Key Stats for FedEx Stock

- 52-Week Range: $194.3 to $392.9

- Current Price: $361.6

- Street High Target: $479

What Happened?

FedEx Corporation (FDX), the global parcel and freight delivery network, just delivered its most profitable peak season in company history, raising its fiscal 2026 adjusted EPS guidance to $19.30-$20.10 from $17.80-$19.00 while trading at $361.63.

On its March 19 Q3 earnings call, FedEx reported quarterly revenue of $24B, up 8.1% year-over-year, with adjusted EPS of $5.25 beating the $4.14 analyst consensus by 27%, even as its MD-11 cargo fleet remained grounded following a November 2025 crash that triggered a Federal Aviation Administration safety halt.

The Express segment, which delivers time-sensitive shipments at premium pricing and generates FedEx’s highest operating margins, drove the beat through 5% U.S. domestic package volume growth, 5% domestic yield expansion, and 14% international priority freight revenue growth tied to the Tricolor air network strategy, a redesign that routes premium, deferred, and partner cargo across three color-coded systems to maximize load factors.

CEO Raj Subramaniam stated on the Q3 FY2026 earnings call that “this peak season is the most profitable peak in FedEx history,” directly attributing the result to improved forecasting discipline, stronger revenue quality management, and early gains from Network 2.0, the multi-year effort to combine the legacy Express and Ground delivery operations into one unified surface network.

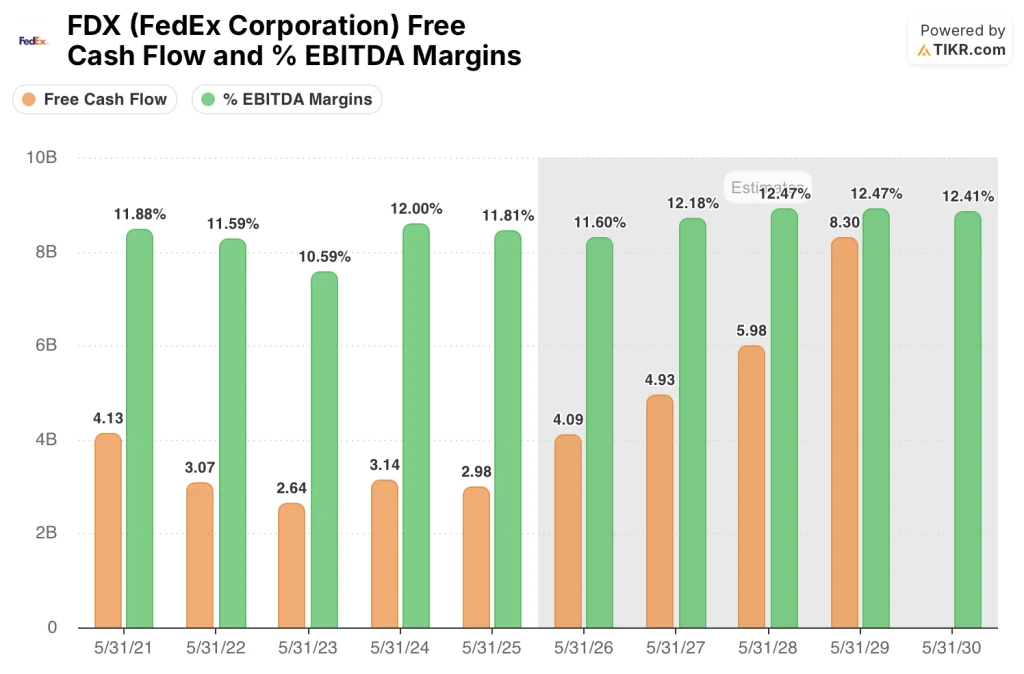

Network 2.0 and the planned June 1 spin-off of FedEx Freight, which handles large trucking shipments and will become a standalone public company, represent the twin structural catalysts that management expects to generate $2B in cumulative savings by end of 2027 and $6B in adjusted free cash flow by fiscal 2029, up from an estimated $4.09B in fiscal 2026.

Wall Street’s Take on FedEx Stock

FDX’s Q3 beat resets the earnings baseline at a structurally higher level, and the raised guidance forces analysts to model a company that is compounding profitability even against an MD-11 headwind worth $120M in the quarter and up to $55M more in Q4.

FDX’s free cash flow inflection is the clearest proof the transformation is working: TIKR estimates FCF nearly triples from $2.98B in fiscal 2025 to $8.30B by fiscal 2029, with FCF margins expanding from 3.4% to 7.8% as Network 2.0 savings compress the cost base faster than revenue grows.

EBITDA margins tell the same story one level up: FDX’s EBITDA margin holds at 11.6% in fiscal 2026 before expanding to 12.5% by fiscal 2028 and holding there through fiscal 2029, signaling that the cost reductions flowing through Network 2.0 and the Freight spin are structural, not cyclical.

Nineteen analysts rate FDX a buy or outperform against nine holds and two sells, with a mean price target of $402.57 implying 11.3% upside from current levels; the bull case at $479 reflects full credit for the Freight spin, Network 2.0 completion, and Europe margin recovery.

