Key Takeaways:

- Strategic Transformation: PepsiCo is executing surgical pricing investments and major brand restages across Lay’s, Gatorade, and Quaker.

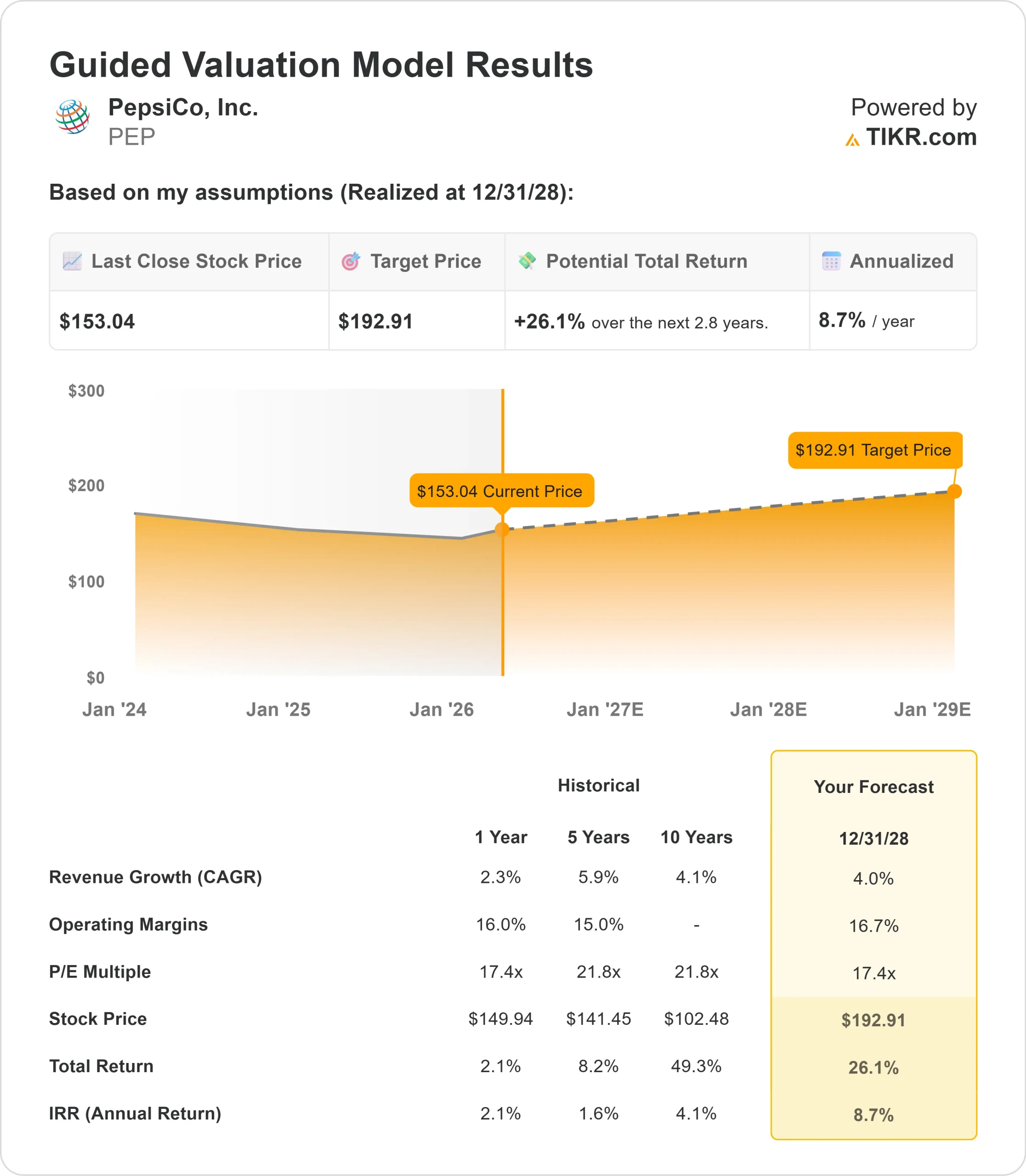

- Price Projection: Based on current assumptions, PEP stock could reach $193 by December 2028.

- Potential Gains: This target implies a total return of 26% from the current price of $153.

- Annual Return: Investors could see roughly 9% growth over the next 2.8 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

PepsiCo (PEP) delivered a mixed Q4 in 2025, navigating persistent consumer headwinds while laying the groundwork for a volume-driven recovery.

The company is now shifting from a price-led strategy to one focused on affordability and innovation, targeting increased household penetration and category growth.

