Key Takeaways:

- Adobe is under pressure because investors want stronger proof that AI products can support growth while leadership and regulatory issues stay in focus.

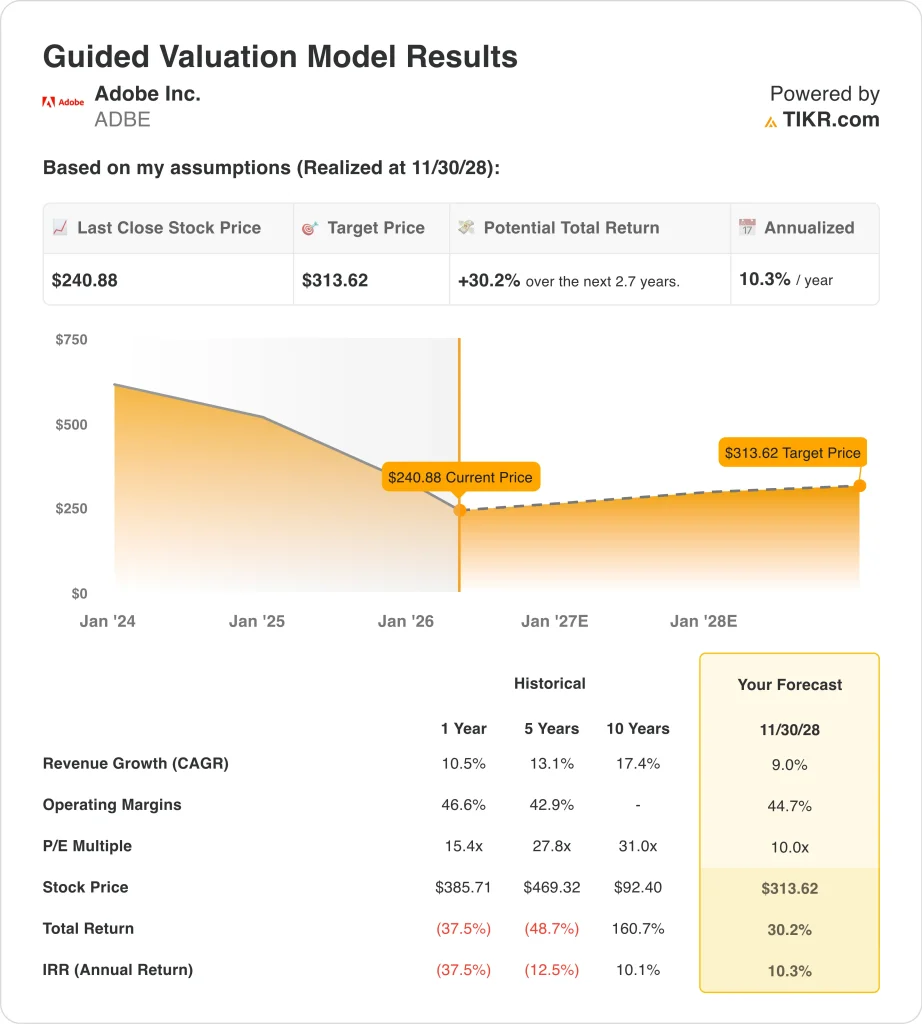

- Adobe stock could reasonably reach $314 per share by November 2028, based on our valuation assumptions.

- This implies a total return of 30.2% from today’s price of $241, with an annualized return of 10.3% over the next 2.7 years.

What Happened?

Adobe Inc. (ADBE) became a bigger market story after its March quarter report and the events that followed. Adobe reported record Q1 FY2026 revenue of $6.4 billion, up 12% year over year, and it also said total ARR exited the quarter at $26.1 billion.

Yet Reuters reported the stock fell after the print because investors were already focused on AI competition and then had to process the added uncertainty of CEO Shantanu Narayen’s planned transition.

