Key Stats for ONEOK Stock

- 52-Week Range: $64 to $95.3

- Current Price: $88.3

- Street High Target: $108

What Happened?

ONEOK, Inc. (OKE) delivered 12 consecutive years of adjusted EBITDA growth in 2025, capping the streak with an 18% full-year gain to $8.02 billion as its diversified midstream network — pipelines that gather, process, and transport natural gas, natural gas liquids, refined products, and crude oil across roughly 60,000 miles — absorbed the integration of four major acquisitions while the stock trades at $88.30.

Jefferies upgraded OKE to “Buy” on March 20, raising its price target to $98 from $85, citing upside from butane blending operations, location-based price spreads, and a projected Bakken volume recovery starting in FY27, even as the brokerage acknowledged near-term volume softness across the Rocky Mountain region.

Underpinning that recovery case, ONEOK captured nearly $500 million in cumulative acquisition synergies since closing the Magellan deal in September 2023, with $250 million of that total realized in 2025 alone, a pace that comfortably outstripped management’s original targets and demonstrates the earnings power of combining adjacent pipeline and fractionation assets.

On the Q4 2025 earnings call, Chief Commercial Officer Sheridan Swords stated that the $150 million of incremental synergies embedded in 2026 guidance are “all identified, and they are in the plan, and they are underway,” directly anchoring the company’s $8.1 billion adjusted EBITDA midpoint to contracted, execution-stage projects rather than speculative upside.

ONEOK’s $2 billion share repurchase authorization, a 4% dividend increase to $1.07 per share announced January 21, and a capital project pipeline stretching from the Medford fractionator rebuild in Q4 2026 through Gulf Coast export terminal phases targeting 2028 collectively position the company to convert its integrated midstream scale into compounding shareholder returns as leverage grinds toward its 3.5x target.

Wall Street’s Take on OKE Stock

The Jefferies upgrade to “Buy” on March 20 crystallizes a directional shift already underway: ONEOK’s four-acquisition integration cycle is closing, and the contracted project pipeline now converts directly into expanding free cash flow.

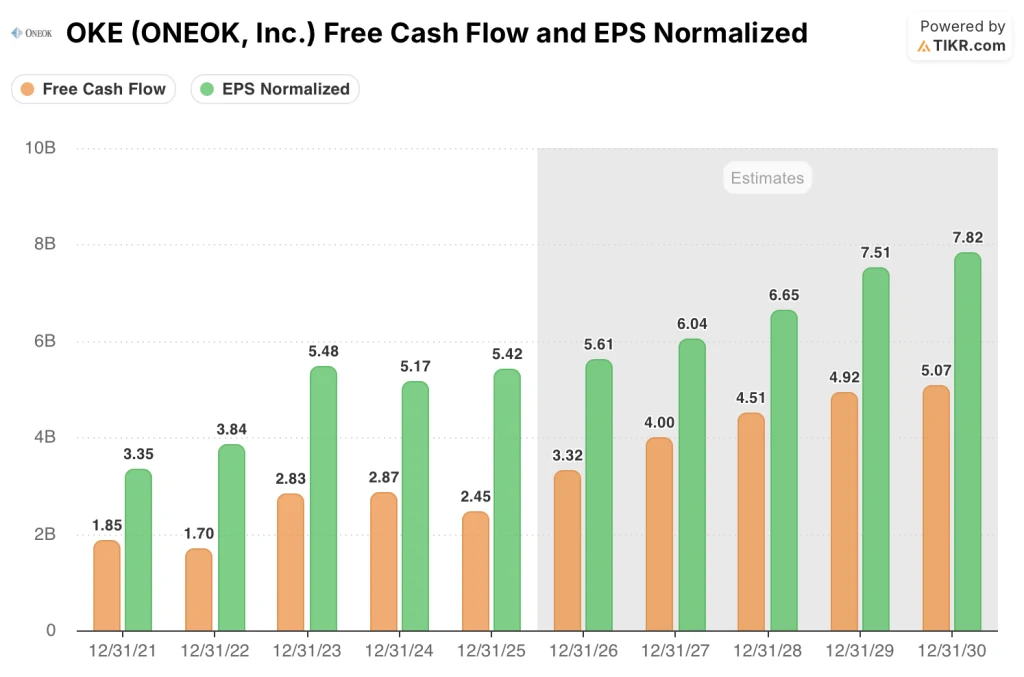

TIKR estimates OKE stock free cash flow surging 35.5% to $3.32 billion in 2026, anchored by the Denver refined products pipeline expansion and Medford fractionator Phase 1 entering service in the second half of this year.