CEO Ramon Laguarta emphasized a comprehensive transformation across the portfolio.

- Frito-Lay North America is launching surgical pricing investments aimed at low- and middle-income consumers facing affordability friction.

- These initiatives, tested extensively across multiple markets, have delivered strong ROI and will be complemented by double-digit gains in shelf space at major retailers starting in March and April.

- The beverage business showed momentum in 2025, with trademark Pepsi growing both volume and dollars.

- Energy continues to be a bright spot, with the company holding close to 20% share through its Celsius distribution partnership and the integration of Alani Nu.

- Management expects both PFNA and PBNA to return to volume growth early in 2026, with net revenue acceleration building throughout the year.

- PepsiCo is also addressing the GLP-1 opportunity head-on.

- Rather than viewing weight-loss medications as a threat, the company sees multiple growth vectors: portion control (already 70%+ of the food business), hydration (Propel growing by 20%+), fiber innovation through Quaker and SunChips, and protein-enriched offerings.

- These initiatives position PepsiCo to capture consumption from GLP-1 users rather than lose it.

For 2026, management guided to low-single-digit organic sales growth with acceleration in the second half.

The company expects operating margin expansion despite significant commercial investments, funded by productivity savings and operational efficiency gains.

See analysts’ full growth forecasts and estimates for PEP stock (It’s free) >>>

What the Model Says for PepsiCo Stock

We analyzed PepsiCo in light of its strategic pivot toward volume growth and category leadership. The company benefits from multiple catalysts that should drive sustainable performance.

- In North America, PepsiCo is resetting its value proposition.

- The Frito-Lay business will gain substantial shelf space while investing in targeted affordability.

- Major brand relaunches include Lay’s (emphasizing freshness, simple ingredients, and premium oils such as avocado and olive), Tostitos, Gatorade (low-sugar, no artificials), and Quaker (whole grains and fiber).

- These aren’t minor tweaks—they’re holistic transformations addressing consumer demands for simpler, more functional products.

- Internationally, momentum is building. Mexico is improving, China shows positive trends, and the Middle East remains strong. These markets should deliver consistent mid-single-digit growth.

Using a forecast of 4.0% annual revenue growth and 16.7% operating margins, our model projects the stock will rise to $193 within 2.8 years. This assumes a 17.4x price-to-earnings multiple.

That represents compression from PepsiCo’s historical P/E averages of 21.8x (five years) and 21.8x (ten years).

The lower multiple acknowledges near-term uncertainty as the company transitions from a pricing-driven model to volume-led growth, with execution risks around the affordability investments and innovation pipeline.

The real value lies in capturing long-term category growth through innovation while expanding margins through productivity and operational integration, including the ongoing tests of combined food and beverage distribution in Texas and Florida.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for PEP stock:

1. Revenue Growth: 4.0%

PepsiCo’s growth centers on structural improvements in North America while maintaining international momentum.

Management expects organic sales growth to strengthen in the second half of 2026 as pricing investments gain traction, innovation launches take hold, and recent acquisitions such as Poppi and Siete contribute to organic growth.

The company delivered 2.3% revenue growth in 2025 despite challenging conditions. With affordability initiatives, double-digit shelf gains, major brand relaunches, and improving international trends, 4% growth appears achievable as the volume trajectory inflects positively.

2. Operating margins: 16.7%

PepsiCo has maintained operating margins near 16% despite inflationary pressures.

The company demonstrated strong productivity in Q4 2025, which management expects to carry into Q1 2026.

These savings will fund commercial investments while still allowing for margin expansion.

The integration of food and beverage distribution systems, supply chain optimization, and right-sizing Frito-Lay operations provides additional opportunities for efficiency.

Combined with operating leverage from volume growth, 16.7% margins are realistic.

3. Exit P/E Multiple: 17.4x

The market currently values PepsiCo at 17.7x earnings. We assume the P/E remains near 17.4x through our forecast period. This reflects balanced risk-reward as the company executes its strategic transformation.

Near-term uncertainty around consumer spending, GLP-1 adoption rates, and execution on affordability investments creates some multiple pressure.

