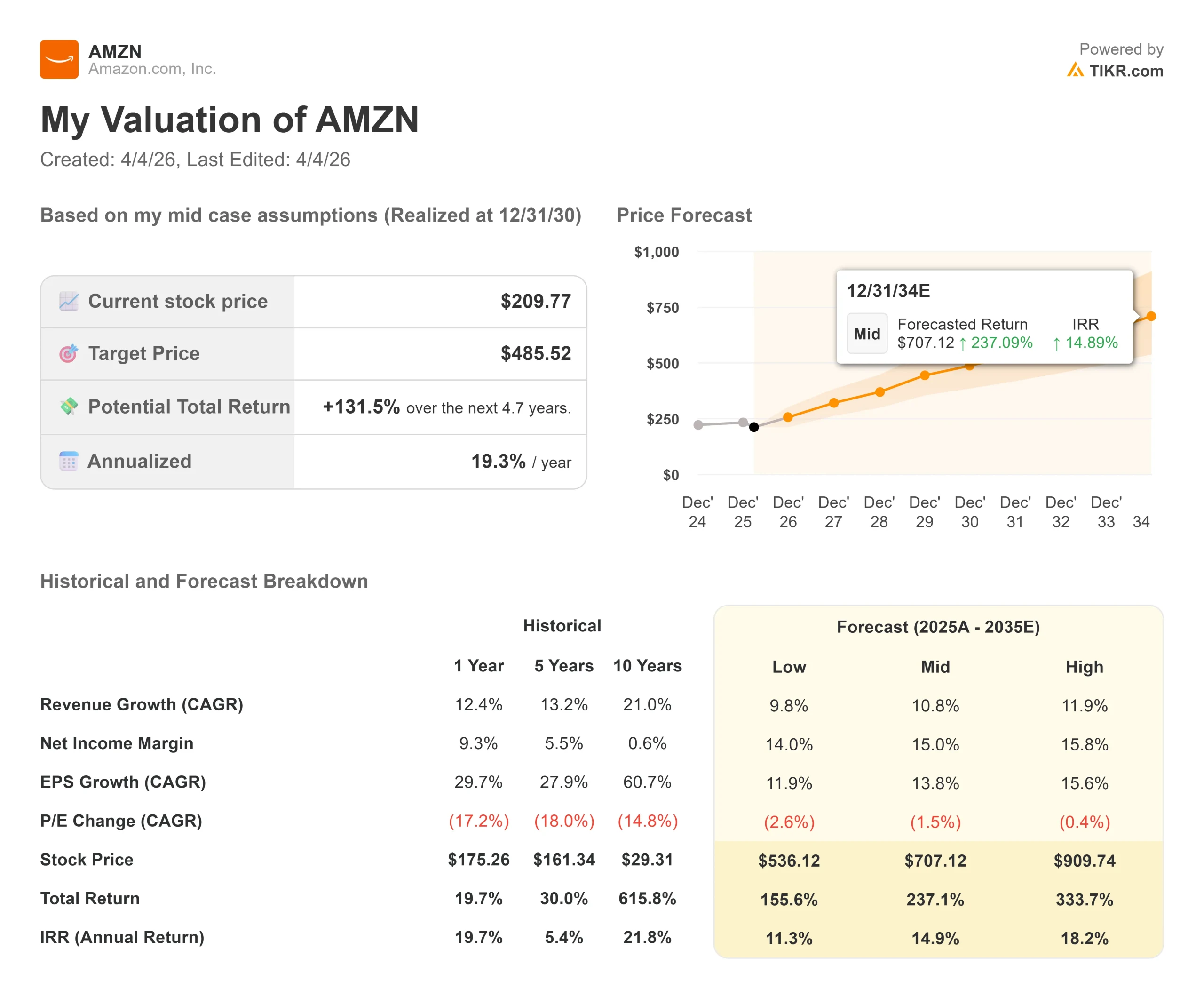

Key Stats for Amazon Stock

- Current Price: $209.77

- TIKR Mid-Case Target: $485.52

- Potential Total Return (Mid): +131.5%

- Annualized IRR: 19.3% / year

- Street Target (Mean): $281.27

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Amazon (AMZN) stock has lost 21.74% from its 52-week high of $258.60, and the question investors are asking is simple: has the market overcorrected?

