Key Takeaways:

- Vertiv is benefiting from strong AI infrastructure demand, and its fourth-quarter orders rose 252% while backlog more than doubled to about $15.0 billion.

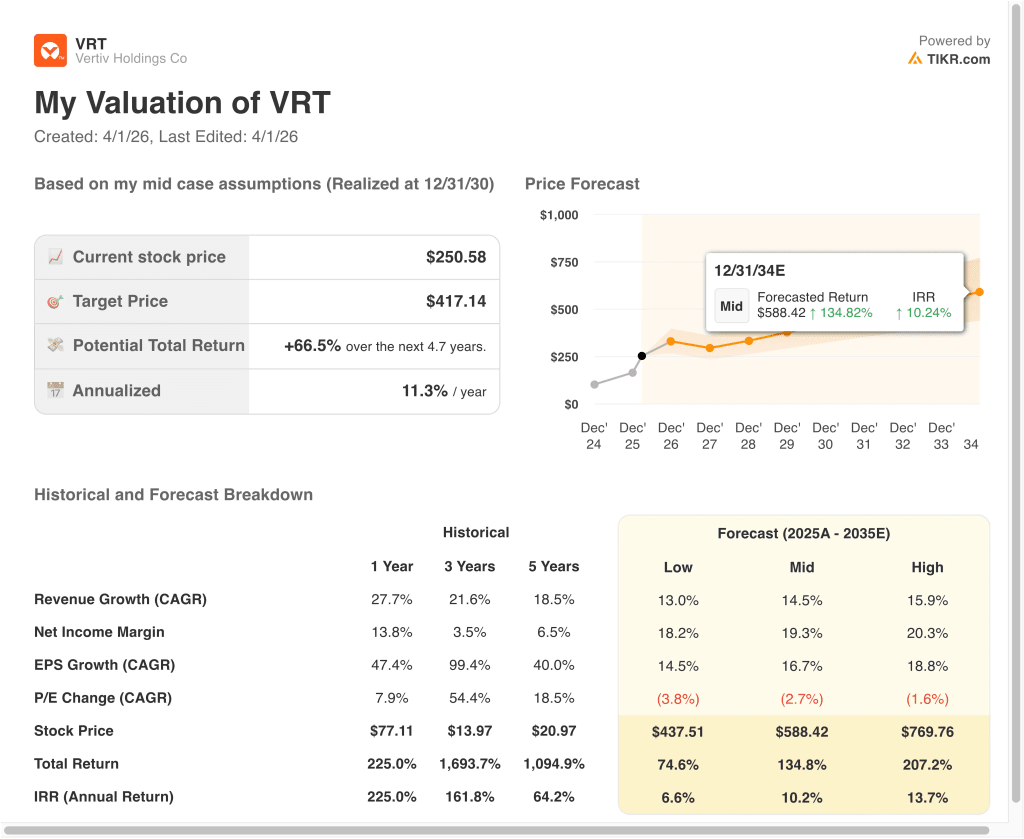

- VRT stock could reasonably reach $297 per share by December 2028, based on our valuation assumptions.

- This implies a total return of 18.5% from today’s price of $251, with an annualized return of 6.4% over the next 2.7 years.

What Happened?

Vertiv Holdings Co (VRT) stayed in focus through March because investors kept reassessing how much AI infrastructure demand is already priced into the stock. Early in the month, Vertiv joined the S&P 500, and shares rose as index funds prepared to buy the stock.

The bullish case also got fresh support from new product and capacity news. Vertiv said it is collaborating with NVIDIA on converged power and cooling designs for Vera Rubin DSX AI factories, and it also agreed to acquire ThermoKey to expand its heat-rejection and heat-exchange portfolio for high-density AI data centers.

At the same time, the stock faced a valuation check at the end of March. Reuters reported that Vertiv fell after Jefferies cut the stock to “hold,” even as the company announced about $50 million of investment to expand cooling systems manufacturing capacity in Ohio.

The latest quarterly results explain why enthusiasm has stayed elevated. Vertiv reported fourth-quarter 2025 net sales of $2.88 billion, up 23%, while adjusted operating margin improved to 23.2%, and management guided for 2026 organic sales growth of 27% to 29%.

CEO Giordano Albertazzi said, “Our fourth quarter performance demonstrates Vertiv’s leadership position in an increasingly complex and demanding data center market,” which helps explain why investors still see the company as a major AI infrastructure beneficiary.

Here’s why Vertiv stock could remain a closely watched AI infrastructure name through 2028 as investors weigh powerful order growth against a stock that already trades at a premium.

