Key Stats for Pool Corporation Stock

- 52-Week Range: $195.5 to $345

- Current Price: $213.5

- Street Mean Target: $266.1

- Street High Target: $340

- TIKR Model Target (Dec. 2030): $316.2

What Happened?

Pool Corporation (POOL), the world’s largest wholesale distributor of swimming pool supplies and equipment, is trading 38% below its 52-week high while the core business that drives the majority of its revenue keeps holding up.

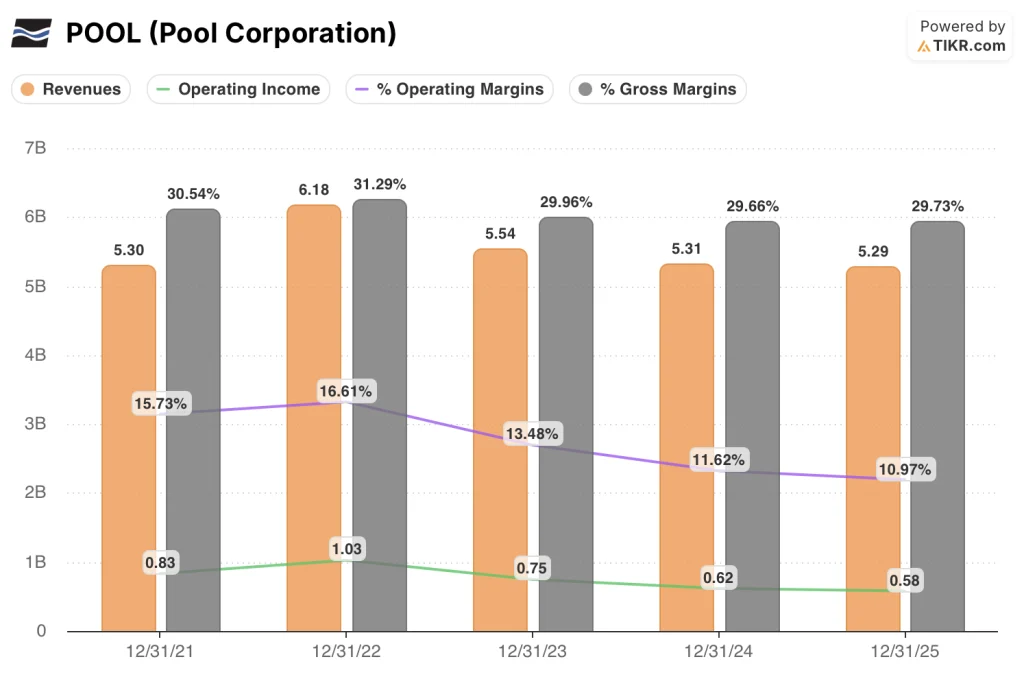

Pool Corporation stock sits at $213.51 today, a price that implies permanent damage to a franchise that generated $5.3 billion in revenue in 2025 and posted gross margins flat to the prior year.

The bear case has already been priced in. The question is whether the recovery case has been priced out too aggressively.

The Q4 2025 earnings release gave the market its latest reason to sell. Pool Corporation reported Q4 2025 revenue of $982.2 million, below Wall Street’s $999.1 million estimate, and adjusted EPS of $0.84 versus the $0.98 consensus.

Management guided full-year 2026 EPS to a $10.85 to $11.15 range, a midpoint of $11.00 that came in below the $11.62 analyst average.

Jefferies followed the print by cutting its price target to $245 from $300, maintaining a hold rating, citing no expectation of a construction or repair-and-remodel rebound in 2026.

The stock, which had already fallen 32.9% in 2025, dropped another 7.8% in premarket trading on February 20, one day after the Q4 earnings release.

The structural reality behind that miss tells a more nuanced story. Maintenance and non-discretionary products, the segment that does not depend on new pool construction or renovation decisions by homeowners, accounted for an estimated 64% of pool product sales in 2025.

That proportion held steady from 2024. Revenue finished the full year essentially flat, down just 0.4%, despite an industry-wide decline in new pool construction to roughly 60,000 units, approximately half of pandemic-era peak volumes. Gross margin for the full year came in at 29.7%, holding even with the prior year after adjusting for a one-time import tax benefit in 2024.

The business is not deteriorating. It is treading water while waiting for the discretionary cycle to turn.

Pool Corporation also made a deliberate capital allocation move ahead of the 2026 season:

The company invested opportunistically in inventory ahead of vendor price increases, building its product inventory balance to $1.45 billion by December 31, a 13% increase from the prior year.

That build positions Pool Corporation to capture pricing benefit from tariff-related cost increases while competitors may face mid-season supply disruptions.

Digital sales, powered by the POOL360 Unlocked platform (an AI-enhanced ordering and customer management tool launched in Q4), reached a record 15% of total annual sales and hit 17% during peak season.

Peter Arvan, President and CEO, stated on the Q4 2025 earnings call that “we are seeing measurable benefits from our strategic investments, including increased efficiency from our technology upgrades, improved customer experiences through digital platforms and enhanced profitability from our supply chain initiatives,” adding that the company expects “these gains to become even more significant in 2026 as our initiatives continue to scale and evolve.”

That framing puts the operating leverage argument squarely on management’s shoulders heading into Q1.

Over the next three to five years, Pool Corporation’s thesis rests on three specific levers: an equipment replacement cycle for variable-speed pumps sold at peak volumes and now entering their end-of-life window, an estimated $200 million in annual dividend commitments supported by the $1.25 quarterly per share declared in February, and a Pinch A Penny franchise network (a company-owned retail and service brand) that crossed 300 locations in 2025 with five new Texas stores added.

