Key Stats for Enphase Stock

- 52-Week Range: $25.8 to $55.4

- Current Price: $32.

- Street Mean Target: $45.8

- Street High Target: $85

- TIKR Model Target (Dec. 2030): $55.3

What Happened?

Enphase Energy (ENPH), the maker of microinverters that convert rooftop solar into usable household power, is trading at $32.04 — near a two-year low — despite Q4 sell-through demand hitting its highest level in more than two years.

Q4 2025 revenue of $343.3 million beat the $340.6 million consensus estimate, and Enphase guided Q1 2026 revenue of $270 million to $300 million, above the $264.6 million analysts expected at the time.

Sell-through of microinverters and batteries — the actual rate at which installers are deploying product to end customers — rose 21% sequentially in Q4, signaling that channel inventory has cleared and real demand is rebuilding from its trough.

Badrinarayanan Kothandaraman, President and CEO, stated on the Q4 2025 earnings call that “Q1 marks the low point for underlying demand with improvement expected through 2026, particularly in the second half,” anchoring the company’s forward outlook to three named tailwinds: rising utility rates across the Northeast and Midwest, new prepaid lease financing structures replacing the expired Section 25D residential tax credit, and anticipated interest rate easing through the year.

ENPH’s path to recovery over the next three to five years now rests on five specific execution levers: IQ Battery 10C expansion to 50 additional utility approvals, scaling the IQ9 GaN commercial microinverter into the new $400 million 480-volt commercial market, battery retrofit campaigns targeting the roughly 475,000 installed Enphase systems in the Netherlands, a fifth-generation battery platform targeting 50% higher energy density at 40% lower cost, and a prepaid lease pilot currently running across four states with more than 40 installers.

On April 6, Enphase disclosed an agreement signed March 31 to sell $235 million of Section 45X Advanced Manufacturing Production Tax Credits — federal credits earned for U.S.-manufactured microinverter components — for $218.55 million in cash, monetizing manufacturing tax assets at 93 cents on the dollar and reducing Q1 GAAP gross margin guidance by approximately 6.7 percentage points.

Wall Street’s Take on ENPH Stock

The Q4 beat and above-consensus Q1 guidance mark the first time in 18 months that Enphase held its initial quarterly outlook rather than cutting it, which J.P. Morgan characterized as an early signal that the company’s forward visibility is beginning to improve.

Enphase stock’s consensus revenue estimate sits at $1.25 billion for FY26 — a 15.3% decline from FY25’s $1.47 billion — yet free cash flow is expected to surge 311% to $0.39 billion as cost cuts and the removal of safe harbor inventory distortions normalize the cash generation picture; normalized EPS of $2.21 is expected for FY26, recovering to $2.71 in FY27 and $3.13 in FY28, supported by the IQ9 commercial ramp and Netherlands battery retrofit campaigns Kothandaraman outlined on the Q4 call.

Eight analysts rate Enphase stock a Buy or Strong Buy and three rate it Outperform, against 17 Holds and five Sells, with a mean price target of $45.76 — implying 42.8% upside from the April 7 close — as Wall Street awaits confirmation that the Q2 sequential revenue improvement materializes on the April 28 earnings call.

The $27 bear case and $85 bull case on the Street reveal a genuine debate: bears are pricing in prolonged U.S. residential demand destruction from the Section 25D credit expiration and sustained tariff pressure on margins, while bulls are underwriting the commercial IQ9 ramp and Netherlands battery retrofit as new revenue streams that shift ENPH’s end-market mix beyond residential.

Trading at roughly 14x forward normalized EPS of $2.21 against a five-year historical forward P/E closer to 30x, Enphase stock is undervalued given that the earnings compression is driven by a one-year policy shock — the 25D credit expiration — rather than structural deterioration in the microinverter franchise.

Kothandaraman’s confirmation that the prepaid lease pilot is live across four states with 40 installers provides the first concrete evidence that a commercial financing replacement for the residential tax credit is operational, not merely theoretical.

If the Netherlands battery retrofit program or the IQ9 commercial ramp stalls, both the margin recovery and the revenue reacceleration timeline extend by at least two to four quarters, pushing the TIKR mid-case target price materially further out in time.

The single number to watch on April 28 is Q2 revenue guidance: any figure above $300 million confirms that Q1 was genuinely the trough and that the prepaid lease and commercial ramp are moving from pilot to scale.

Enphase Energy Stock Income Statement

Enphase’s gross profit fell to $0.45 billion in FY25 — a 4.9% decline from FY24’s already compressed $0.47 billion — pulling gross margins to 30.4%, the lowest level in at least four fiscal years.

The gross margin compression traces directly to the Section 45X tax credit accounting treatment, where $235 million of credits generated in 2025 were sold below face value and the associated impact reduces reported GAAP gross margins, compounding the tariff drag of 5.1 percentage points Kothandaraman quantified on the Q4 call.

ENPH’s operating income recovered to $0.16 billion in FY25 — an 82.1% improvement from FY24’s $0.09 billion trough — as operating margins rebuilt from 6.8% to 11.2%, demonstrating that cost discipline and workforce reductions are translating into operating leverage even as gross margins remain under pressure.

