Key Takeaways:

- UPS is reshaping its network and customer mix, and management said 2026 should be an “inflection point” as the company completes its Amazon volume glide-down and focuses on higher-quality revenue.

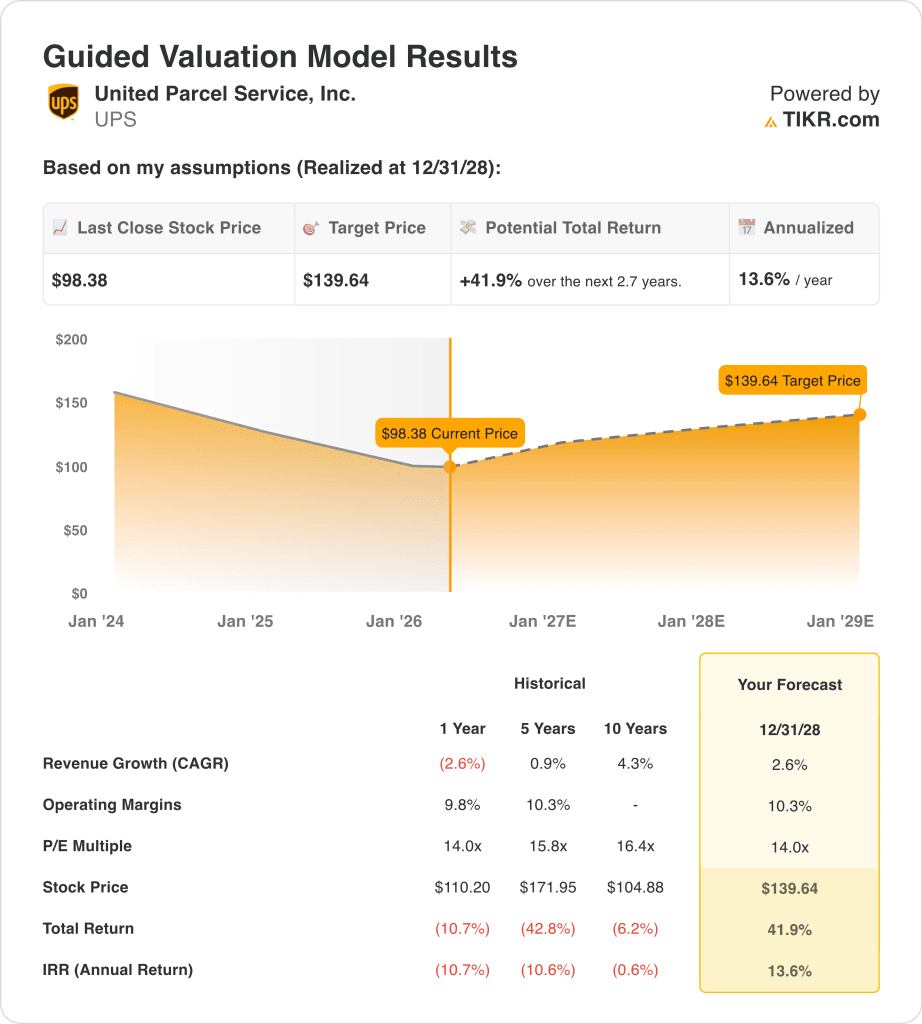

- UPS stock could reasonably reach $140 per share by December 2028, based on our valuation assumptions.

- This implies a total return of 41.9% from today’s price of $98, with an annualized return of 13.6% over the next 2.7 years.

What Happened?

United Parcel Service (UPS) is back in focus because investors are trying to decide whether the company is finally through the worst of its volume reset. In January, UPS reported fourth-quarter 2025 revenue of $24.5 billion, above analyst expectations, but also said it would cut up to 30,000 jobs and close 24 facilities in 2026 as it reduces lower-margin Amazon volume.

The latest operating data also looked mixed by segment. In the fourth quarter, U.S. Domestic revenue fell 3.2% because volume declined, but revenue per piece rose 8.3%, while International revenue increased 2.5% and revenue per piece rose 7.1%. Supply Chain Solutions revenue fell 12.7%, mainly because of lower Mail Innovations volume, which shows that UPS is still working through weaker, lower-value business.

