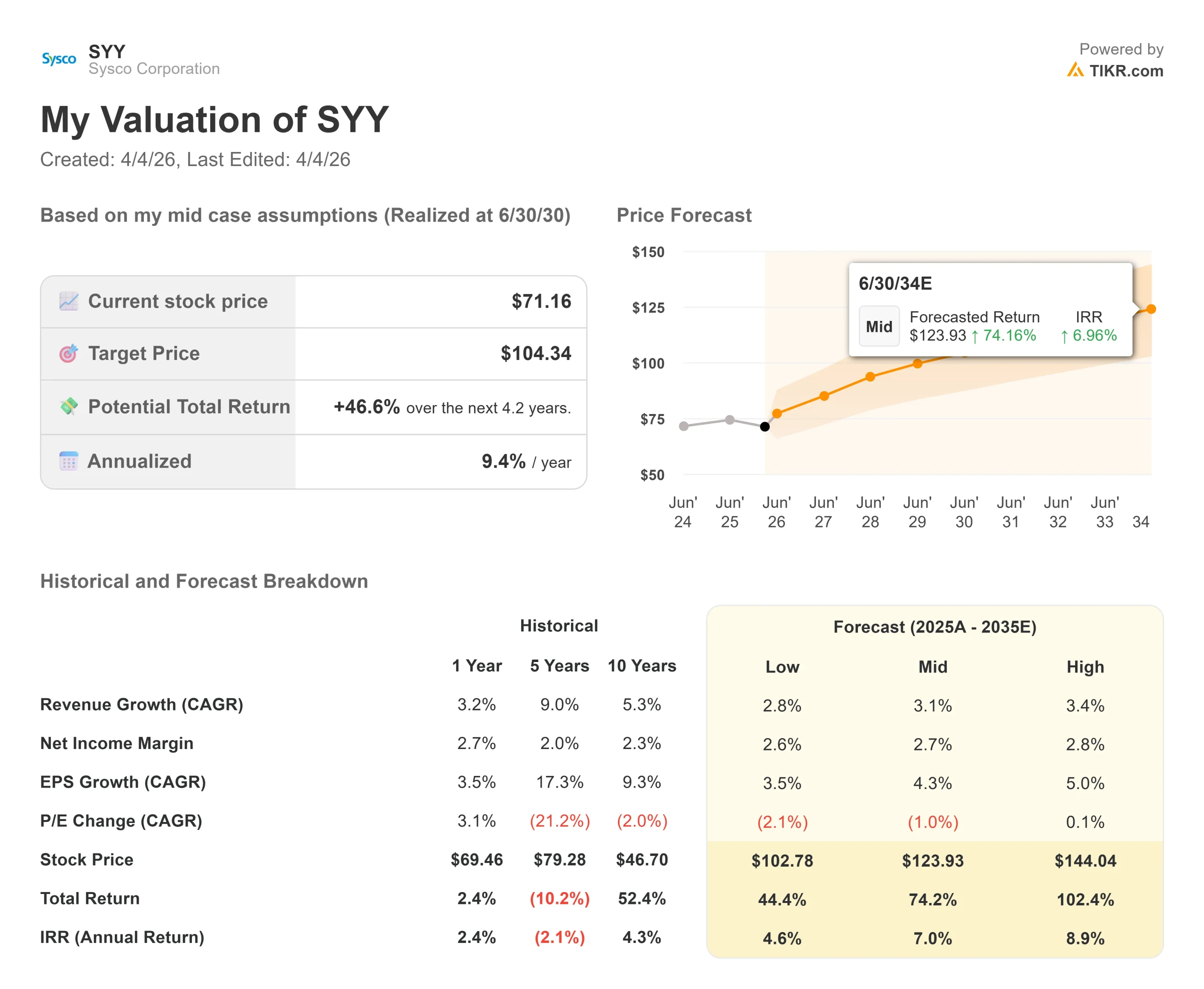

Key Stats for Sysco Stock

- Current Price: $71.16

- Target Price (Mid): $104.34

- Street Target (Mean): $88.47

- Potential Total Return: +46.6%

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

largest in recent history, after announcing a $29.1 billion deal to acquire Jetro Restaurant Depot, the largest cash-and-carry wholesale food supplier in the U.S.

Cash-and-carry refers to a model where restaurant owners drive to a warehouse, select products, and pay on the spot rather than receiving scheduled delivery.

