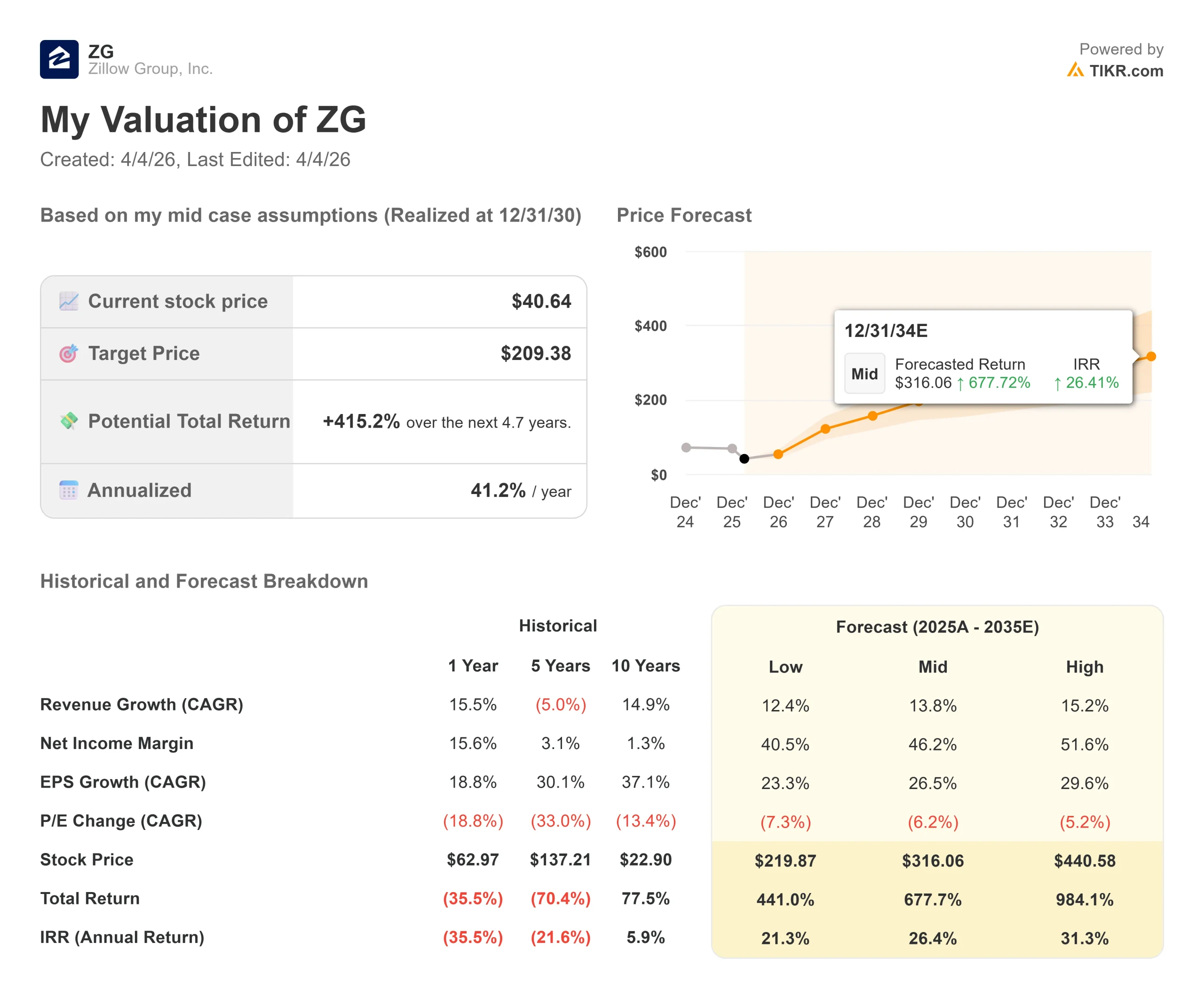

Key Stats for Zillow Stock

- Current Price: $40.64

- Target Price (Mid): $209.38

- Street Target: $73.83

- Potential Total Return: +415.2%

- Annualized IRR: 41.2% / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Few consumer internet stocks have been punished as quickly as Zillow (ZG). The stock fell 17.13% on February 10, 2026, after reporting Q4 2025 earnings, and has since hit a max drawdown of 53.42% from its recent high as of March 27, 2026. At $40.64, ZG trades just above its 52-week low of $39.14.

The selloff had two triggers.

The first was Zillow’s Q1 2026 adjusted EBITDA guidance of $160 million to $175 million, which missed Street expectations of roughly $183 million, weighed down by rising legal costs.

The second was larger: analysts described the broader selling in real estate service stocks as an “AI scare trade,” driven by investor concern that horizontal AI platforms could disrupt Zillow’s marketplace model.

