Key Stats for Live Nation Stock

- 52-Week Range: $122.1 to $175.3

- Current Price: $163.2

- Street Mean Target: $184

- Street High Target: $205

- TIKR Model Target (Dec. 2030): $281.3

What Happened?

Live Nation Entertainment (LYV), the world’s largest live entertainment company integrating concert promotion, venue ownership, and ticketing, settled its two-year DOJ antitrust lawsuit in March while reporting 52% operating income growth in fiscal 2025, all at a current price of $163.56.

On March 9, Live Nation reached a settlement with the U.S. Department of Justice, resolving a lawsuit filed in 2024 that sought to break up the company and force the sale of Ticketmaster,its dominant ticket-selling platform that processes roughly 80% of major-venue ticket transactions.

The settlement, which avoids a Ticketmaster divestiture, requires Live Nation to give up exclusive booking agreements at 13 amphitheaters, allow venues to use competing ticketing platforms, and set aside $280 million to resolve claims by participating states, removing the existential breakup risk that had weighed on the stock since mid-2024.

On March 31, Live Nation completed the acquisition of ForumNet Group, Italy’s largest venue operator anchored by Milan’s Unipol Forum, a 12,700-capacity indoor arena that will also host events during the 2026 Winter Olympics, for an enterprise value of roughly 90 million euros ($106 million).

Joe Berchtold, President and CFO, stated on the Q4 2025 earnings call that “we’re continuing to see very strong consistent demand” and that 80% of 2026 large-venue shows were already booked, with stadium show counts up double digits internationally, anchoring the company’s guidance for double-digit adjusted operating income growth across its concert segment in 2026.

Live Nation’s Venue Nation strategy, a long-term plan to own and operate arenas globally in markets underserved by NBA and NHL infrastructure, now spans venues across Paris, Milan, Latin America, and Asia, targeting a multi-year ramp where each owned venue reaches mature profitability within two to three years of opening.

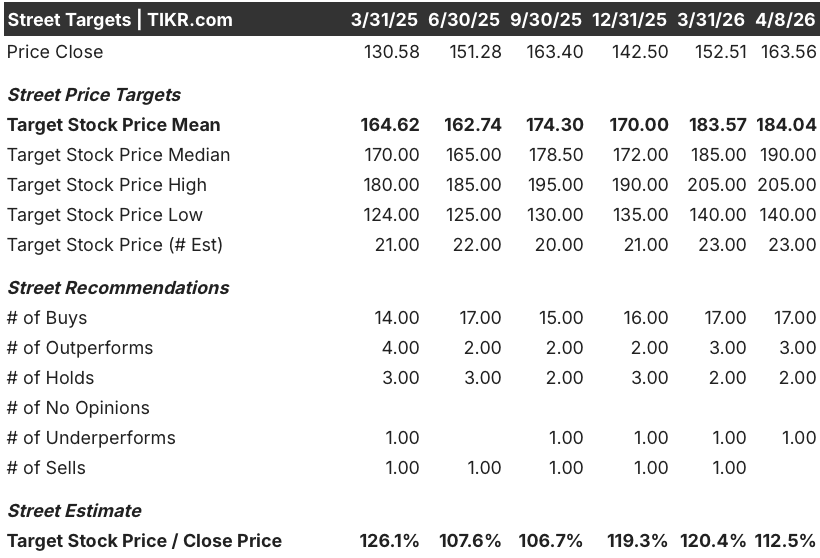

Wall Street’s Take on LYV Stock

Removing the DOJ breakup threat converts Live Nation stock from a structurally discounted holding into a clean margin expansion and cash generation story, and the forward numbers reflect exactly that shift.

LYV’s consensus 2026 EBITDA estimate of $2.63 billion, up 11% from $2.37 billion in 2025, is supported by the 159 million fan attendance record in fiscal 2025 and 67 million tickets already sold through early 2026, up double digits versus the same period last year, both driven by the artist supply pipeline and the booking visibility Berchtold described on the earnings call.

Twenty of 23 analysts covering LYV rate the stock a buy or outperform, with a mean 12-month target of $184.04 representing 12.5% upside, while Wall Street waits for Venue Nation pre-opening costs (guided at $50 million for 2026) to taper and the owned-venue AOI ramp to inflect toward the mature portfolio run rate management outlined at its investor day.