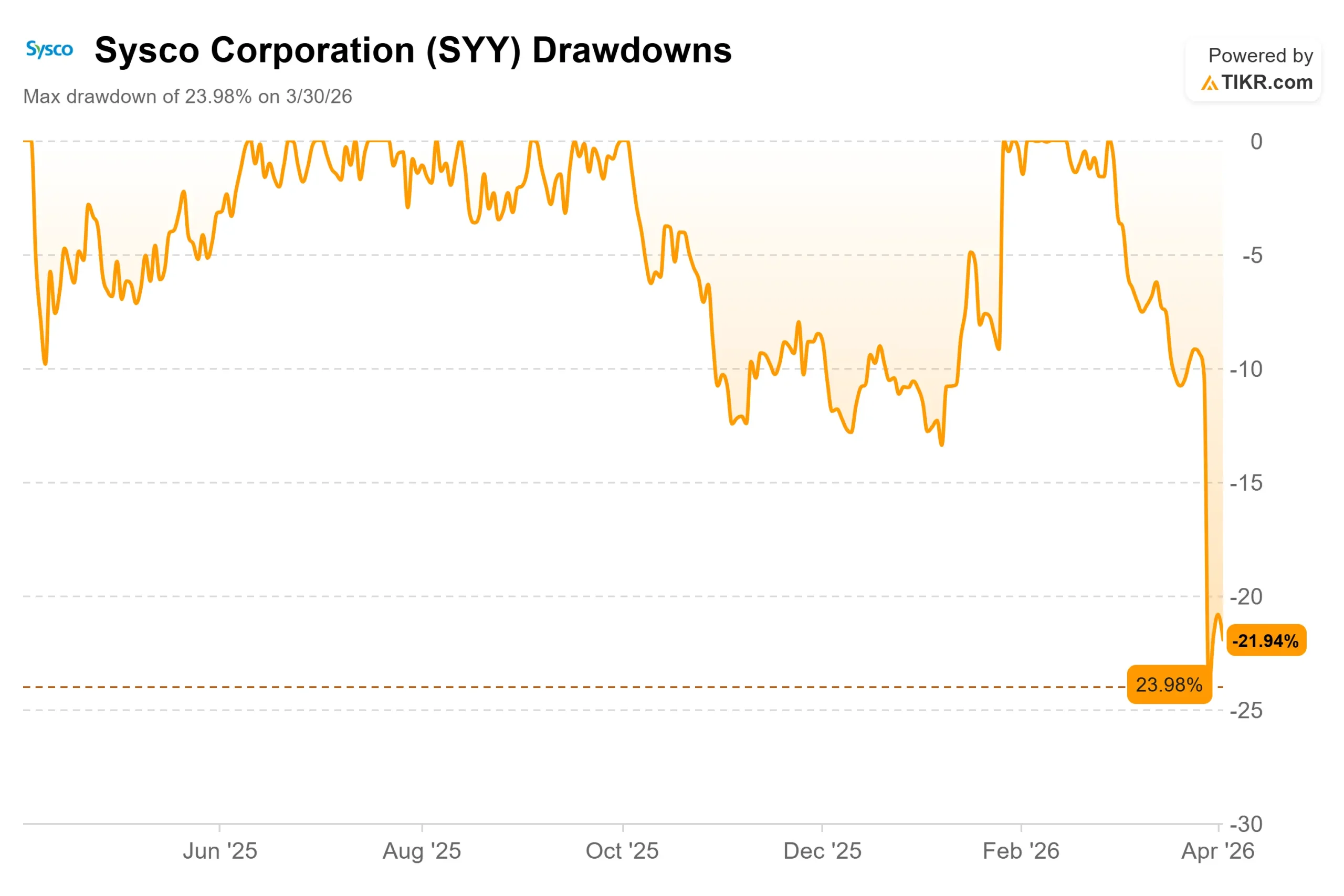

The stock closed at $71.16 on April 2, down from its 52-week high of $91.85 just six weeks earlier.

Bulls say the deal transforms Sysco into a higher-margin, omnichannel food distribution platform. Bears say the company took on $21 billion in new debt at the wrong moment in the cycle. Both are partly right.

The deal is structured as $21.6 billion in cash and 91.5 million Sysco shares for Restaurant Depot, a family-owned business with 166 warehouse locations across 35 states serving more than 725,000 local customers.

Following the announcement, both Fitch placed Sysco on rating watch negative and Moody’s placed its ratings on review for potential downgrade.

The Independent Restaurant Coalition called on the FTC to block the transaction, arguing the deal eliminates the one meaningful wholesale alternative available to small operators.

Kevin Hourican, Chair of the Board and Chief Executive Officer, made the financial case plainly on the deal call: “We expect this combination to significantly enhance Sysco’s financial profile, increasing our revenue by approximately 20%, adjusted EBITDA by approximately 45%, and free cash flow by approximately 55% on a pro forma basis.”