However, as PepsiCo demonstrates volume recovery and successful innovation launches, the company should command a stable premium multiple given its market leadership and strong cash generation.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

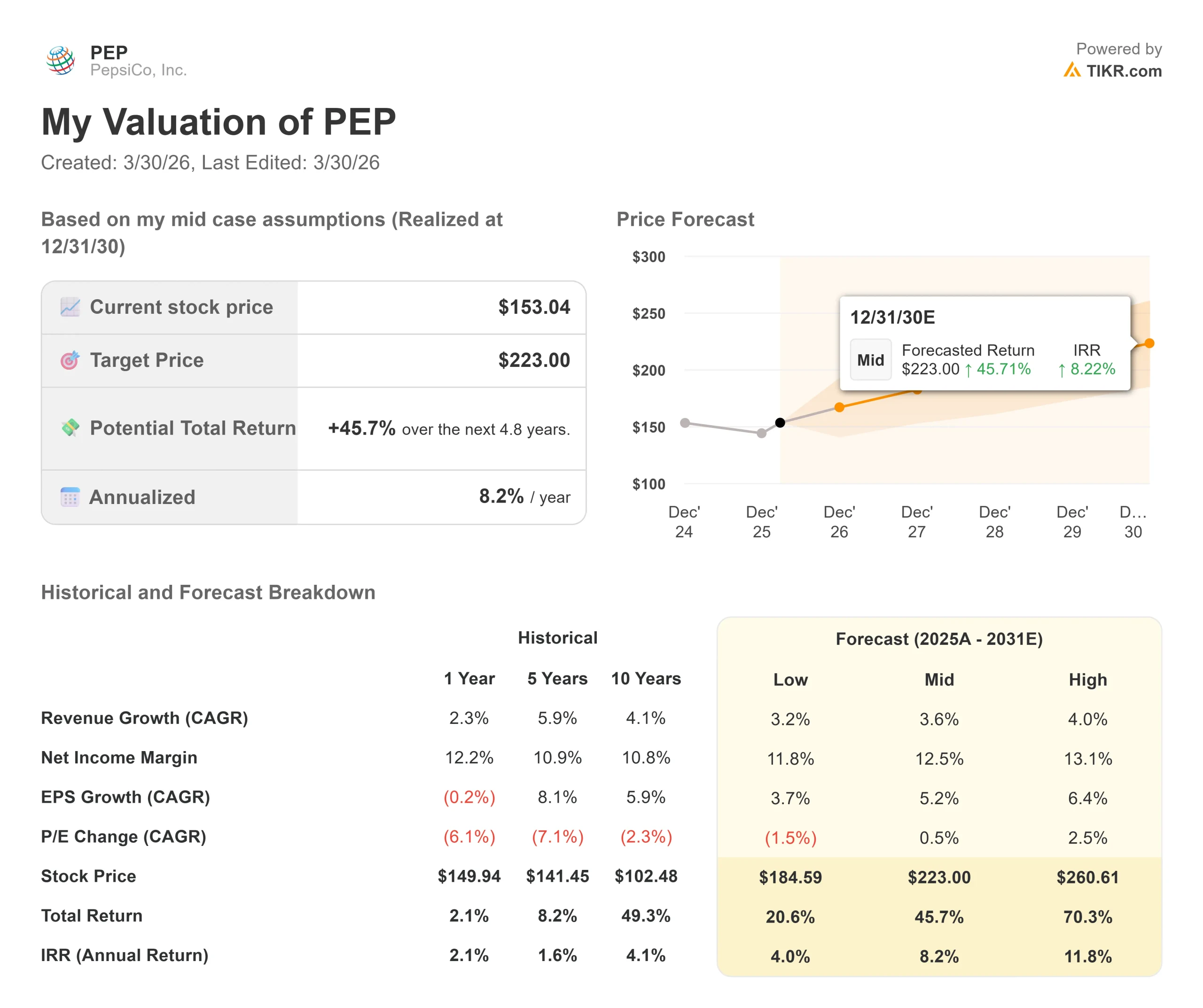

Consumer staples face evolving consumption patterns and competitive intensity. Here’s how PepsiCo stock might perform under different scenarios through December 2030:

- Low Case: If revenue growth slows to 3.2% and net income margins compress to 11.8%, investors still see a 21% total return (4.0% annually).

- Mid Case: With 3.6% growth and 12.5% margins, we expect a total return of 46% (8.2% annually).

- High Case: If innovation and affordability initiatives drive 4.0% revenue growth while PepsiCo maintains 13.1% margins, returns could hit 70% total (11.8% annually).

See what analysts think about PEP stock right now (Free with TIKR) >>>

The range reflects execution on brand relaunches, successful navigation of the GLP-1 opportunity, and the company’s ability to convert shelf space gains and affordability investments into sustained volume growth.

In the low case, consumer pressures intensify or innovation fails to resonate.

In the high case, the strategic pivot accelerates category growth beyond expectations while productivity initiatives deliver better-than-planned margin expansion.

How Much Upside Does PepsiCo Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!