Key Stats for Union Pacific Stock

- 52-Week Range: $204.7 to $268.1

- Current Price: $244.7

- Street High Target: $

What Happened?

Union Pacific (UNP), the largest freight railroad in the western United States, is executing at a record operational level while simultaneously pursuing the most transformative merger in modern rail history, with its $244.71 stock trading roughly 10% below the street’s mean price target of $271.38.

On February 4, Union Pacific signed a $1.2 billion agreement with locomotive parts maker Wabtec to modernize over 1,700 AC4400 locomotives, the largest locomotive modernization investment in rail industry history, with deliveries beginning in 2027.

The fleet upgrade is engineered to reduce fuel consumption by over 5%, increase tractive effort by 14%, and improve locomotive reliability by 80%, reinforcing a network that already set best-ever records for freight car velocity, locomotive productivity, and fuel consumption in 2025.

CFO Jennifer Hamann stated at the Barclays 2026 Industrial Select Conference that “the network is running, we’re back at, call it, 230, 240 car miles per day,” adding that the company expects “every carload that’s available” to be captured as tightening truck capacity drives shippers toward rail.

Union Pacific’s planned $85 billion merger with Norfolk Southern, which would create America’s first coast-to-coast freight railroad, remains on track for a first-half 2027 close, with the revised STB application due April 30 targeting 2 million truckload conversions and 24 to 48 hours of transit time savings on interchange traffic.

Wall Street’s Take on UNP Stock

Union Pacific’s investment thesis is an operating leverage story built on a railroad that already runs 24% fewer trains than in 2019 on the same volume, while an $85 billion merger with Norfolk Southern adds a layer of optionality the current $244.71 stock price does not fully price in.

The fundamental case starts with the operating ratio. Union Pacific’s adjusted full-year 2025 operating ratio improved 60 basis points to 59.3%, and management has committed to improving it further in 2026, driven by workforce productivity gains that already delivered 3% fewer employees on 1% more volume last year. That cost discipline supports consensus 2026 EPS of $12.39, up from $11.98 in 2025, even as price is expected to contribute less than it did in prior years.

Management has committed to improving it further in 2026, driven not by price but by continued productivity gains, with workforce levels already 3% lower on 1% more volume in 2025.

Consensus estimates project 2027 EPS of $13.56, a 9.3% jump from 2026, supported by two structural tailwinds already in motion:

- The $1.2 billion Wabtec locomotive modernization program beginning deliveries in 2027, which is engineered to cut fuel consumption by over 5% per upgraded unit and improve reliability by 80%,

- and the merger with Norfolk Southern, which management expects to close in the first half of 2027 and which targets 2 million truckload conversions onto the combined network.

Revenue is also projected to grow from $24.5 billion in 2025 to $26.7 billion in 2027, a 9% two-year expansion driven by those same truck-to-rail conversion wins that CFO Jennifer Hamann confirmed at the Barclays conference are already showing up in domestic intermodal volumes.

Wall Street is broadly constructive on Union Pacific, with 15 buys, 2 outperforms, 8 holds, and 1 underperform among the 26 analysts covering the stock, and a mean price target of $271.38 against a current price of $244.71, implying roughly 11% upside from here.

The debate among analysts centers on whether productivity alone can drive margin improvement in a year where price is not expected to contribute.

TD Cowen cut its target to $255, citing a muted economic environment with continued industrial softness, though it noted coal carloadings up 20% year-to-date as a near-term offset.

JPMorgan, at $265, flagged weakness across autos and housing as persistent volume headwinds. Citigroup was the outlier on the bullish side, raising its target to $270 and noting that “rail inflation is ticking up again” while still expecting operational execution to drive margin improvement.

United Pacific Corp Financials

Union Pacific’s total revenues grew from $22.6 billion in 2023 to $24.5 billion in 2025, with gross margins expanding from 53.5% to 56.4% as the railroad’s efficiency program lowered the cost base faster than revenue decelerated.

Operating income held at $9.97 billion in 2025 despite only 1.1% revenue growth, as total operating expenses of $3.84 billion were effectively flat year-over-year, demonstrating that cost discipline, not volume, is driving the margin recovery.

Consensus estimates project revenue accelerating to $25.4 billion in 2026 and $26.7 billion in 2027, with operating margins expanding to 41.6% and 42.7% respectively, a trajectory that assumes truck-to-rail conversion gains and merger-adjacent volume wins begin to materialize at scale.

The one tension in the data is free cash flow: at $5.5 billion in 2025, FCF declined 6.7% year-over-year as higher capital spend pulled cash conversion lower, though estimates project a sharp recovery to $6.8 billion in 2026 as the capital cycle moderates from $3.8 billion to $3.3 billion.

