Key Stats for Lululemon Stock

- 52-Week Range: $144 to $340.3

- Current Price: $155.7

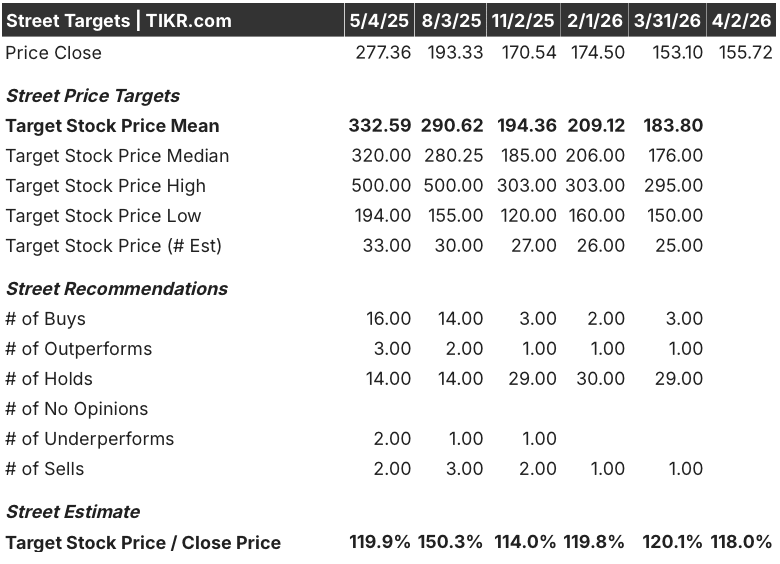

- Street High Target: $295

What Happened?

Lululemon Athletica (LULU), the premium athletic apparel brand built on high-margin technical leggings and a loyal direct-to-consumer base, trades at $155.72 after losing more than half its value in two years as design missteps, a CEO departure, and a $380 million tariff headwind converged into the brand’s deepest operational reset in a decade.

The trigger arrived March 17 when LULU reported Q4 FY2025 net revenue of $3.64 billion, a narrow beat against the $3.58 billion estimate, but diluted EPS fell to $5.01 from $6.14 a year earlier as gross margin collapsed 550 basis points to 54.9%, with U.S. import tariffs on China-sourced manufacturing accounting for 520 basis points of that decline.

International operations proved the one undeniable bright spot, with China Mainland revenue surging 28% in Q4 while Americas net revenue fell 4%, a divergence that confirms the brand’s premium positioning travels better overseas than it currently executes at home against fast-growing rivals Alo Yoga and Vuori.

Interim co-CEO and CFO Meghan Frank stated on the Q4 FY2025 earnings call that “a top priority for the management team as we enter the year is returning to full-price sales growth in North America… through a series of steps that include the inflection of product newness, SKU reduction and rebalancing the inventory levels,” directly anchoring the recovery thesis to three execution-dependent levers already in motion.

The board overhang shifted in March with the appointment of Chip Bergh, the former Levi Strauss CEO who guided that brand’s turnaround and 2019 IPO, while founder Chip Wilson, controlling 4.27% of shares, called the move insufficient and pressed for broader board replacement before any permanent CEO selection, per Reuters wire on March 18.

Meanwhile, a federal judge overturned a jury verdict on March 31 finding LULU had infringed a Nike manufacturing patent covering the knitted upper structure of its Chargefeel and Blissfeel running shoes, eliminating a $355,450 damages award and removing one litigation overhang even as a separate Nike case remains pending.

Insider conviction followed the stock lower: director Charles V. Bergh’s trust purchased approximately $999,378 of Lululemon shares on March 23 and interim co-CEO Andre Maestrini added approximately $494,591 on April 3 at $151.02, two executives putting capital behind a recovery thesis the market has not yet priced in.

Wall Street’s Take on LULU Stock

LULU’s normalized EPS has already contracted 9.4% to $13.26 in FY2026A and faces a further 7.1% decline to $12.32 in FY2027E, but the insider buying, board reset, and full-price inflection guidance collectively signal the earnings trough is closer than the stock price implies.

LULU’s normalized EPS troughs at an estimated $12.32 in FY2027E before recovering to $24.99 by FY2031E, a trajectory the TIKR model supports through China Mainland’s 20% revenue growth guidance for FY2026 and a North America full-price inflection that management guided to turn positive in the second half of this year.

Wall Street’s posture is overwhelmingly cautious, with 29 of 34 analysts holding a neutral rating, a mean price target of $183.80 implying 18% upside from current levels, and the Street withholding conviction until a permanent CEO provides a concrete strategy to reclaim North America share from Alo Yoga and Vuori.

The target range from $150 to $295 reflects genuine disagreement: the bear case anchored at $150 prices in continued North America deterioration and no CEO resolution, while the $295 bull case requires the full-price inflection to accelerate through the second half and a re-rating catalyst in the form of a credible permanent CEO appointment.

What Does the Valuation Model Say?

The TIKR mid-case model prices lululemon at $203.32 by January 2031, assuming a 4.2% revenue CAGR supported by mid-teens international expansion and a North America recovery, with net income margins rebuilding to 12.5% as tariff offsets from enterprise efficiency initiatives scale toward the guided $160 million annually.

At 12.5x forward earnings, LULU trades near a decade low on its own multiple history for a brand that compounded EPS at 21.7% over ten years and still holds the top U.S. women’s activewear position, making LULU stock undervalued relative to its own normalized earnings power, with a 3.3% EPS CAGR to FY2031E as the conservative floor, not the ceiling.

The evidence supporting the TIKR target is the insider buying signal: two executives purchased a combined $1.5 million of LULU shares near 52-week lows in consecutive weeks while management simultaneously guided full-price selling to inflect positive in Q2, directly supporting the $203.32 mid-case assumption that the markdown cycle has already found its floor.

The signal that this is a misunderstood stock rather than a broken one is the stability of new guest acquisition, retention, and brand relevance metrics through FY2025, which management confirmed held steady even as North America comparable sales turned negative.

No permanent CEO means no multiple re-rating, and every quarter of interim leadership extending past mid-year increases the risk that the full-price inflection arrives too late to offset the 250 basis point operating margin compression guided for FY2026.

A permanent CEO announcement is the single catalyst that changes LULU’s investment identity from a governance distraction to a brand recovery, and the number to watch is Q2 North America full-price sales growth, which management guided to inflect flat before turning positive in the second half.

LULU at $155.72 is a brand-recovery option priced as a broken retailer, and the 5.7% annualized IRR in the TIKR mid-case understates the upside if a permanent CEO appointment triggers the multiple re-rating the earnings trajectory already justifies.

Should You Invest in lululemon athletica inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up LULU stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track lululemon athletica inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze LULU stock on TIKR for Free →