March brought a few new signals for investors. UPS opened a $100 million logistics hub in Taiwan, its largest investment in Asia Pacific, to serve high-tech customers like semiconductor companies, but the company also withdrew its latest driver buyout program in the central U.S. after pressure from the Teamsters.

Those events matter because they show UPS is still investing in better long-term freight and healthcare-style logistics opportunities while labor and restructuring issues remain part of the near-term story. The broader backdrop is still complicated. FedEx said in March that global demand was holding up despite higher fuel costs, while the U.S. Postal Service sought a temporary 8% package price hike and noted that UPS and FedEx fuel surcharges were already much higher.

Here’s why UPS stock could keep recovering through 2028 if the company proves that lower-volume, higher-yield business can support steadier margins and cash flow.

What the Model Says for UPS Stock

We analyzed the upside potential for UPS stock using valuation assumptions based on its network reset, improving revenue quality, and ability to hold margins while growing slower than in prior cycles.

Based on estimates of 2.6% annual revenue growth, 10.3% operating margins, and a normalized P/E multiple of 14.0x, the model projects UPS stock could rise from $98 to $140 per share.

That would be a 41.9% total return, or a 13.6% annualized return over the next 2.7 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for UPS stock:

1. Revenue Growth: 2.6%

UPS is no longer in a high-volume expansion phase, and that is central to the valuation. Revenue fell 2.6% in 2025 to $88.7 billion, and the company’s 2026 guidance called for about $89.7 billion of revenue. That outlook points to only modest top-line growth, but it also reflects management’s strategy of reducing less profitable Amazon shipments rather than chasing volume at any cost.

The segment details support that view. Full-year 2025 U.S. Domestic adjusted revenue declined 1.7%, while International adjusted revenue rose 7.1%, and Supply Chain Solutions adjusted revenue fell 13.7%. In other words, UPS is leaning more on pricing, mix, and international strength while some legacy or lower-quality businesses shrink.

New investments still matter for the growth case. The Taiwan hub expansion shows UPS is targeting semiconductor and technology shipping flows, and management continues to emphasize healthcare, international, and premium logistics opportunities as better uses of the network.

Based on analysts’ consensus estimates, we use a 2.6% revenue growth forecast, which fits a mature logistics company that is prioritizing quality and yield over raw package counts.

2. Operating Margins: 10.3%

Margins are the heart of the current thesis. UPS reported a 10.5% consolidated operating margin in the fourth quarter of 2025 and guided to about 9.6% non-GAAP adjusted operating margin for full-year 2026, while management said 2026 should be an inflection point for growth and sustained margin expansion after the Amazon glide-down is complete.

The recent numbers show both pressure and stabilization. In 2025, operating income rose 6.4% to $8.5 billion, and full-year operating margin improved to 9.6% from 8.8% on an LTM basis in the terminal data, but domestic and international segment margins were still below the prior year in the fourth quarter. UPS is clearly improving efficiency, but it is not yet back to earlier cycle profitability levels.

Labor and restructuring will remain part of the equation. Reuters said UPS had planned up to 30,000 job cuts and 24 facility closures, while the driver buyout issue shows the labor side of the reset is still contested.

Based on analysts’ consensus estimates, we use a 10.3% operating margin assumption, which is slightly above the latest LTM margin and assumes steady execution rather than a sharp snapback.

3. Exit P/E Multiple: 14x

UPS no longer commands the richer multiple it had during the pandemic parcel boom. The stock trades at about 14.0x forward earnings in the terminal snapshot, which is below its own 5-year and 10-year historical P/E levels shown in the guided valuation model. That lower multiple reflects slower growth, restructuring risk, and the market’s preference for cleaner cyclical stories right now.

At the same time, UPS still has traits that support a respectable valuation. The company generated $8.5 billion of operating cash flow in 2025, paid a quarterly dividend of $1.64, and ended the year with a 6.7% indicated dividend yield in the terminal snapshot. That combination of cash flow, scale, and shareholder returns helps explain why the stock can still look attractive when sentiment improves.

Peers also matter for context. Reuters reported that FedEx surpassed UPS in market value in March as investors rewarded FedEx’s steadier demand commentary and cost progress, which shows how quickly the market can shift between logistics names.

