Key Stats for Centene Stock

- 52-Week Range: $25.1 to $66

- Current Price: $35.1

- Street High Target: $70

What Happened?

Centene Corporation (CNC), the managed care giant serving more than 1 in 15 Americans through Medicaid, Medicare, and Marketplace plans, is executing a recovery from a 2025 adjusted EPS trough of $2.08 to a guided 2026 target exceeding $3.00, representing more than 40% earnings growth, even as shares trade near $35.

On February 6, CEO Sarah London reported Q4 2025 adjusted EPS of -$1.19, beating the -$1.22 consensus estimate, and issued 2026 adjusted EPS guidance above $3.00, topping the $2.94 analyst estimate compiled by LSEG, signaling stabilizing medical costs across Medicaid, Marketplace, and Medicare.

The Medicaid unit, Centene’s largest business line generating the bulk of its 27.6 million members, exited Q4 2025 with a health benefits ratio of 93.0%, improving 190 basis points from the Q2 2025 peak of 94.9%, while Molina Healthcare, its closest government-managed care peer, simultaneously guided 2026 adjusted EPS to just $5.00 against a $13.76 consensus estimate.

Sarah London, Chief Executive Officer, stated on the Q4 2025 earnings call that “while 2025 was undeniably challenging, disciplined execution enabled us to close the year slightly ahead of the expectations we outlined on our third quarter call,” anchoring confidence in the company’s mid-4s Medicaid net trend assumption and flat year-over-year HBR target for 2026.

A $1 billion partial redemption of its 4.25% notes, executed March 25, combined with a guided Marketplace pretax margin recovery from -1% to approximately 4%, and a Part D prescription drug plan business growing to 8.7 million members positions Centene to rebuild earnings toward the earnings power embedded across its three core businesses over the next three to five years.

Wall Street’s Take on CNC Stock

The Q4 2025 adjusted EPS beat of -$1.19 versus the -$1.22 consensus, combined with a 2026 adjusted EPS guide exceeding $3.00, marks the first credible earnings inflection point since Centene’s Medicaid health benefits ratio peaked at 94.9% in Q2 2025.

Medicaid stabilization, the recovery of Marketplace pretax margins from -1% to an estimated 4%, and Part D prescription drug plan membership growth to 8.7 million together support TIKR estimates of $2.99 normalized EPS in 2026 and $4.08 in 2027.

Wall Street remains cautious but is warming: 3 buys, 2 outperforms, and 13 holds among 17 analysts covering CNC put the mean price target at $43.18, implying roughly 23% upside from the current $35.11, as analysts track whether the guided Medicaid HBR stability at 93.7% holds through mid-year rate cycles.

The analyst price target spread of $32.00 to $70.00 reflects a binary read on Medicaid rate adequacy: bears anchor to the low end on further rate-trend mismatches, while bulls at $70.00 price in full Marketplace margin recovery and Medicare Advantage reaching breakeven in 2027.

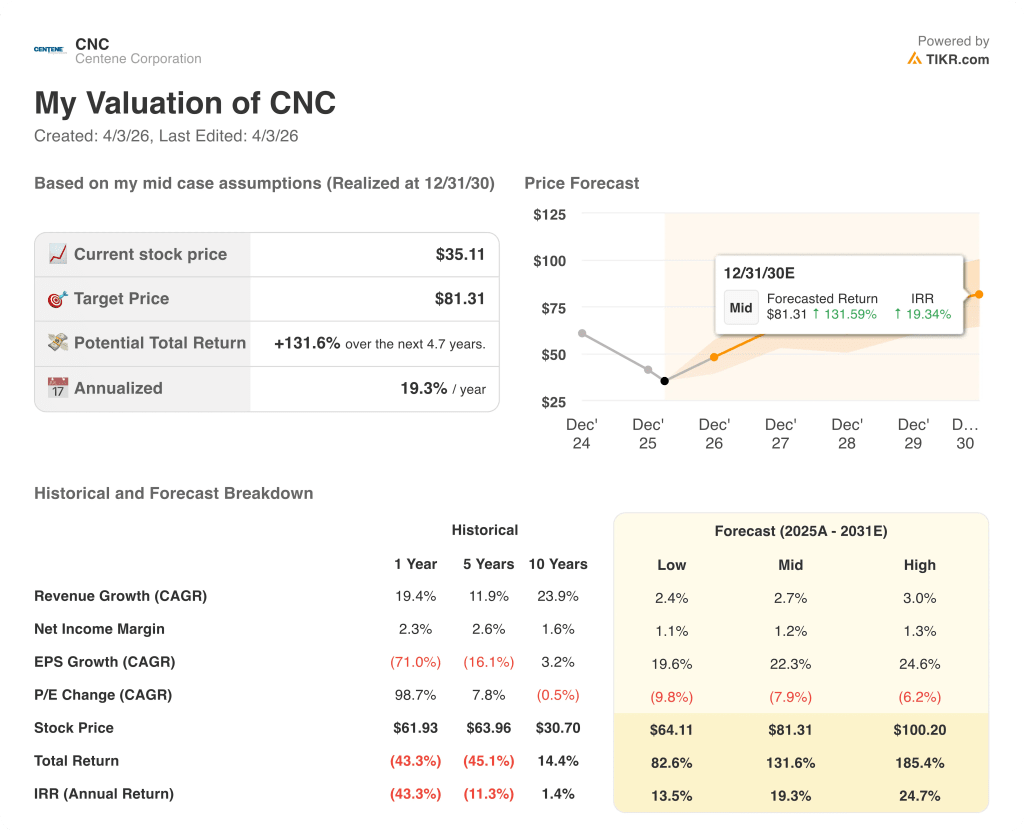

What Does the Valuation Model Say?

The TIKR mid-case model prices CNC at $81.31 by December 2030, embedding a 22.3% EPS CAGR assumption supported by the Medicaid HBR improvement trajectory and the Marketplace repricing of approximately mid-30% for 2026 that management executed in Q3 2025.

At approximately 11.7x 2026 normalized EPS of $2.99, CNC trades at a steep discount to its own pre-deterioration forward multiples and well below the managed care sector average, even as EBITDA is estimated to nearly double from $0.99 billion in 2025 to $1.87 billion in 2026, making CNC stock undervalued relative to the pace of its fundamental recovery.

The TIKR model’s core assumption, an EPS CAGR of 22.3% through 2030, is directly supported by the sequential Medicaid HBR improvement from 94.9% in Q2 2025 to 93.0% in Q4 2025 and the guided flat HBR in 2026, pointing to a TIKR mid-case price target of $81.31.

Management’s decision to monetize its PDP receivable to fund the $1 billion note redemption ahead of the December 2027 maturity signals active balance sheet management at a trough earnings level, not a company waiting to be rescued by macro tailwinds.

The one development that breaks the model is a Medicaid rate shortfall: if mid-year 4/1 and 7/1 state rate cycles come in below the mid-4s assumption, the flat HBR guide collapses and the EPS recovery trajectory shifts materially.

The final CMS Medicare Advantage rates expected in early April, alongside the end-of-Q1 Wakely Marketplace report, will confirm whether both the Medicare and Marketplace recovery assumptions embedded in the $3.00-plus 2026 EPS guide are tracking as planned.

Should You Invest in Centene Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CNC stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Centene Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CNC stock on TIKR for Free →