Whether Pool Corporation stock earns a meaningful re-rating depends on how quickly consumer confidence returns to the discretionary pool and renovation market.

Wall Street’s Take on POOL Stock

The February earnings miss reset Wall Street’s timeline for Pool Corporation, but it did not change the architecture of the long-term case: a near-monopoly distributor with 64% of revenue tied to non-discretionary maintenance, generating operating leverage from a technology and footprint investment cycle that is now shifting from spending to harvesting.

Pool Corporation’s consensus estimates show 2026 revenue growing to $5.4 billion, a 2.2% increase driven by low single-digit maintenance growth and pricing pass-throughs of 1% to 2% from vendor cost increases, with normalized EPS of $11.00 reflecting the incentive compensation reset that only activates with that level of top-line growth.

Five analysts rate POOL a buy, eight hold it, and one has an underperform. The mean price target is $266.09, implying 24.6% upside from $213.51, but what Wall Street is specifically waiting for is evidence that the discretionary spending recovery is tracking before moving to more constructive positioning.

The target spread from $229 to $340 reflects a genuine debate. The low end essentially prices in another year of muted construction and flat margins. The high end assumes a discretionary demand inflection by mid-2026. Building materials momentum (up 4% in Q4 2025) and the variable-speed pump replacement cycle are the two data points worth monitoring to know which end is tracking.

At roughly 19x forward earnings on 2026 consensus EPS of $11.00, with maintenance revenue holding and the inventory pre-buy positioned to protect margins through at least mid-season, Pool Corporation stock is undervalued against the backdrop of a franchise that has held gross margins flat through the worst new pool construction environment in a decade.

A specific management signal from the Q4 call is worth noting: the 50-plus greenfield locations opened since 2021 are now in what CFO Melanie Hart called “capacity absorption” mode, meaning expense growth should come in below revenue growth in 2026 for the first time in years.

If discretionary spending stays compressed through 2026 and the equipment replacement cycle is slower to materialize, Pool Corporation’s operating margins remain stuck near 11% and the earnings re-rating does not happen.

Q1 2026 results on April 23 are the first read on whether the pre-buy inventory is generating the expected pricing benefit and whether the maintenance business is tracking management’s low single-digit growth guide.

Pool Corporation Stock Financials

Pool Corporation’s operating income has declined from $830 million in 2021 to $580 million in 2025, a compression of $250 million over four years as revenue growth reversed and operating expenses absorbed technology and network investment ahead of the revenue payback.

The gross margin line tells a different story. Pool Corporation held gross margins at 29.7% in 2025, matching the 2024 reported figure and improving 70 basis points in Q4 specifically to 30.1%, a result driven by disciplined supply chain management, strategic private label expansion, and pricing execution on a product mix that skews toward non-commoditized maintenance supplies.

What makes the operating margin trajectory notable is the direction of the underlying driver. Operating expenses grew $34 million to $992 million in 2025, with approximately 1% attributable to new greenfield locations and 1% to incremental technology spend. Both categories of investment are now past their peak spending phase. Management guidance for 2026 calls for expense growth to come in slightly below revenue growth as the capacity built over the last three years begins generating returns rather than costs.

The tension in the income statement is the gap between gross margin stability and operating margin decline: gross margins have held in a 29.7% to 31.3% range since 2021, but operating margins have compressed from 15.7% to 11.0% over the same period. Closing that gap is the entire operating thesis for 2026 and beyond.

What Does the Valuation Model Say?

The TIKR model targets $316 for Pool Corporation by December 2030, a 48.1% total return over 4.7 years, built on a mid-case revenue CAGR of 3.7% and net income margins recovering to 7.9% — a level that requires the operating leverage from the company’s technology and network investments to materialize as management has guided.

At 19x forward earnings with maintenance revenue resilient and operating expenses past their investment peak, Pool Corporation stock is undervalued at a price that embeds permanent construction cycle impairment the gross margin data and installer sentiment do not support.

The range of outcomes for Pool Corporation comes down to one variable: the pace at which discretionary pool renovation and new construction activity recovers, and how much of the operating leverage thesis materializes independent of that recovery.

Low Case: If consumer confidence stays suppressed and construction remains near 60,000 units annually, revenue grows around 3.3% and net income margins stabilize near 7.4% → 4.3% annualized return, target price $261.

Mid Case: With maintenance resilient and the greenfield network beginning to generate positive operating leverage, revenue grows near 3.7% and net income margins improve toward 7.9% → 8.7% annualized return, target price $316.

High Case: If discretionary demand inflects in 2026 to 2027 and the variable-speed pump replacement cycle accelerates alongside renovation demand, revenue reaches around 4.1% growth and net income margins approach 8.2% → 12.4% annualized return, target price $371.

The mid-case requires no multiple expansion: only that Pool Corporation’s maintenance business continues to track, that operating expenses grow slower than revenue for the first time since 2021, and that gross margins hold near 29.7%. Pool Corporation ended 2025 with a $1.45 billion inventory position built specifically for this season, confirmed 1% to 2% pricing pass-throughs from vendor cost increases, and guided incentive compensation to reload only in line with improved results. The conditions for the mid-case are observable and do not depend on a macro turn.

Should You Invest in Pool Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up POOL stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Pool Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze POOL stock on TIKR for Free →