Wells Fargo at $450 and TD Cowen at $426 anchor the high end of the range around the Express unit’s sustained volume and pricing outperformance, while Morningstar at $272 fair value anchors the low end on concerns that rising oil prices and Middle East disruption will compress demand before the transformation delivers.

Trading at roughly 18.4x forward earnings versus UPS at 14.6x, FDX commands a meaningful premium to its nearest peer, yet the gap reflects a fundamentally different earnings trajectory: TIKR’s model projects normalized EPS growing at roughly 15% annually through fiscal 2029 versus UPS’s flat-to-declining profile, leaving FDX fairly valued relative to the growth differential despite the premium multiple.

FedEx’s Financials: Margin Expansion in Motion

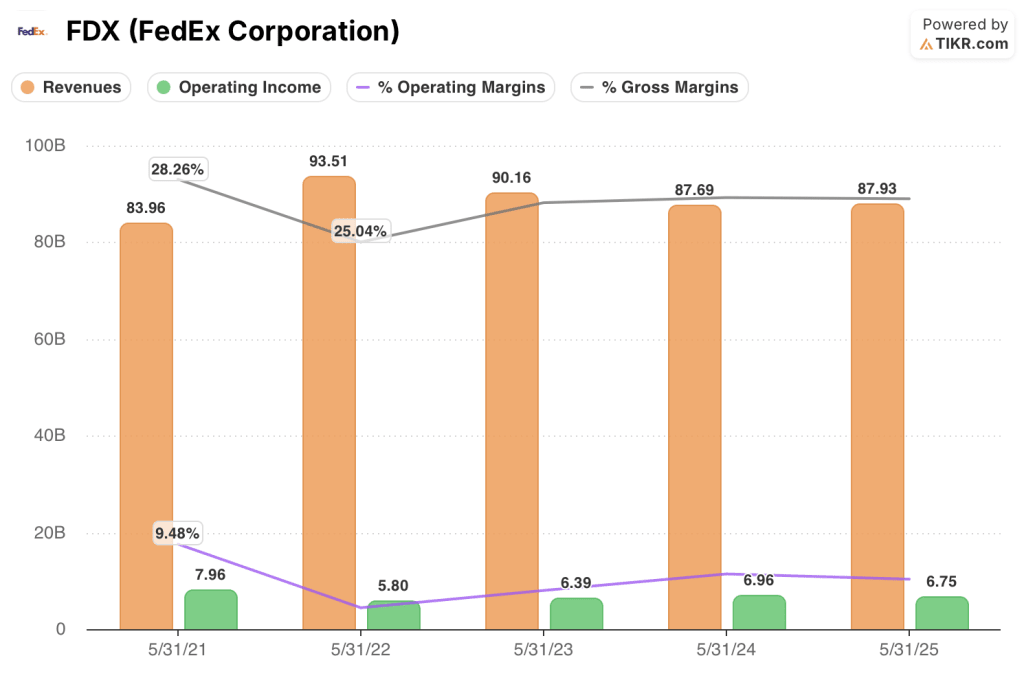

FDX’s operating income has recovered from a post-peak low of $5.80B in fiscal 2022 to $6.75B in fiscal 2025, with operating margins tracking the same arc from 6.2% back toward the 7.9% level last seen in fiscal 2021.

The gross margin recovery from 25.0% in fiscal 2022 to 27.3% in fiscal 2025 signals that FDX’s revenue quality strategy, anchored in B2B mix shift and yield discipline, is already flowing through the income statement ahead of the full Network 2.0 buildout.

Revenue inflected in fiscal 2026 after two consecutive years of contraction, with TIKR estimating $93.47B this year and $106.26B by fiscal 2029, as B2B vertical growth in healthcare, automotive, aerospace, and data center logistics replaces the low-margin B2C volume FDX has been deliberately shedding.

What Does the Valuation Model Say?

The TIKR mid-case target of $497.14 assumes a 4.7% revenue CAGR and 11.3% normalized EPS CAGR through May 2030, with operating margins expanding toward 12.5% as Network 2.0 densification, Tricolor load factor gains, and Europe’s structural cost reductions compound simultaneously.

FDX appears undervalued at current levels, with the TIKR model implying 37.5% total return over 4.1 years at a 7.9% IRR, while the stock still trades 8% below its 52-week high of $392.86.

Moreover, Iran war-driven fuel cost inflation and consumer demand softening remain the model’s primary vulnerability; if oil sustains above $100 a barrel, customers trading down from premium Express services would directly erode the yield growth that drives the entire earnings bridge.

The June 1 FedEx Freight spin-off is the near-term catalyst to watch: a clean separation that isolates the trucking business as its own public entity removes the earnings drag from Freight’s challenged LTL volume and puts FDX’s higher-margin domestic and international package operations into sharper focus for institutional investors.

Should You Invest in FedEx Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up FDX stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track FedEx Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze FDX stock on TIKR for Free →