Key Stats for Marriott Stock

- 52-Week Range: $205.4 to $370

- Current Price: $331.9

- Street High Target: $415

What Happened?

Marriott International (MAR), the world’s largest hotel operator with nearly 1.78 million rooms across 9,800+ properties, is navigating a bifurcated demand environment where record luxury growth and a 35% co-branded credit card fee surge are being offset by a UK antitrust probe and soft U.S. government travel, keeping the stock at $331.93 — well below its February record high of $363.54.

On February 10, Marriott reported Q4 2025 adjusted EPS of $2.58, missing the $2.61 consensus estimate, while total gross fee revenues grew 7% to $1.4 billion and full-year adjusted EBITDA rose 8% to $5.38 billion, ahead of expectations.

The headline catalyst for 2026 is a projected 35% jump in co-branded credit card fees — loyalty-linked products that collect royalties from card partners like Chase and American Express — driven by both a renegotiated royalty rate and continued high-spend growth across Marriott’s 34-card, 11-country Bonvoy program, which now counts 271 million members.

Anthony Capuano, President and CEO, stated on the Q4 2025 earnings call that “internationally, there is an almost insatiable demand for luxury,” then tied it directly to Marriott’s record pipeline of 610,000 rooms, of which 10% sit in the luxury tier.

A 610,000-room development pipeline up 6% year-over-year, accelerating net rooms growth guidance of 4.5% to 5%, a FIFA World Cup tailwind of 30 to 35 basis points of global RevPAR, and active AI distribution partnerships with Google and OpenAI collectively define Marriott’s competitive positioning through 2030.

On March 2, the UK’s Competition and Markets Authority launched a probe into whether Marriott, Hilton, and IHG used CoStar’s hotel data analytics tool — a platform that tracks occupancy, average daily rates, and revenue per available room — to share competitively sensitive pricing information that could reduce competition for consumers.

Wall Street’s Take on MAR Stock

The 35% co-branded credit card fee jump is not a one-year event — it is a royalty rate renegotiation that permanently lifts the fee share Marriott collects from Chase and American Express on every dollar spent across its 271 million Bonvoy members, compounding against a high single-digit growth baseline in card spend.

MAR’s FY2026E adjusted EPS of $11.55 implies 15.2% growth over FY2025’s $10.02, supported by gross fee revenue guidance of $5.9 billion to $5.96 billion — a range made credible by Marriott’s record 610,000-room pipeline, a 35% credit card royalty uplift from the Bonvoy renegotiation, and over $4.3 billion in planned share buybacks compressing the denominator further.

The bull case rests on three compounding drivers:

- co-branded credit card fees accounted for 13% of gross fees in FY2025 and are guided to reach 16% in FY2026 and approximately 17% in FY2027, according to JP Morgan, a royalty rate renegotiation that functions more like a permanent margin expansion than a one-time gain;

- gross fee revenue guided to rise 8% to 10% in 2026, with adjusted EPS growth projected at 13% to 15%, materially above the revenue growth rate, reflecting operating leverage and a meaningful reduction in share count from over $4.3 billion in planned capital returns;

- and Jefferies raising its FY2026 lodging revenue estimate to $7.62 billion following the Q4 print, citing pipeline momentum with over half of the 610,000-room pipeline located internationally, where RevPAR growth continues to outpace the U.S.

The bear case is less about fundamentals and more about macro sensitivity and regulatory overhang, with the CMA probe into hotel data-sharing with CoStar introducing tail risk on pricing practices in the UK and potentially continental Europe, Morgan Stanley cutting hotel price targets in March citing a cautious macro outlook, government RevPAR already down over 30% during the 43-day U.S. government shutdown remaining a structural drag on domestic select-service properties, and Greater China RevPAR guided flat year-over-year amid continued weak consumer sentiment.

Eleven analysts rate MAR a Buy, 1 an Outperform, 13 a Hold, 1 an Underperform, and 1 a Sell at the March 31 snapshot, with a mean target of $356.12 implying 7.3% upside from $331.93 — a muted consensus that largely excludes the potential Chase and American Express contract renewals currently stripped from guidance entirely.

The target spread between Jefferies at $415 and the bear end at $269 captures a real disagreement: whether the royalty renegotiation represents durable structural earnings or a pull-forward that compresses future upside once the new credit card deals are signed and normalized.

Marriott International Financial Performance

Marriott’s gross fee revenues rose 5% in FY2025 to $5.4 billion, with operating income expanding 7.7% to $4.14 billion and operating margins holding at 59.3%, consistent with the prior year’s 58.1% trough recovery after a 2024 dip.

The margin stability is notable given the $90 million in above-property cost savings from Marriott’s enterprise productivity initiative, which compressed SG&A from $1.94 billion in FY2024 to $1.87 billion in FY2025 even as the company added over 700 properties net to its system.

