Key Stats for Pinterest Stock

- 52-Week Range: $13.8 to $40

- Current Price: $18.2

- Street High Target: $45

What Happened?

Pinterest (PINS), the visual discovery and shopping platform that converts browsing intent into advertiser clicks, secured a $1 billion strategic investment from activist firm Elliott Management on March 3 while authorizing $3.5 billion in total share repurchases, signaling a structural reset for a stock sitting 54% below its 52-week high of $39.93.

Elliott’s convertible notes carry an initial conversion price of $22.72 per share, and Pinterest simultaneously committed to $2 billion in near-term buybacks, including an accelerated repurchase program plus $500 million from cash, compressing the float as the company rebuilds its revenue base.

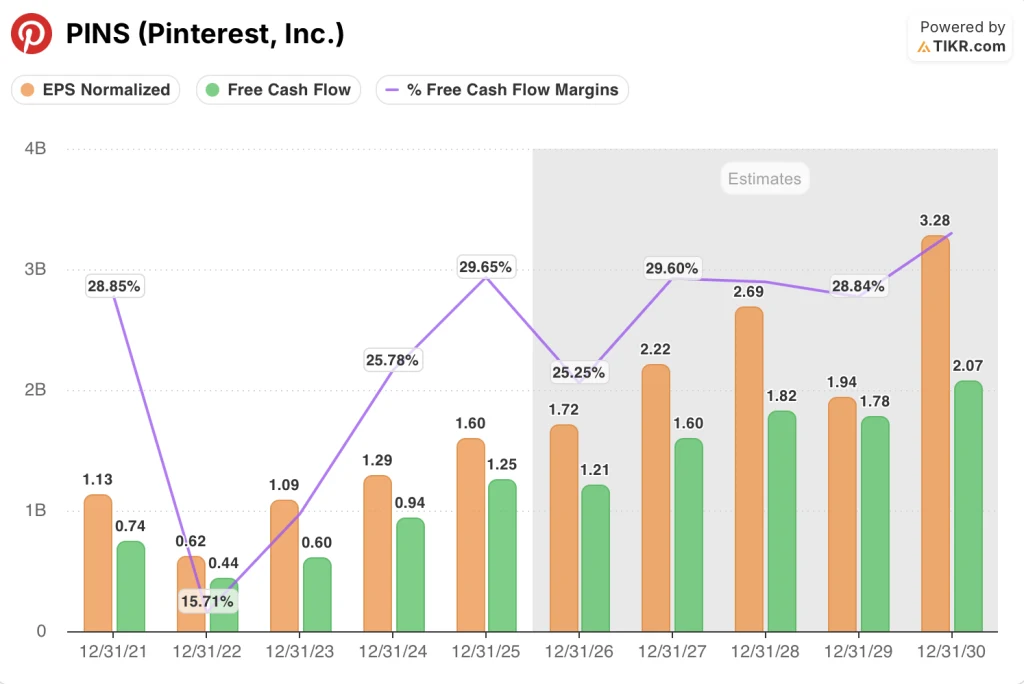

Pinterest closed 2025 with 619 million monthly active users, up 12%, and generated $1.25 billion in free cash flow at a 99% conversion rate, outpacing Snap’s far thinner margin profile, yet Q4 revenue of $1.319 billion missed the $1.329 billion consensus as tariff-pressured large retailers pulled back ad spend disproportionately on Pinterest’s platform.

Bill Ready, Chief Executive Officer, stated on the Q4 2025 earnings call that “we’ve taken Pinterest from a platform with declining users into a growing, AI-powered, visual-first shopping assistant and search destination that has now put up 10 straight quarters of record high users,” anchoring the long-term user thesis against the near-term revenue miss.

Elliott’s capital commitment, combined with the tvScientific acquisition, which folds connected-TV performance advertising into Pinterest’s platform and closed February 18, and the appointment of Chief Business Officer Lee Brown to lead the company’s go-to-market overhaul, gives Pinterest three simultaneous levers targeting durable mid-to-high-teens revenue growth and a 30% to 34% adjusted EBITDA margin over the medium term.