Management argued the two companies serve meaningfully different customers with minimal overlap, since Restaurant Depot’s self-serve, value-seeking shoppers and Sysco’s broadline delivery customers, meaning restaurants and institutions that receive scheduled delivery and pay for consultative sales service, rarely use both channels for the same purpose.

The underlying business was building momentum before this announcement.

Interim CFO Brandon Sewell disclosed on the call that Sysco expects Q3 fiscal 2026 adjusted EPS of approximately $0.94 and U.S. Foodservice local case volume growth of at least 3% year over year, more than 50 basis points above prior guidance, and the fourth consecutive quarter of sequential improvement, up over 600 basis points versus a year ago.

See historical and forward estimates for Sysco stock (It’s free!) >>>

Is Sysco Undervalued Today?

Restaurant Depot generated approximately $16 billion in revenue and $2 billion in EBITDA in calendar 2025 at a 13% EBITDA margin, well above Sysco’s current standalone LTM EBIT margin of 4.3%.

The combined company is expected to carry a pro forma EBITDA margin of approximately 6.7%, a 150 basis point step-up. Restaurant Depot also generated $1.9 billion in free cash flow in 2025 at a conversion rate above 90%, with capital expenditures of just $136 million, or 7% of its EBITDA.

Adding that free cash flow generation to Sysco’s balance sheet changes the capital allocation picture materially within a few years of close. Management guided for more than $2 billion in additional annual free cash flow in the long term.

The cash-and-carry channel itself is a genuine growth asset.

The segment represents a $60 billion to $70 billion total addressable market where Sysco had zero share before this deal. Restaurant Depot grew its revenue in 28 of the last 30 years and its profit in all 30, including through COVID. The business also tends to gain share during downturns, as value-seeking operators shift toward lower-cost self-service purchasing.

The debt is a legitimate concern.

Net leverage rises from 2.81x to approximately 4.5x at close. Sysco has paused its buyback and targets reducing leverage by at least 1x within 24 months post-close, with a long-term target of approximately 2.75x. That path requires clean execution.

A prolonged regulatory review, a macro slowdown, or a slower synergy ramp would extend the deleveraging timeline.

The $250 million in annualized cost synergies, concentrated in procurement scale and private label optimization, are expected within three years. Hourican was explicit that the companies will avoid deep technology integration, protecting each company’s culture and limiting integration risk.

The comparison investors are drawing is to US Foods and its Chef’s Store operation.

US Foods acquired Chef’Store in 2020 and announced plans to sell it in 2024, citing limited operational benefits. The scale is different here: Restaurant Depot is a $2 billion EBITDA business being added to a company with $4.5 billion in LTM EBITDA, a far more significant combination.

Still, Sysco is a logistics business integrating what functions as a retail operation, and the cultural and operational gap is real.

See how Sysco performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $71.16

- Target Price (Mid): $104.34

- Potential Total Return: +46.6%

- Annualized IRR: 9.4% / year

See analysts’ growth forecasts and price targets for Sysco stock (It’s free!) >>>

The TIKR mid-case model targets $104.34 by June 30, 2030, implying a 46.6% total return and a 9.4% annualized IRR from the current price of $71.16. This IRR is calculated to the 6/30/30 target date. The model’s longer-horizon IRR over the full 2025 to 2035 forecast period is 7.0% annually. The two primary revenue growth drivers are continued organic volume gains in Sysco’s core U.S. Foodservice segment and the additive contribution from Restaurant Depot post-close. The margin driver is EBITDA expansion toward the 6.7% pro forma target, lifted by Restaurant Depot’s higher-margin business rather than cost cuts in the legacy Sysco operation.

The TIKR high case reaches $144.04 by 6/30/30, a 102.4% total return, if synergies accelerate and store openings outpace the current run rate. The low case is $102.78, a 44.4% total return, reflecting slower growth and margin pressure if integration headwinds or leverage prove sticky. The primary risk in every scenario is timing: the longer the regulatory review and deleveraging process extend, the longer the buyback remains suspended.

Conclusion: Watch local case volume growth at the Q3 fiscal 2026 earnings call on April 28, 2026. Management guided to at least 3%. A result at or above that level confirms the core business can support this acquisition. A miss at the moment of maximum balance sheet stress would validate the market’s harshest interpretation.

The thesis: Sysco’s $29.1 billion acquisition of Restaurant Depot is a long-term free cash flow and margin expansion story the market has priced as a near-term leverage problem. The TIKR mid-case model suggests patient investors are being paid 9.4% annually to wait for the evidence to catch up with the thesis.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Sysco?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Sysco, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Sysco alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!