The tension in the income statement is real: ENPH’s 30.4% gross margin in FY25 sits well below the 46.2% gross margin posted in FY23, and the path back depends on the fifth-generation battery delivering its promised 40% cost reduction and the IQ9 commercial microinverter commanding the premium margins that higher domestic content and FEOC compliance justify.

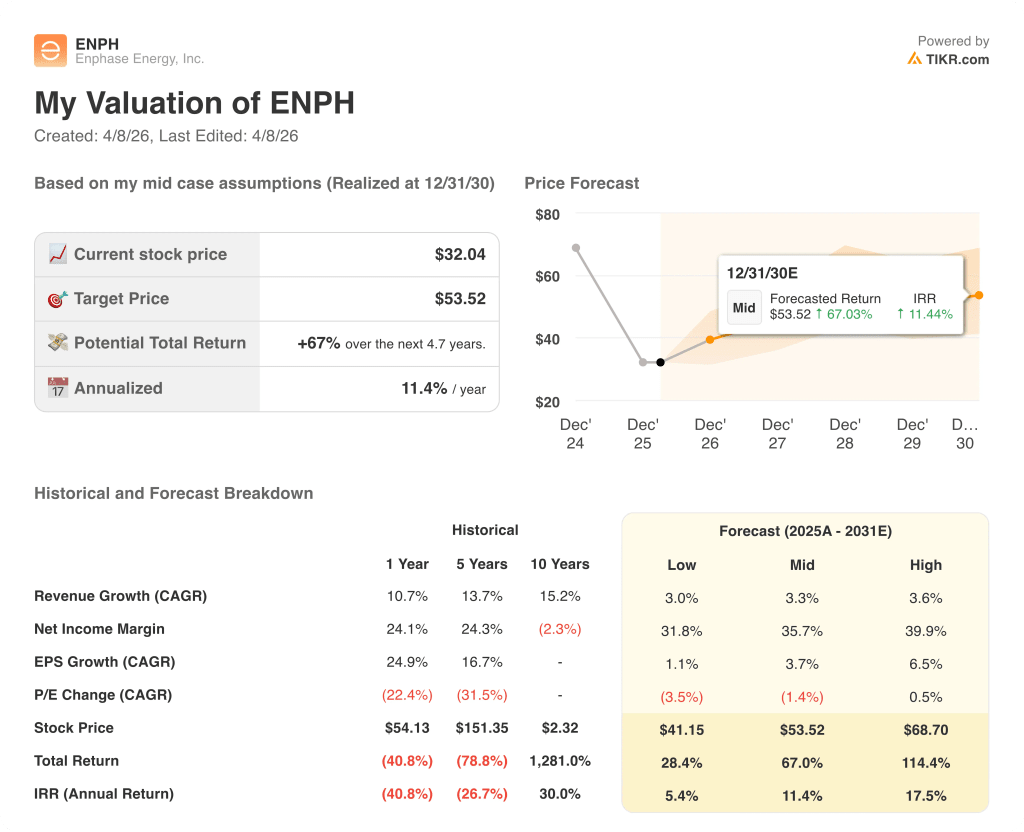

What Does the Valuation Model Say?

The TIKR mid-case model returns a $53.52 price target on revenue growing at just 3.3% annually through 2030 — a fraction of ENPH’s 13.7% five-year historical CAGR — implying the model prices in near-permanent demand impairment that the Q4 sell-through data and IQ9 commercial pipeline do not support.

At $32.04 with the model requiring only 3.3% revenue growth to generate a 67% total return, ENPH is undervalued — the multiple prices in a structural collapse the underlying business data has not confirmed.

The central tension in the ENPH investment case is not whether residential solar recovers, but whether commercial solar and battery retrofit revenue can grow fast enough to offset the residential trough before investors lose patience.

Low Case — If the prepaid lease pilot stalls, Netherlands retrofit adoption lags, and tariffs persist, revenue grows around 3.0% and margins stabilize near 31.8% → 5.4% annualized return, target price $41.

Mid Case — With the IQ9 commercial ramp delivering initial scale, battery retrofits gaining traction across Europe, and the fifth-gen battery launching in Q4, revenue grows near 3.3% and net income margins improve toward 35.7% → 11.4% annualized return, target price $54.

High Case — If commercial solar captures meaningful market share and the Netherlands battery retrofit campaign drives sustained volume above Kothandaraman’s 100-event target, revenue reaches around 3.6% and net income margins approach 39.9% → 17.5% annualized return, target price $69.

The mid-case requires Q2 2026 revenue to confirm the trough, the fifth-gen battery to begin pilots in Q3 as guided, and no multiple expansion — just execution against already-announced product and market initiatives toward a $54 target price.

Right now, the evidence is directionally supportive: channel inventory is lean, Q4 sell-through rose 21% sequentially to a two-year high, the IQ9 commercial backlog already exceeded 50,000 units for Q1, and the Netherlands homeowner event program generated preorders from its initial ten events — making the mid-case the live scenario, not an aspirational one.

Should You Invest in Enphase Energy, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ENPH stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Enphase Energy, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ENPH stock on TIKR for Free →