Forward estimates project revenue climbing from $26.19 billion in FY2025 to $27.91 billion in FY2026, with EBITDA margins expanding from 20.6% to 21.1%; a trajectory that supports the 8% to 10% adjusted EBITDA guidance range of $5.8 billion to $5.9 billion for the year.

The primary financial tension is gross margins, which compressed from 79.9% in FY2024 to 79.1% in FY2025 and have been flat to declining since the 2022 post-COVID peak of 79.9%, signaling that cost of revenues is growing slightly faster than fee revenues — a dynamic worth monitoring as World Cup and AI tech investments ramp in 2026.

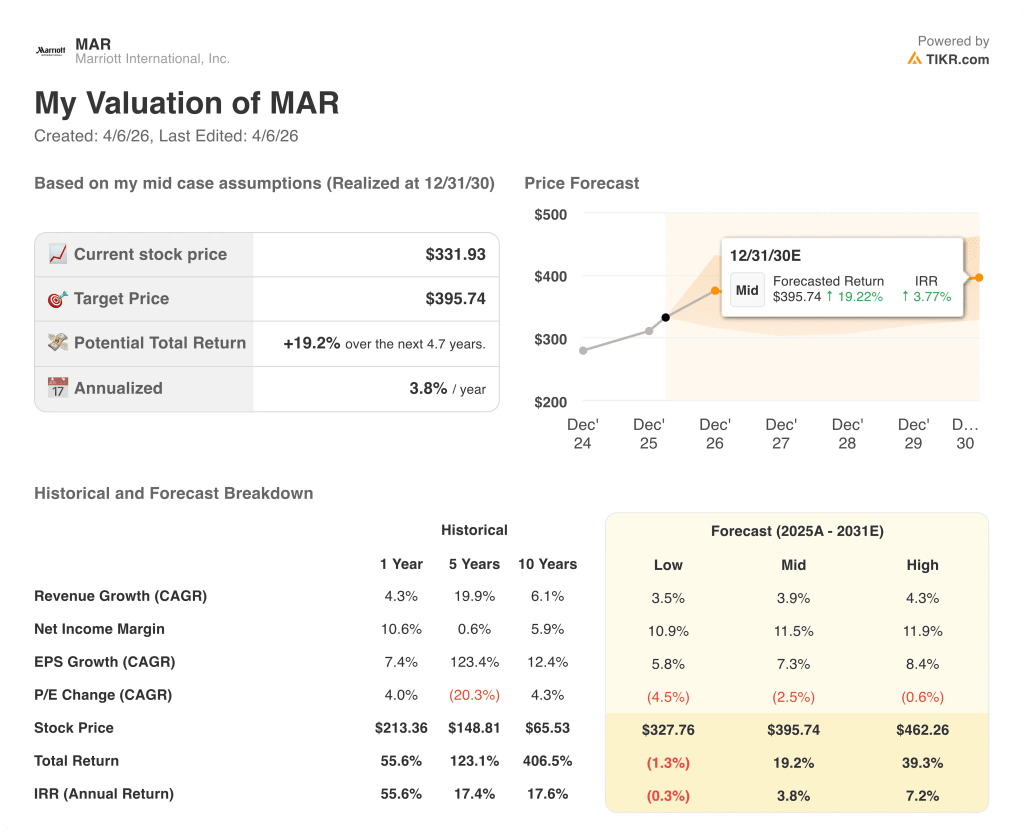

What Does the Valuation Model Say?

The TIKR model assigns a mid-case target of $395.74 by December 2030, built on a 7.3% EPS CAGR and modest P/E compression of 2.5% per year — a return profile anchored by the Bonvoy royalty rate lift and 4.5% to 5% net rooms growth, not multiple expansion.

MAR appears modestly undervalued at current levels, trading at 28.7x FY2026E EPS while the TIKR mid-case delivers 19.2% total return through earnings growth alone, with no re-rating required to hit $395.74.

Priced at 28.7x forward earnings against 15.2% EPS growth in 2026 and a PEG ratio well below 2.0x, MAR’s current multiple does not yet reflect the structural fee stream shift from the Bonvoy royalty renegotiation or the World Cup RevPAR tailwind, leaving MAR moderately undervalued relative to its own near-term earnings trajectory.

If the Middle East conflict expands beyond the region or oil-driven flight costs materially soften international inbound demand, the 30 to 35 basis point World Cup RevPAR contribution evaporates and government travel weakness could deepen further.

When Q3 earnings report, watch gross fee revenue against the $5.9 billion to $5.96 billion full-year guide — any upward revision signals the Chase and American Express renewals are tracking ahead of stripped-out guidance assumptions.

Should You Invest in Marriott International, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MAR stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Marriott International, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MAR stock on TIKR for Free →