What the Model Says for VRT Stock

We analyzed the upside potential for Vertiv stock using valuation assumptions based on its strong position in AI data center power and cooling, accelerating order growth, and rising margin profile across critical digital infrastructure markets.

Based on estimates of 24.1% annual revenue growth, 20.4% operating margins, and a normalized P/E multiple of 29.6x, the model projects Vertiv stock could rise from $251 to $297 per share.

That would be a 18.5% total return, or a 6.4% annualized return over the next 2.7 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for VRT stock:

1. Revenue Growth: 24.1%

Vertiv ended 2025 with strong momentum. Fourth-quarter 2025 net sales rose 23% year over year to $2.88 billion, and full-year 2026 guidance called for organic sales growth of 27% to 29%. That growth is being driven by hyperscale and colocation customers that are building more AI-ready capacity.

Orders are an even more important signal for this business right now. Fourth-quarter organic orders rose about 252%, trailing twelve-month organic orders rose about 81%, and backlog reached about $15.0 billion, up 109% from a year earlier. Those numbers suggest that customer demand is not just healthy today, but also supports future revenue visibility.

Vertiv is also investing to support that demand. The company announced new manufacturing expansions across the Americas, including an Ohio investment tied to liquid cooling and chilled water systems, and it agreed to buy ThermoKey to deepen its cooling portfolio.

Based on analysts’ consensus estimates, we use a 24.1% revenue growth forecast, which reflects continued AI infrastructure demand while still assuming growth moderates from the most recent order surge.

2. Operating Margins: 20.4%

Vertiv’s margin story has improved materially, and that is a big reason the stock has rerated. In fourth-quarter 2025, adjusted operating margin reached 23.2%, up 170 basis points year over year, helped by higher volume, productivity, and favorable price-cost dynamics. Management also guided for a full-year 2026 adjusted operating margin of 22.0% to 23.0%.

The business mix helps here. Vertiv sells power systems, thermal systems, integrated modular solutions, racks, and lifecycle services, so it can capture value across multiple layers of a data center build. As AI clusters become denser, customers need more advanced cooling and power infrastructure, and that can support both pricing and mix.

Margin expansion still needs to be balanced against ongoing investment. Vertiv is increasing ER&D spending and expanding production capacity to capture more of the AI opportunity, so some costs will rise alongside growth.

Based on analysts’ consensus estimates, we use a 20.4% operating margin assumption, which fits the company’s recent execution while staying below management’s 2026 adjusted margin outlook.

3. Exit P/E Multiple: 29.6x

Vertiv trades at a premium because the market sees it as part of the AI infrastructure buildout rather than as a traditional electrical equipment company. That premium has been reinforced by the company’s S&P 500 inclusion, strong backlog growth, and repeated announcements tied to AI factory power and cooling systems. Still, premium multiples can compress quickly when expectations get too high.

That risk became visible at the end of March. Reuters reported that Vertiv shares fell after Jefferies downgraded the stock to “hold,” even though the company announced more manufacturing expansion in Ohio. In other words, investors still like the business, but some are questioning how much upside remains after the rally.

Vertiv does have financial flexibility to support its valuation. Management said net leverage was about 0.5x at the end of the fourth quarter, and the company completed a $2.1 billion senior unsecured bond offering plus a $2.5 billion revolving credit facility in March.

Based on analysts’ consensus estimates, we maintain a 29.6x exit P/E multiple, which reflects Vertiv’s AI exposure but also assumes some moderation from today’s elevated enthusiasm.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for VRT stock through 2030 show varied outcomes based on AI infrastructure demand, margin execution, and valuation discipline (these are estimates, not guaranteed returns):

- Low Case: AI data center spending cools, and valuation compresses faster → 6.6% annual returns

- Mid Case: Vertiv keeps scaling power and cooling solutions across AI deployments → 10.2% annual returns

- High Case: Orders, margins, and AI factory adoption remain exceptionally strong → 13.7% annual returns

Even in the conservative case, Vertiv stock offers positive returns supported by its strong position in power and cooling infrastructure, rising free cash flow, and deep exposure to AI data center spending.

Vertiv’s next move will likely depend on whether first-quarter results confirm that demand is still converting into revenue and margins. The next key checkpoint is its expected Q1 2026 report on April 22, followed by its May investor conference, where management is set to discuss strategy and technology updates.

If order growth stays strong but the valuation multiple cools, the stock could still work higher, but likely with more volatility than investors saw earlier in the rally.

See what analysts think about VRT stock right now (Free with TIKR) >>>

Should You Invest in Vertiv Holdings Co?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up VRT, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track VRT alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Vertiv stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!