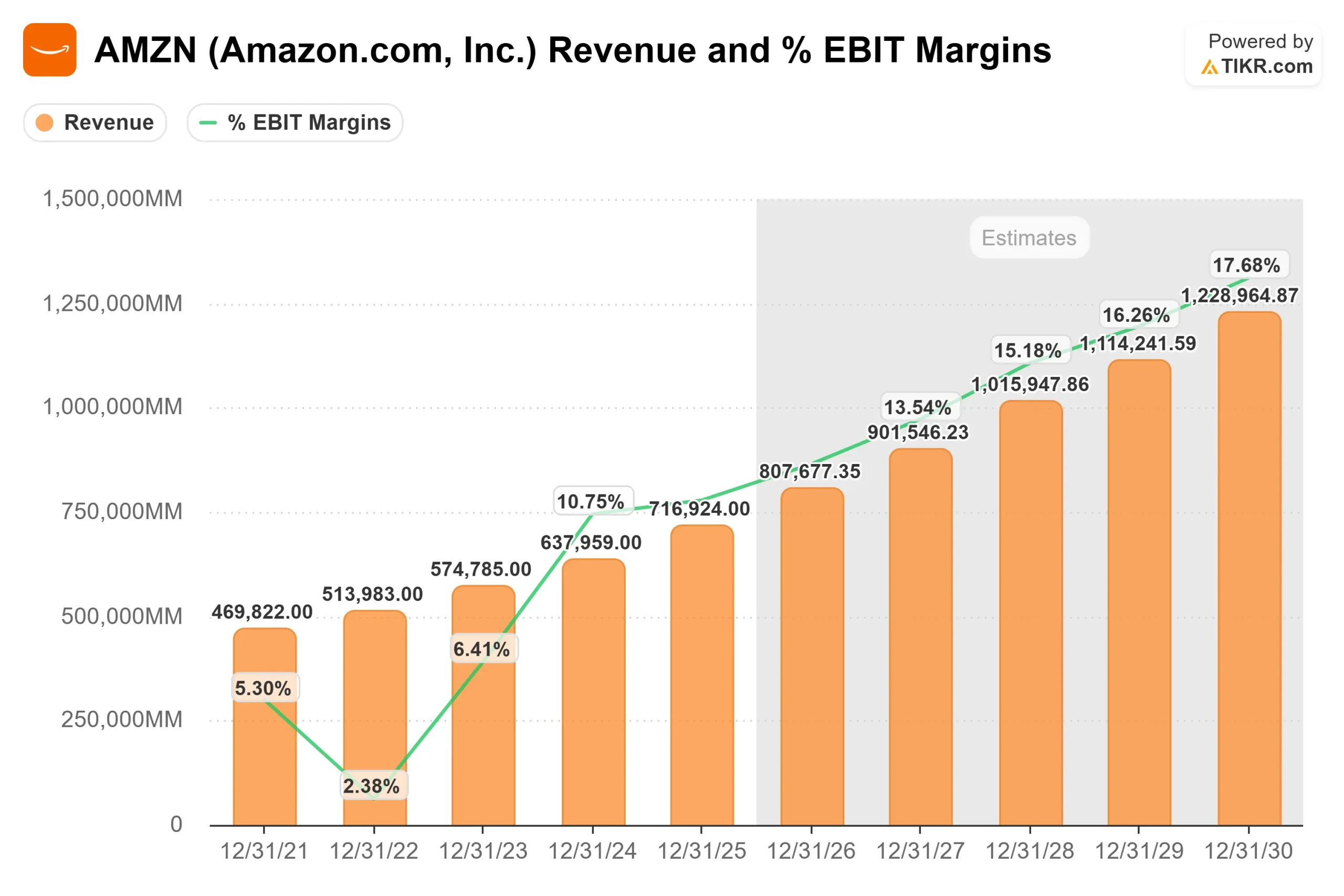

The stock is down roughly 7% year to date, trading near the low end of its own recent valuation history despite reporting $716.9 billion in annual revenue, with its cloud segment growing at the fastest pace in over three years.