Wall Street’s Take on PINS Stock

Elliott’s $1 billion convertible investment, with a conversion price of $22.72, establishes a near-term floor and directly accelerates the $3.5 billion share repurchase program already authorized by Pinterest’s board.

Pinterest’s visual discovery platform generated $1.25 billion in free cash flow in 2025 at a 29.7% margin, and the TIKR model projects normalized EPS climbing from $1.60 in 2025 to $2.22 by 2027 and $3.28 by 2030, supported by the tvScientific CTV expansion and Lee Brown’s go-to-market overhaul.

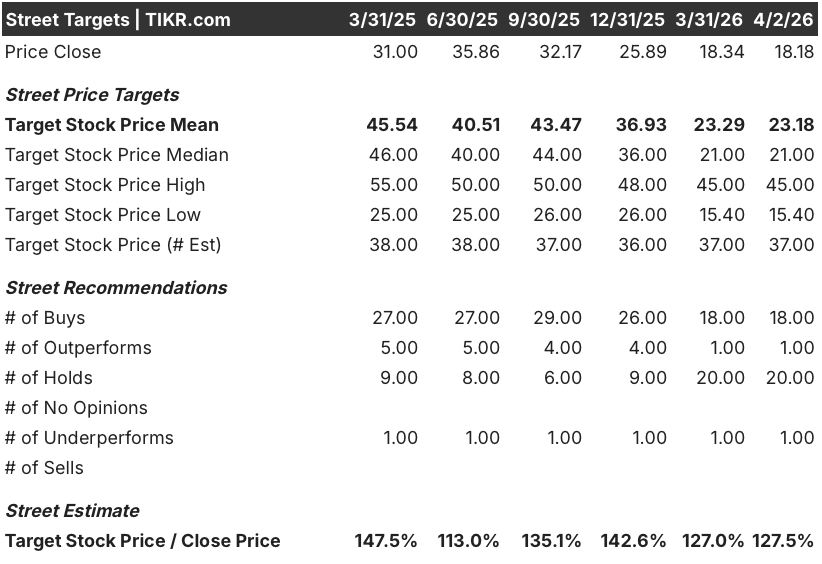

Wall Street’s conviction has narrowed sharply: 18 analysts rate PINS a buy, 1 an outperform, and 20 a hold, with a mean price target of $23.18 against a current price of $18.18, implying 27.5% upside, as analysts await evidence that the sales transformation under Brown converts engagement into accelerating revenue.

The analyst target range runs from $15.40 to $45.00, with the low reflecting continued large-retailer ad pullback and go-to-market disruption, and the high contingent on tvScientific CTV monetization and SMB advertiser penetration scaling beyond the current 15% revenue share.

What Does the Valuation Model Say?

The TIKR mid-case model prices PINS at $45.95 by December 31, 2030, implying a 21.6% IRR, anchored by an 8.8% revenue CAGR and net income margin expansion from 26.1% in 2025 to 35.4% by 2030, driven by the SMB flywheel and connected-TV budget pools from tvScientific.

At 10.6x 2026E normalized EPS of $1.72, PINS trades at a steep discount to its own 3-year historical earnings growth rate of 37.2%, and against a TIKR mid-case EPS CAGR of 18.1% through 2030, PINS stock looks plainly undervalued by any earnings-compounding framework.

The TIKR $45.95 mid-case target finds its clearest real-world anchor in Pinterest’s 80 billion monthly visual searches generating 1.7 billion outbound clicks monthly, a monetization base that Performance+ ROAS bidding and tvScientific CTV inventory are only beginning to convert at scale.

Management’s disclosure that one Performance+ pilot advertiser increased Pinterest bids by more than 30% under value-based optimization confirms the platform’s monetization gap is a measurement problem, not a demand problem.

If large-retailer ad spend deteriorates beyond the second-half anniversary, the TIKR model’s 13.4% revenue growth assumption for 2026 breaks, and FCF compresses from the projected $1.21 billion.

Q1 2026 earnings will test whether revised revenue guidance of $958 million to $978 million holds as the go-to-market restructuring disruption plays out; watch for SMB revenue share moving above 15% as the leading indicator.

Should You Invest in Pinterest, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up PINS stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Pinterest, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze PINS stock on TIKR for Free →