The company’s recent news flow added both positives and negatives. Adobe announced a deeper partnership with NVIDIA to build the next generation of Firefly models and agentic workflows, and Germany’s cartel office cleared Adobe’s planned acquisition of Semrush in the first phase of review.

But the U.K. regulator also opened a probe over cancellation fee concerns, and Adobe agreed to a $150 million settlement with U.S. authorities over subscription disclosures and cancellations.

Adobe’s own management tried to keep the focus on execution. In the Q1 release, CFO Dan Durn said, “Adobe delivered 13 percent subscription revenue growth and record Q1 cash flow of $2.96 billion,” while management also said AI-first offerings ended ARR more than tripled year over year.

Even so, the market still seems more interested in the pace of AI monetization, leadership continuity, and subscription policy scrutiny than in the headline beat alone.

Here’s why Adobe stock could deliver moderate returns through 2028 if AI products deepen monetization and margins stay strong, but the stock likely needs cleaner execution and better sentiment first.

What the Model Says for ADBE Stock

We analyzed the upside potential for Adobe stock using valuation assumptions based on recurring subscription revenue, very high margins, and a lower earnings multiple than Adobe carried in prior years.

Based on estimates of 9.0% annual revenue growth, 44.7% operating margins, and a normalized P/E multiple of 10.0x, the model projects Adobe stock could rise from $241 to $314 per share.

That would be a 30.2% total return, or a 10.3% annualized return over the next 2.7 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for ADBE stock:

1. Revenue Growth: 9%

Adobe has remained a steady grower even as the stock fell sharply. Revenue rose from $21.5 billion in FY2024 to $23.8 billion in FY2025, and LTM revenue reached about $24.5 billion in the figures you provided. That matters because investors are not dealing with a broken top line, but with a debate over how much AI can sustain or accelerate that growth.

The revenue engine is still mostly subscriptions. Adobe said Q1 FY2026 subscription revenue rose 13%, and management said total ARR reached $26.06 billion exiting the quarter. Those numbers show why the market still gives Adobe credit for a durable business model, even while it questions future growth quality.

Based on analysts’ consensus estimates, we use a 9.0% revenue growth assumption. That is below Adobe’s 10.5% one-year historical revenue CAGR shown in the valuation model, so it is not asking for a major acceleration. It assumes Adobe keeps growing through Creative Cloud, Document Cloud, and AI-first offerings, but at a slower pace than its older high-growth years.

2. Operating Margins: 44.7%

Adobe’s margins remain one of its biggest strengths. LTM gross margin was 89.4%, and LTM EBIT margin was 36.6% in the figures you provided, while the income statement shows Adobe has kept operating income growing alongside revenue. That gives Adobe room to invest in AI and still produce strong earnings and cash flow.

Cash flow helps explain why margin quality matters so much here. Adobe reported record Q1 operating cash flow of $2.96 billion, and the cash flow figures you shared show LTM free cash flow above $10 billion. A business that throws off that much cash can absorb product investment, support buybacks, and still defend profitability better than most software peers.

Based on analysts’ consensus estimates, we use a 44.7% operating margin assumption. That is slightly below the 46.6% one-year historical margin shown in the valuation model, so it looks measured rather than aggressive. It assumes Adobe stays highly profitable, but it also leaves room for AI investment and go-to-market costs as the company pushes new offerings.

3. Exit P/E Multiple: 10x

Adobe’s multiple has compressed sharply, and that is a big part of the story. The figures you provided show LTM P/E near 14.0x, while the guided model uses a 10.0x exit multiple. That means the valuation case already assumes further compression, not a big rebound in sentiment.

That lower multiple reflects real uncertainty. Investors are balancing strong fundamentals against AI competition, leadership transition risk, and regulatory pressure around subscription practices. Those concerns explain why Adobe could beat revenue expectations and remain under pressure in the market.