The catalyst was Amazon’s Q4 2025 earnings, reported February 5, 2026. Revenue beat at $213.4 billion versus the $211.4 billion estimate, and AWS (Amazon Web Services, the company’s cloud division) grew 24% year over year to $35.6 billion.

EPS came in at $1.95 against a $1.97 consensus, and the announcement of a $200 billion capex (capital expenditure, meaning infrastructure investment) budget for 2026 triggered an immediate selloff. The stock fell 5.55% on the day and reached its max drawdown of 21.74% on February 13.

In Amazon’s investor relations materials, CEO Andy Jassy stated: “With such strong demand for our existing offerings and seminal opportunities like AI, chips, robotics, and low-earth orbit satellites, we expect to invest about $200 billion in capital expenditures across Amazon in 2026, and anticipate strong long-term return on invested capital.”

Two developments this week added to the narrative.

Amazon announced a 3.5% fuel and logistics surcharge on third-party sellers effective April 17, and the Financial Times reported Amazon is in advanced talks to acquire Globalstar for approximately $9 billion to accelerate its Project Kuiper satellite internet initiative against SpaceX’s Starlink.

See historical and forward estimates for Amazon stock (It’s free!) >>>

Is Amazon Undervalued Today?

At a NTM P/E of 27.08x and NTM EV/EBITDA of 10.96x, Amazon is trading near S&P 500 average multiples, pricing in little of the structural advantages in its two highest-margin businesses.

The bull case rests on three engines.

AWS generated $128.7 billion in 2025 revenue with $45.6 billion in operating income at a 35.4% segment margin, and its contracted backlog stood at $244 billion at year-end per Amazon’s Q4 2025 earnings release.

Advertising grew 22% in Q4 2025 to $21.3 billion in quarterly revenue at high incremental margins. North America retail operating income expanded from a loss in 2022 to $29.6 billion in 2025.

Analysts project 2026 revenue at $807.7 billion and 2027 at $901.5 billion, a two-year forward CAGR of 12.1%.

The bear case is equally clear.

LTM levered free cash flow stands at $41.55 billion, but the NTM estimate is ($18.56 billion) as the $200 billion capex commitment runs well ahead of near-term monetization.

Tariff headwinds are real: Amazon has acknowledged active discussions with vendors about pricing adjustments tied to Chinese import tariff changes, and the elimination of the de minimis rule (which previously allowed low-value overseas shipments to enter the U.S. with minimal customs friction) has raised costs across its third-party marketplace.

Azure and Google Cloud are both gaining ground in AI workloads, putting pressure on AWS to sustain growth at scale.

See how Amazon performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $209.77

- TIKR Mid-Case Target: $485.52

- Potential Total Return: +131.5%

- Annualized IRR: 19.3% / year

See analysts’ growth forecasts and price targets for Amazon stock (It’s free!) >>>

The TIKR mid-case model assumes a 10.8% revenue CAGR, driven by AWS AI infrastructure demand and advertising growth, with net income margin expanding to 15.0% from the current LTM level of 10.8% as the capex cycle matures. The high case (11.9% revenue CAGR, 15.8% net income margin) implies meaningfully greater upside. The downside risk is straightforward: if AWS growth decelerates faster than modeled and free cash flow compression extends beyond 2026, multiple contractions could delay or derail the path to the mid-case target. The Q1 2026 operating income guidance of $16.5 billion to $21.5 billion, which came in below the Street’s $22.2 billion consensus, is the most immediate pressure point for that scenario.

Conclusion: Watch AWS revenue growth rate at Q1 2026 earnings on April 29. Sustained growth at or above 20% keeps the margin expansion thesis intact. A print below 20% will force a reassessment of the valuation framework built around AWS acceleration. At 27.08x forward earnings with a $244 billion cloud backlog and a Street mean target of $281.27, the current price appears to reflect more pessimism than the business fundamentals warrant, but April 29 is the first real test.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Amazon?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Amazon, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Amazon alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!