Based on analysts’ consensus estimates, we maintain a 14.0x exit P/E multiple, which reflects UPS’s mature profile, income appeal, and the fact that investors still need proof that the margin-reset strategy is working.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

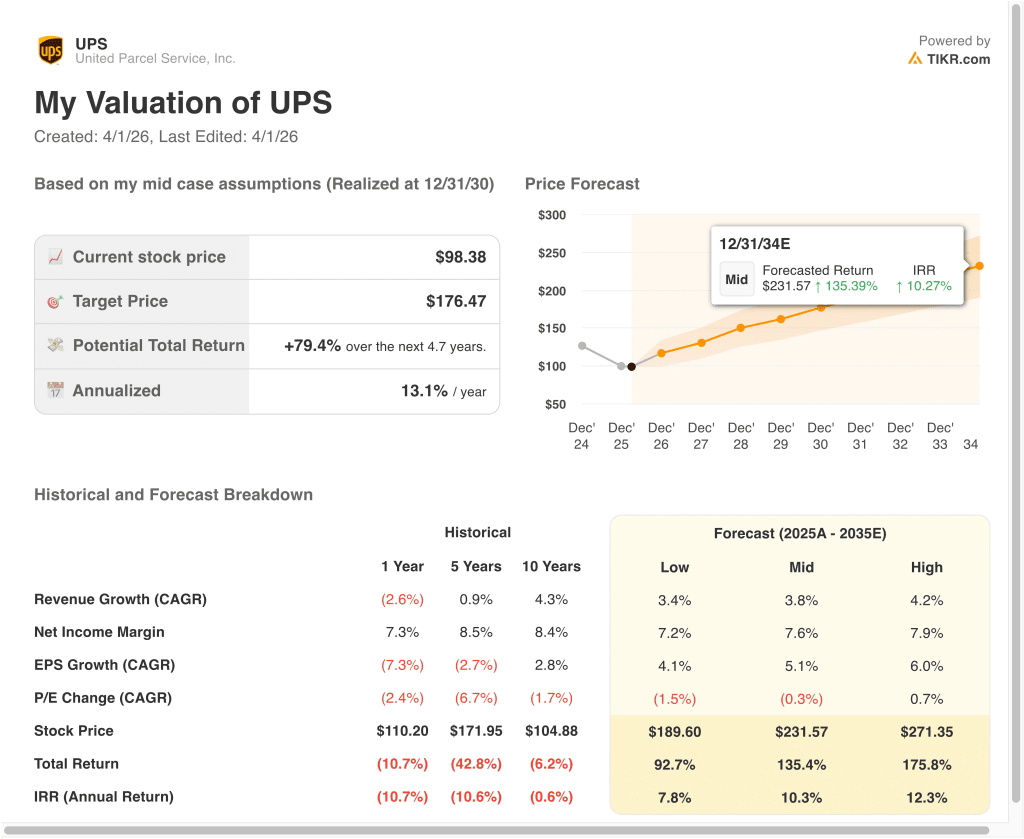

Different scenarios for UPS stock through 2035 show varied outcomes based on volume recovery, margin execution, and valuation discipline (these are estimates, not guaranteed returns):

- Low Case: Volume stays weak, and pricing cannot fully offset cost pressure → 7.8% annual returns

- Mid Case: UPS keeps improving revenue quality and executes its network reset well → 10.3% annual returns

- High Case: Margins recover faster, and international and healthcare logistics drive better mix → 12.3% annual returns

Even in the conservative case, UPS stock offers positive returns supported by its global network, sticky enterprise relationships, and dividend income. The key question is whether the company can prove that lower Amazon exposure and a leaner network will create better earnings quality over time. That is why the stock is trading more like a restructuring story than a simple macro shipping recovery.

Looking ahead, UPS stock will likely be focused on a few clear checkpoints. Investors will want to hear on the April 28 earnings call whether volume trends, pricing, and margin progression are tracking the 2026 guidance, and whether Taiwan and healthcare-style logistics investments are helping mix. If management can show that the revenue reset is mostly behind it, the stock could keep rerating from a lower base.

See what analysts think about UPS stock right now (Free with TIKR) >>>

Should You Invest in United Parcel Service, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up UPS, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track UPS alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze United Parcel Service stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!