TargetKey Stats for Global Payments Stock

- 52-Week Range: $62.7 to $90.9

- Current Price: $64.05

- Street High Target: $194

What Happened?

Global Payments (GPN), a payment technology company that processes transactions for over 6 million merchant locations worldwide, crossed a strategic inflection point after completing the Worldpay acquisition and the simultaneous divestiture of its Issuer Solutions business, guiding for 13% to 15% adjusted EPS growth in 2026 as shares trade at $64.05.

On February 18, Q4 2025 earnings showed adjusted EPS of $3.18, beating the consensus estimate of $3.16, while the company simultaneously announced a $2.5 billion share repurchase authorization and a $550 million accelerated share repurchase plan targeting 30% of its market cap returned to shareholders by end of 2027.

The Worldpay integration is already generating measurable commercial traction, with Worldpay’s U.S. direct sales force enabled to sell Genius, GPN’s AI-powered point-of-sale platform, within weeks of the January close and new Genius restaurant rooftops up more than 50% year over year at the end of 2025.

Cameron Bready, Chief Executive Officer, stated on the Q4 2025 earnings call that “at current valuation levels, we see buybacks as a highly compelling opportunity to drive shareholder value, given the clear dislocation between our share price and the fundamental performance and outlook for the business,” directly tying the $550 million accelerated repurchase to management’s conviction in the mispricing.

Global Payments’ repositioning as a pure-play merchant solutions provider, anchored by $600 million in targeted Worldpay expense synergies over three years, a $7.5 billion capital return target through 2027, and a $1 billion annual technology investment commitment, positions it to reach the mid- to high-single-digit revenue growth rate management has explicitly set as its medium-term objective.

Wall Street’s Take on GPN Stock

The Worldpay acquisition’s January close unlocks $600 million in expense synergies over three years and $200 million in revenue synergies, directly supporting the 13% to 15% adjusted EPS growth guidance that makes the capital return program self-funding.

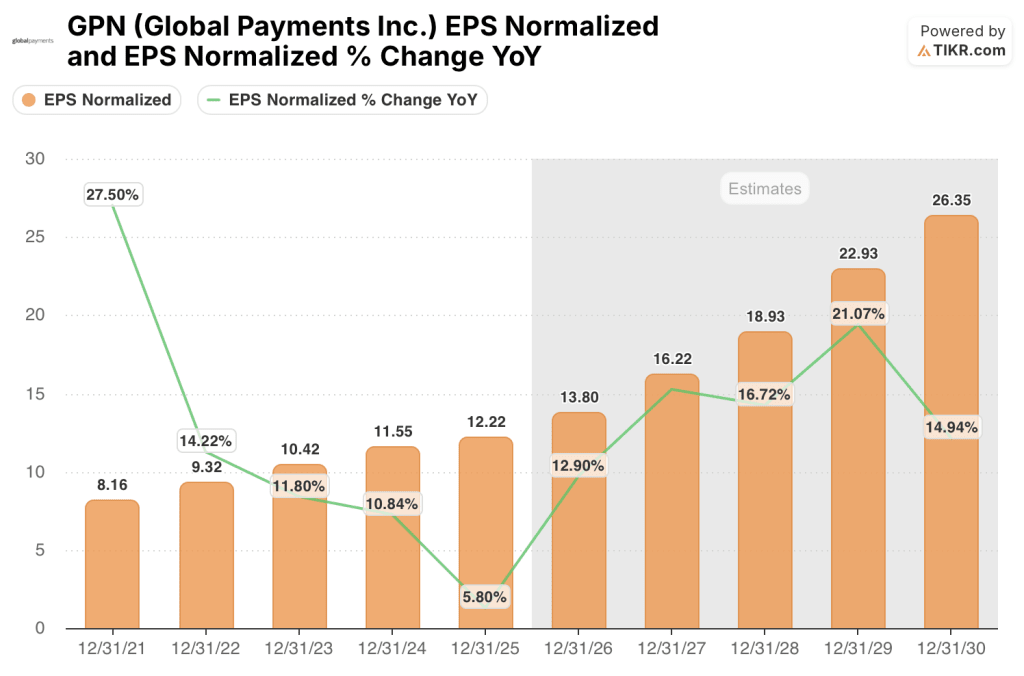

GPN’s normalized EPS is estimated at $13.80 for 2026, a 12.9% jump from $12.22 in 2025, driven by 150 basis points of guided operating margin expansion as the first $70 million to $80 million in Worldpay cost synergies flow through and Genius payment attach rates continue climbing off the 2025 base.

Wall Street carries 12 buys, 19 holds, and 2 sells across 33 analysts covering the stock, with a median price target of $95.00, implying roughly 48% upside from the April 2 close of $64.05, a posture that has yet to fully reprice for the combined company’s earnings acceleration.

The target spread is meaningful: the low anchors to integration execution risk and top-line growth staying below 5%, while the high reflects full realization of Worldpay synergies and Genius scaling into new verticals and geographies through Worldpay’s distribution network.

What Does the Valuation Model Say?

The TIKR mid-case model prices GPN at $111.28 by December 31, 2030, implying a 12.3% annualized IRR, driven by a 9.5% revenue CAGR assumption grounded in the Worldpay combination’s scale, Genius expansion into 50-plus Worldpay referral bank channels, and $200 million in targeted revenue synergies compounding on top of organic merchant volume growth.

Trading at roughly 4.6x 2026 normalized EPS of $13.80, GPN sits at a steep discount to its own recent multiple history and meaningfully below the payment technology peer group, even as EPS growth accelerates from 5.8% in 2025 to a guided 12.9% in 2026, leaving GPN deeply undervalued at a moment of fundamental improvement.

The $550 million accelerated share repurchase already in motion, combined with $3.4 billion in estimated 2026 free cash flow and a confirmed $7.5 billion capital return target through 2027, justifies the TIKR model’s $111.28 price target as the earnings base compounds and the multiple re-rates toward historical norms.

Bready’s statement at the Wolfe FinTech Forum on March 10 that the business feels better today than when the Worldpay transaction was announced confirms this is a structural repositioning story, not a cyclical bounce playing out at a depressed multiple.

If Genius adoption slows or Worldpay integration disrupts merchant retention, the 9.5% revenue CAGR assumption breaks and the $111.28 model target compresses materially.

The Q1 2026 earnings release will be the first clean read on Genius rooftop growth through Worldpay’s 50 largest referral banks and whether the $70 million to $80 million in synergies are tracking on schedule.

Should You Invest in Global Payments Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up X stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track GPN alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze GPN stock on TIKR for Free →