Based on analysts’ consensus estimates, we maintain a 10.0x exit multiple. That looks conservative for a software company with Adobe’s margins and cash generation, but it matches the model and today’s sentiment. If Adobe outperforms this setup, it will likely come from stronger earnings and AI monetization, not from investors suddenly paying a premium multiple again.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

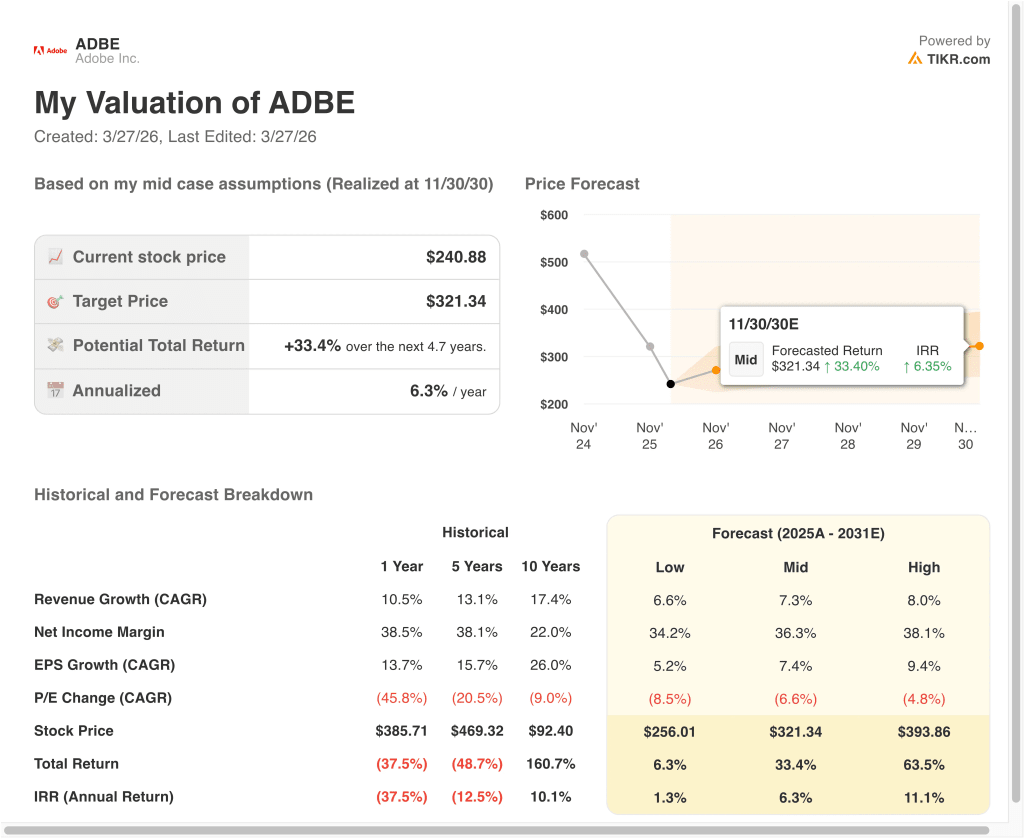

Different scenarios for ADBE stock through 2030 show varied outcomes based on AI monetization, margin durability, and valuation discipline (these are estimates, not guaranteed returns):

- Low Case: AI monetization ramps slowly, and valuation compresses faster → 1.3% annual returns

- Mid Case: Adobe keeps scaling AI across Creative Cloud, Document Cloud, and enterprise workflows → 6.3% annual returns

- High Case: Firefly adoption, enterprise AI workflows, and cross-cloud monetization stay exceptionally strong → 11.1% annual returns

Going forward, Adobe stock will likely trade on AI revenue signals, subscription durability, and management clarity. The next key checkpoints are the April 15 annual meeting, Adobe Summit in late April, and fiscal Q2 results expected in June.

If Adobe can show that Firefly and other AI products are adding meaningful growth without hurting margins, the stock may start to look less like a disrupted incumbent and more like a profitable platform in transition.

See what analysts think about ADBE stock right now (Free with TIKR) >>>

Should You Invest in Adobe Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ADBE, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track ADBE alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Adobe stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!