Key Stats for Waste Management Stock

- 52-Week Range: $194.1 to $248.1

- Current Price: $235.4

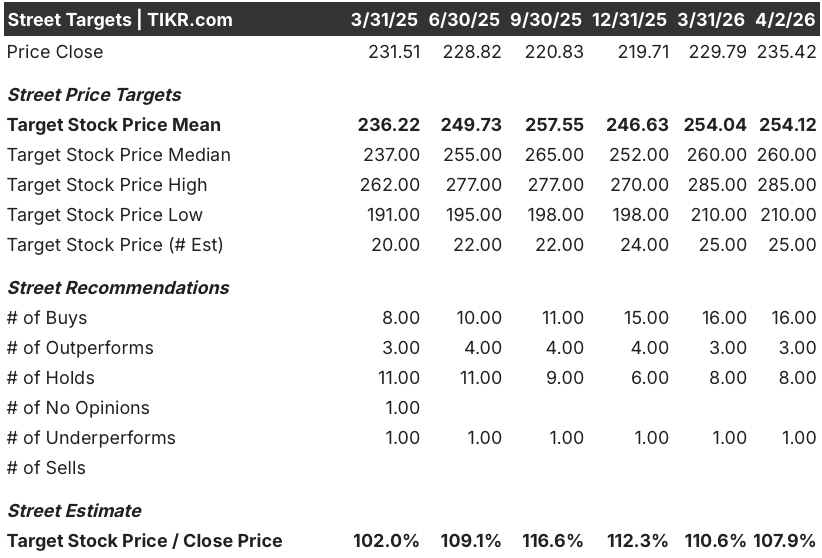

- Street High Target: $285

What Happened?

Waste Management, Inc. (WM), the largest waste collection and disposal company in North America, crossed a structural threshold in 2025 by pushing operating expenses below 60% of revenue for the first time in company history, even as it absorbed the Stericycle healthcare waste acquisition, with shares trading at $235.42.

On January 29, WM reported Q4 2025 results that missed revenue estimates at $6.31 billion versus the $6.39 billion consensus, yet still delivered a record 31.3% quarterly operating EBITDA margin and all-time high collection and disposal EBITDA margin of 39%.

The structural cost story is the sharpest proof point: WM achieved 59.5% operating expenses as a percentage of revenue for the full year, driven by fleet automation, a connected truck platform giving managers real-time routing visibility, and driver turnover falling to 15.7% in Q4, while the recycling business delivered 22% EBITDA growth despite commodity prices falling nearly 20%.

On March 3, WM’s board granted annual performance share units and stock options to its executive team, with PSU payouts tied 50% to cash flow generation and 50% to total shareholder return versus the S&P 500, measured through December 31, 2028, directly aligning management incentives with the free cash flow inflection already in motion.

Moreover,, CEO James C. Fish Jr. stated on the Q4 2025 earnings call that “we are well positioned to convert more of our earnings into long-term shareholder value,” directly anchoring his remarks to the company’s 2026 guidance of nearly 30% free cash flow growth to $3.8 billion and $3.5 billion in planned shareholder returns through dividends and buybacks.

WM’s competitive position over the next three to five years compounds through three converging forces: free cash flow scaling from $2.94 billion in 2025 toward a ~$1 billion sustainability EBITDA contribution by 2027 from renewable natural gas and recycling investments, Healthcare Solutions SG&A declining from 25% at acquisition toward the company’s core 9% target, and a $3 billion share repurchase program beginning Q1 2026 that management confirmed as a recurring program, not a one-time event.

Wall Street’s Take on WM Stock

WM’s first-ever sub-60% annual operating expense ratio directly unlocks the math behind the company’s 2026 guidance: EBITDA of $8.21 billion estimated this year, up 8.2% from $7.58 billion in 2025, on revenue growing only 5.1%.

Meanwhile, the structural cost reset, driven by fleet automation, connected truck logistics, and Healthcare Solutions SG&A declining from 25% at acquisition toward the company’s core 9% target, supports EPS normalized growth from $7.50 in 2025 to an estimated $8.21 in 2026 and $9.36 in 2027.

Sixteen analysts carry Buy ratings on WM against eight Holds and one Underperform across 25 estimates, with a mean price target of $254.12 implying 7.9% upside from the April 2 close as Wall Street prices in the FCF inflection and $3.5 billion shareholder return program for 2026.

The spread between the $210 low target and $285 high reflects a real binary: the bull case prices in Healthcare Solutions SG&A normalizing and recycling commodity prices recovering from $62 per ton, while the bear case assumes Stericycle integration costs persist and credit memo headwinds linger into the second half.

What Does the Valuation Model Say?

The TIKR mid-case model targets $388.04 by December 2030, assuming a 5.3% revenue CAGR and net income margins expanding to 14.6%, justified directly by the structural operating cost reset and renewable natural gas output doubling in 2026 as new facilities come online.

At roughly 28.9x 2026 estimated FCF ($235.42 on $3.77 billion FCF) against a FCF margin expanding from 11.7% in 2025 to 14.2% in 2026 and 14.8% in 2027, WM trades modestly above its own 5-year average FCF multiple for a business whose cost structure just permanently reset lower, making WM stock fairly valued today with a clear path to re-rating as the Stericycle integration completes and sustainability EBITDA approaches $1 billion by 2027.

The $3 billion share repurchase program beginning Q1 2026, combined with the $388.04 TIKR mid-case target anchored to 9.9% EPS CAGR through 2030, justifies the model’s 11.1% annualized IRR assumption as FCF conversion above 46% of EBITDA provides the capital to fund both returns and sustainability growth CapEx simultaneously.

Management’s decision to tie executive PSU payouts 50% to cash flow generation through December 2028 directly signals that the FCF inflection is the internal scorecard metric, not just an analyst talking point.

The key risk is Healthcare Solutions integration stalling: if SG&A in that segment fails to decline from 20.8% toward the 9% target, the EBITDA margin expansion thesis breaks and the $8.21 billion 2026 estimate becomes unreachable.

WM reports Q1 2026 results on April 28, and the number to watch is operating EBITDA margin against the 30.1% full-year 2025 baseline, specifically whether Healthcare Solutions SG&A continues its sequential decline from the Q4 20.8% exit rate.

Should You Invest in Waste Management, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up WM stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Waste Management, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze WM stock on TIKR for Free →