Normalized EPS is also forecast to grow from $5.42 in 2025 to $6.04 by 2027, a trajectory supported by $150 million of already-identified incremental synergies and the full-year contribution of delayed Permian NGL plants that compressed 2025 results.

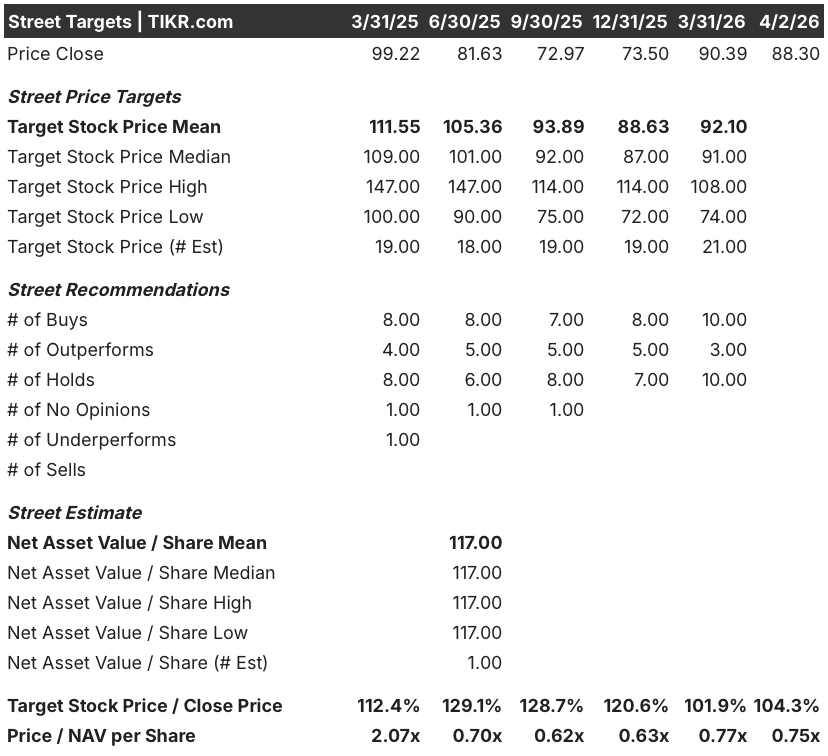

Sentiment has materially tightened since last September, when 19 analysts covered OKE with a mean price target of $93.89 against a $72.97 close; today, 13 of 21 analysts rate the stock “Buy” or “Outperform,” with a mean target of $92.10, implying approximately 4.3% upside to the current $88.30 price.

The spread between the $74.00 low target and the $108.00 high target reflects a genuine binary: bears anchor on the $55–$60 WTI crude oil assumption compressing Bakken drilling activity and narrowing Waha-to-Katy natural gas price differentials, while bulls price in a commodity recovery that accelerates synergy capture and pushes EBITDA above the $8.3 billion guidance ceiling.

What Does the Valuation Model Say?

The TIKR mid-case values OKE at $116.32 by December 2030, embedding a 4.5% normalized EPS CAGR and a free cash flow margin expanding from 7.3% in 2025 to 10.0% in 2026, driven by the capex step-down management has explicitly guided as large projects complete.

OKE stock trades at roughly 10.7x forward EBITDA of $8.26 billion, a discount to the 11x–12x range where scaled, fee-based midstream infrastructure peers with comparable earnings stability have historically traded; ONEOK stock is undervalued relative to that benchmark given that 90% fee-based earnings and $500 million of confirmed synergies make the 2026 EBITDA estimate unusually high-confidence.

The TIKR model’s $116.32 target is justifiable specifically because Eiger Express Pipeline capacity is now 100% contracted for a minimum of 10 years at 3.7 Bcf per day, providing the long-duration revenue visibility that mid-case models require.

Management’s confirmation that all $150 million of 2026 synergies are “identified and in the plan” removes the most common execution discount applied to post-acquisition infrastructure stories.

The model breaks if WTI crude falls sustainably below $55, triggering further Bakken rig reductions and compressing the volume growth that drives the 2027 EBITDA step to $8.60 billion.

The April 28 Q1 2026 earnings release is the first confirmation gate: watch reported adjusted EBITDA against the implied $1.98 billion quarterly run-rate, and monitor whether Permian NGL plant connections are tracking the three confirmed 2026 hook-ups management committed to on the February call.

Should You Invest in ONEOK, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up OKE stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track ONEOK, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze OKE stock on TIKR for Free →