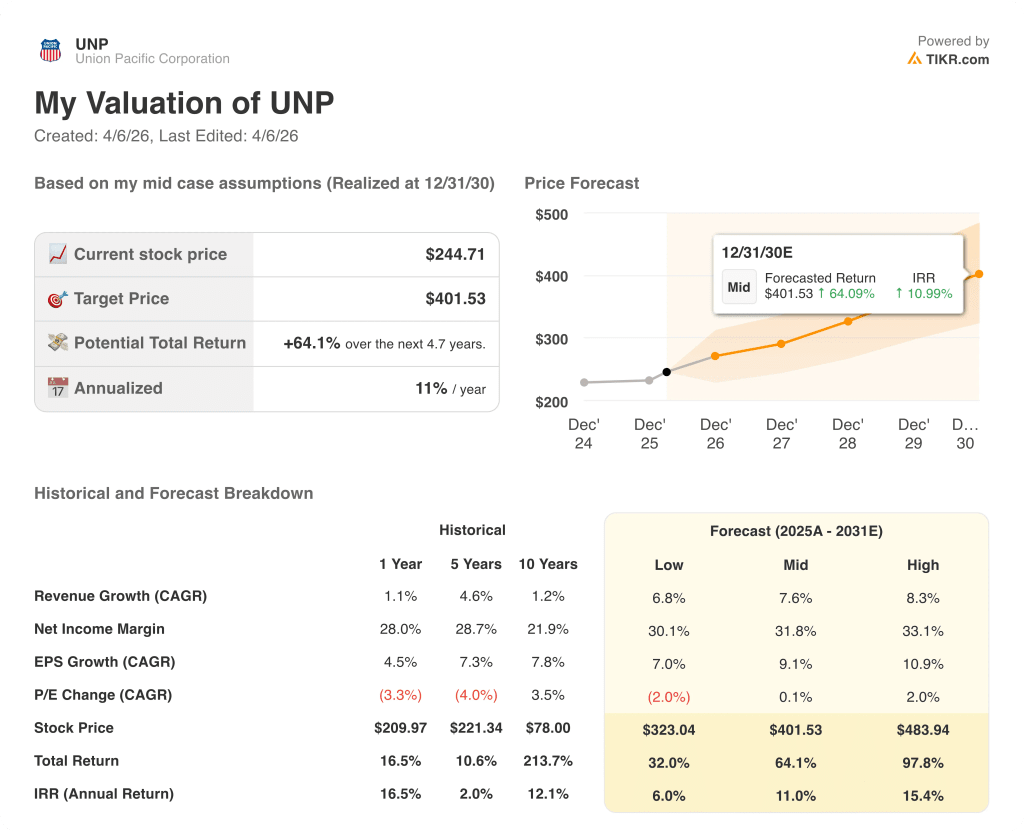

What Does the Valuation Model Say?

The TIKR model’s mid-case target of $401.53 by December 2030, implying an 11% annualized IRR, reflects a more complete picture that includes EPS compounding at a 9.1% CAGR through 2027 and margin expansion toward a 31.8% net income margin.

The key debate among analysts is whether price can drive margin improvement in 2026.

TD Cowen cut its target to $255, citing a muted economic environment, while Citigroup raised its target to $270, noting that “rail inflation is ticking up again” and that price may be less of a driver than productivity. JPMorgan, at $265, flagged weakness across autos and housing as volume headwinds.

The bull case is that none of those concerns are structural: industrial volumes were up 4% in Q1 2026 through 10 weeks, bulk loadings were up 14%, and domestic intermodal continues to benefit from over-the-road truck conversions enabled by record service levels.

The merger adds a credible asymmetric upside. CEO Jim Vena, at the JPMorgan Industrials Conference on March 18, said that “if something comes back to destroy the incremental nature of the merger, we would walk away from it,” drawing a clear line between protecting the core franchise and pursuing the deal.

That framing matters: it signals that the $85 billion transaction is structured not to dilute Union Pacific’s standalone returns, but to add to them.

The company has already secured six national union jobs-for-life agreements, removing one of the primary objections to regulatory approval.

The near-term risk is regulatory timeline.

The STB directed Union Pacific and Norfolk Southern on March 18 to submit additional information, pushing the revised application to April 30.

Merger-related costs of approximately $30 million per quarter are running through the income statement, and share repurchases of $4 billion to $5 billion annually have been paused to conserve cash ahead of the deal close.

For investors with a 12-to-18-month horizon, that pause removes a meaningful EPS support mechanism.

For investors with a multi-year view, it is a temporary friction in front of a transaction that management believes will take 24 to 48 hours off every interchange movement in the combined network.

Should You Invest in Union Pacific Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up UNP stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Union Pacific Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze UNP stock on TIKR for Free →