That fear intensified when reports emerged that Google was testing a mobile-focused real estate format integrating property listings directly into search results, with a “Request a tour” button connecting users with local agents.

Multiple firms, including BofA, UBS, Mizuho, Baird, and Piper Sandler, reduced their price targets, citing concerns around valuation, competitive intensity, and evolving housing market structure.

Zillow’s response was a two-hour AI Investor Summit in New York City on March 24, 2026, the company’s first investor day since 2013. CEO Jeremy Wacksman made the strategic case directly: “Just like the last change everything moment with the mobile revolution, Zillow is leaning in and leading where AI is going in real estate.”

The stock gained approximately 1% on the day.

The more important question is whether what Zillow demonstrated actually resolves the bear thesis.

See historical and forward estimates for Zillow stock (It’s free!) >>>

Is Zillow Undervalued Today?

A frozen housing market, elevated mortgage rates, litigation overhang, and the theoretical threat of AI-driven top-of-funnel disruption have all compressed the multiple sharply.

The bull case starts with what most investors have not seen: the depth of Zillow’s operational footprint inside the transaction itself.

ShowingTime powers tour scheduling for 90% of all listings in the United States, with 40 million home tours booked through it in the past year.

Follow Up Boss is used by 41 of the top 50 real estate teams in the country. Dotloop is involved in more than 50% of all home closings in America.

These are not consumer-facing features. They are the infrastructure of the transaction, and a horizontal AI platform cannot replicate them by training on public data.

At the summit, CFO Jeremy Hofmann stated that Zillow grew revenue by approximately 33% and EBITDA by approximately 59% from 2023 to 2025, while the housing market grew only roughly 3% in 2025, approximately 1,300 basis points of outperformance.

That is not what a disrupted business looks like.

The rentals segment is a separate growth driver.

Rentals revenue has grown 130% since 2022. Zillow has nearly tripled its multifamily advertiser count from 28,000 in 2022 to more than 72,000 by the end of Q4 2025. Since launching its payments product, Zillow has processed more than $10 billion in rent on the platform, with year-over-year payment volume up approximately 20% as of February 2026.

On peers, Newmark Group trades at approximately 1.31x NTM EV/Revenue and 7.41x NTM EV/EBITDA, and Colliers International at approximately 1.37x and 10.44x.

Zillow’s premium is real but reflects a different business: a technology platform with 41.7% LTM gross margins and software embedded across professional workflows.

The relevant question is whether a company on a path to 45% EBITDA margins and 25% net income margins at mid-cycle deserves to trade near a multi-year low.

The AI Mode product debuted at the summit, linking conversational AI to Zillow’s proprietary inventory, BuyAbility financial profiles, real-time ShowingTime tour availability, and Zillow Home Loans prequalification.

A user asking whether they can afford a specific home gets an answer built from their own financial data already stored in the platform. A generic LLM cannot replicate that without Zillow’s closed-loop data infrastructure.

On capital allocation: CFO Hofmann confirmed at the summit that Zillow repurchased over $625 million of stock in Q1 2026 alone. Zillow’s board also added $1.25 billion to its repurchase authorization, bringing total remaining buyback capacity to approximately $1.3 billion.

Co-founder Rich Barton disclosed personal stock purchases in the weeks before the summit.

See how Zillow performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $40.64

- Target Price (Mid): $209.38

- Potential Total Return: +415.2%

- Annualized IRR: 41.2% / year

See analysts’ growth forecasts and price targets for Zillow stock (It’s free!) >>>

The TIKR mid-case model targets $209.38 by December 31, 2030, built on a 13.8% revenue CAGR and a 46.2% net income margin. The two primary revenue drivers are continued Rentals scaling, compounding at approximately 30% annually toward the $1 billion segment target, and for-sale transaction monetization deepening through Zillow Home Loans, which grew purchase origination volume by more than 6x from 2022 to 2025. The margin driver is operating leverage on a largely fixed cost base, which Hofmann stated has grown at only approximately 5% annually since 2023, while revenue has compounded well above that rate.

The primary risk to the model is a prolonged housing market freeze. If transaction volumes remain depressed beyond 2027, the 13.8% revenue CAGR becomes harder to sustain. At $40.64, the stock appears to be pricing in a scenario more pessimistic than what the model’s conservative assumptions already reflect.

Conclusion: Watch Rentals revenue at Zillow’s Q1 2026 earnings report, expected May 6, 2026. Management has guided approximately 30% full-year Rentals growth. If Q1 Rentals comes in on track, it removes one of the two key variables suppressing the multiple. Any indication that legal costs peak in 2026 would further improve the path to the 45% EBITDA margin target.

Zillow is a housing recovery bet built on technology infrastructure that has quietly become the operational backbone of the U.S. residential transaction. At 53% off its recent high, the stock is pricing in a permanence of disruption that its own data and platform depth make very difficult to justify.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Zillow?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Zillow, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Zillow alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!