The $140 to $205 target spread captures a real debate: the $140 floor prices in sustained structural damage from the 20-plus state attorneys general who rejected the DOJ deal and continue to litigate, while the $205 ceiling reflects full re-rating if state claims settle before 2028 and Venue Nation delivers on its per-fan economics.

Trading at roughly 17x 2026E EBITDA with 11% annual EBITDA growth ahead and Ticketmaster’s strategic moat intact after the settlement, Live Nation stock is undervalued relative to what the post-settlement business model actually earns.

The ongoing state litigation, led by New York and California, is the model’s core vulnerability: a court ruling requiring deeper contract restructuring could impair Ticketmaster’s multi-year venue renewal rates and the GTV growth trajectory that supports the EBITDA outlook.

Q2 2026 results, the first full quarter reflecting the post-settlement operating environment and the ForumNet close, will confirm whether concert AOI is tracking the double-digit guidance and whether Venue Nation ramp costs stay within the guided range.

Live Nation Entertainment Financials

LYV’s operating income grew 67.2% to $1.32 billion in fiscal 2025, the sharpest annual improvement in the company’s post-pandemic history, as revenue grew 8.8% to $25.2 billion and cost discipline across the Ticketing and Sponsorship segments allowed incremental concert revenue to flow through at a higher rate.

The concert segment drove Live Nation’s revenue expansion, with the company investing nearly $15 billion in artists and shows to secure a 159 million fan attendance record, the supply-side commitment that anchors both the 2026 forward booking data and the sponsorship pipeline running double digits ahead year over year.

Gross margins expanded from 23.9% in fiscal 2023 to 25.5% in fiscal 2025, a 160-basis-point recovery that reflects improving sponsorship mix, which is the highest-margin business line, and Ticketing gross profit stability even as the company absorbed secondary-market headwinds in the back half of the year.

LYV’s operating margins remain structurally thin at 5.3%, a feature of a business model where artist investment flows through cost of revenue, but the recovery from 3.4% in fiscal 2024 confirms the operating leverage thesis is tracking as the business scales toward the Venue Nation portfolio build.

What Does the Valuation Model Say?

The TIKR model’s mid-case target of $281 assumes 7.5% annual revenue CAGR through 2030 with net income margins reaching 2.2%, a set of inputs the 2025 trajectory already supports given 8.8% revenue growth, the 67 million early-2026 tickets sold at double-digit pacing, and over 70% of 2026 sponsorship commitments already booked.

A 72% total return over 4.7 years makes Live Nation stock undervalued at current prices — the multiple still carries antitrust discount that the DOJ settlement has materially reduced.

How far LYV travels between a $211 floor and a $339 ceiling depends on one variable the model cannot fully price: whether the remaining state litigation resolves cleanly or drags structural uncertainty into 2028 and beyond.

Low Case (6.7% Revenue CAGR, 1.9% Net Income Margin → $211 target, 5.5% annualized)

- State attorneys general litigation extends past 2027, creating renewal uncertainty across Ticketmaster’s major-venue contract base and moderating ticketing GTV growth

- Venue Nation pre-opening costs persist above $50 million as international builds face delays, delaying AOI inflection to 2029

- Concert revenue CAGR of 6.7% reflects modest attendance growth with no upside from Ticketmaster secondary-market recovery

High Case (8.2% Revenue CAGR, 2.2% Net Income Margin → $339 target, 16.6% annualized)

- State litigation broadly resolves by 2027, eliminating the last structural discount and enabling full institutional re-rating of LYV

- Venue Nation venues in Paris, Milan, and Latin America reach mature profitability by 2028, with owned-venue fan count compounding as new builds are added annually

- International stadium shows sustain double-digit growth beyond 2025’s record base, extending the attendance and sponsorship flywheel

The mid-case requires 7.5% revenue growth and 2.2% net income margins through 2030, both consistent with the trajectory visible today, and it requires no multiple expansion to deliver $281.

Ticketmaster posted record January concert ticket GTV (up over 50%), 67 million 2026 tickets are already sold at double-digit growth, and Berchtold confirmed on the earnings call that forward supply across arenas, amphitheaters, and stadiums is running ahead of both 2024 and 2025 levels — the mid-case is not a projection, it is a description of what is already in motion.

Should You Invest in Live Nation Entertainment, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up LYV stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Live Nation Entertainment, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze LYV stock on TIKR for Free →