71, Hasbro stock appears undervalued relative to the transformation it has already executed, particularly as peers in the gamified entertainment category such as Pop Mart and Bandai Namco command forward multiples of 20x to 25x, with HAS stock entering 2026 carrying record margins, a $1 billion buyback authorization, and the Harry Potter license just beginning to layer into future revenue.

If the March 28 cybersecurity breach extends the interim operating disruption beyond the guided several-week timeframe and causes lasting damage to the spring Consumer Products order cycle, that would put real pressure on the low-single-digit revenue growth Hasbro guided for the segment in 2026.

Q2 2026 Consumer Products revenue will be the first clean read: management guided for a favorable tariff comparison to boost Q2 year-over-year, and any shortfall versus that setup would signal the operational disruption is larger than currently disclosed.

Hasbro’s Financial Performance

Hasbro’s operating income grew 40.4% in fiscal 2025 to $1.06 billion, with operating margins expanding from 18.3% to 22.6%, as Wizards segment profitability scaled faster than the cost base and Consumer Products executed a cost restructuring that nearly offset $70 million in tariff impact.

Gross margins expanded in parallel, rising from 62.8% in fiscal 2024 to 63.8% in fiscal 2025, driven by the ongoing mix shift toward the Wizards and Digital Gaming segment, where Magic card sets carry structurally higher margins than physical toy manufacturing.

The multi-year trajectory tells the operating leverage story most plainly: Hasbro stock reflects a business whose operating margins have recovered from a trough of 6.1% in fiscal 2023 to 22.6% in fiscal 2025, a 1,650 basis point expansion in two years, as transformation cost savings and Wizards scale compounded simultaneously.

What Does the Valuation Model Say?

TIKR’s mid-case valuation model prices HAS at $127.19 by December 2030, implying a 38.7% total return (7.2% annualized IRR) on revenue CAGR of 3.5% and a net income margin of 17.5%, assumptions Hasbro has already beaten in fiscal 2025 where it delivered a 16.7% net income margin on 13.7% revenue growth, meaning the model is pricing in deceleration, not continuation

HAS appears undervalued at current levels, trading at roughly 16x 2026 consensus EPS while the gamified entertainment peers Hasbro is competing for re-rating against command 20x to 25x, with the $127.19 mid-case target representing nearly 39% upside even under conservative 3.5% growth assumptions.

The investment question hinges on whether Magic’s growth rate normalizes gradually or falls sharply as 2025’s extraordinary comparable period arrives in Q4, and whether the cybersecurity disruption proves shallow or signals a deeper operational vulnerability in Consumer Products.

What Has to Go Right

- Magic: The Gathering’s 2026 Universes Beyond slate (Teenage Mutant Ninja Turtles, Marvel Super Heroes, The Hobbit, Star Trek) sustains the momentum behind over 1 million organized play participants in 2025, keeping distribution expansion in the Wizards Play Network (now over 10,000 active stores, up 20% year-over-year) on track

- EXODUS and WARLOCK launch in 2027 into the strong demand signal already generated by 100 million combined trailer views across gaming and social channels since the titles debuted at The Game Awards

- Consumer Products grows low single digits on four Disney film releases in 2026 (Toy Story 5, Mandalorian and Grogu, Spider-Man: Brand New Day, Avengers: Doomsday) and the $8 million annual productivity contribution from the new Georgia distribution center

- Harry Potter primary toy license revenues begin materializing in fiscal 2027, adding scale to the Consumer Products segment at a time when the business has already rebuilt its margin structure

What Could Go Wrong

- The April 1 cybersecurity disclosure creates order fulfillment disruptions that extend beyond several weeks into the spring shipping window, causing Consumer Products to miss its guided low-single-digit growth before the favorable Q2 tariff comparison can provide cover

- Magic: The Gathering growth decelerates sharply in Q4 2026 against its hardest comparable (141% growth in Q4 2025), creating an earnings miss that delays the valuation re-rating the stock is working to earn

- Higher interest expense from the March 2026 $400 million notes offering and approximately $60 million in estimated 2026 tariff costs pressure EPS growth below the 3.1% consensus estimate for fiscal 2026, widening the gap between operating profit growth and reported earnings per share

- The $3.3 billion in total long-term debt constrains Hasbro’s flexibility to accelerate the buyback or pursue additional IP licenses at a time when the Harry Potter and new partnership announcements are raising expectations for the Consumer Products pipeline

Should You Invest in Hasbro, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up HAS stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Hasbro, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze HAS stock on TIKR for Free →