Key Takeaways:

- Upstart is being pulled between two forces right now: a much better funding and revenue story, and investor concern about margins, dilution, and leverage after a sharp 2026 selloff.

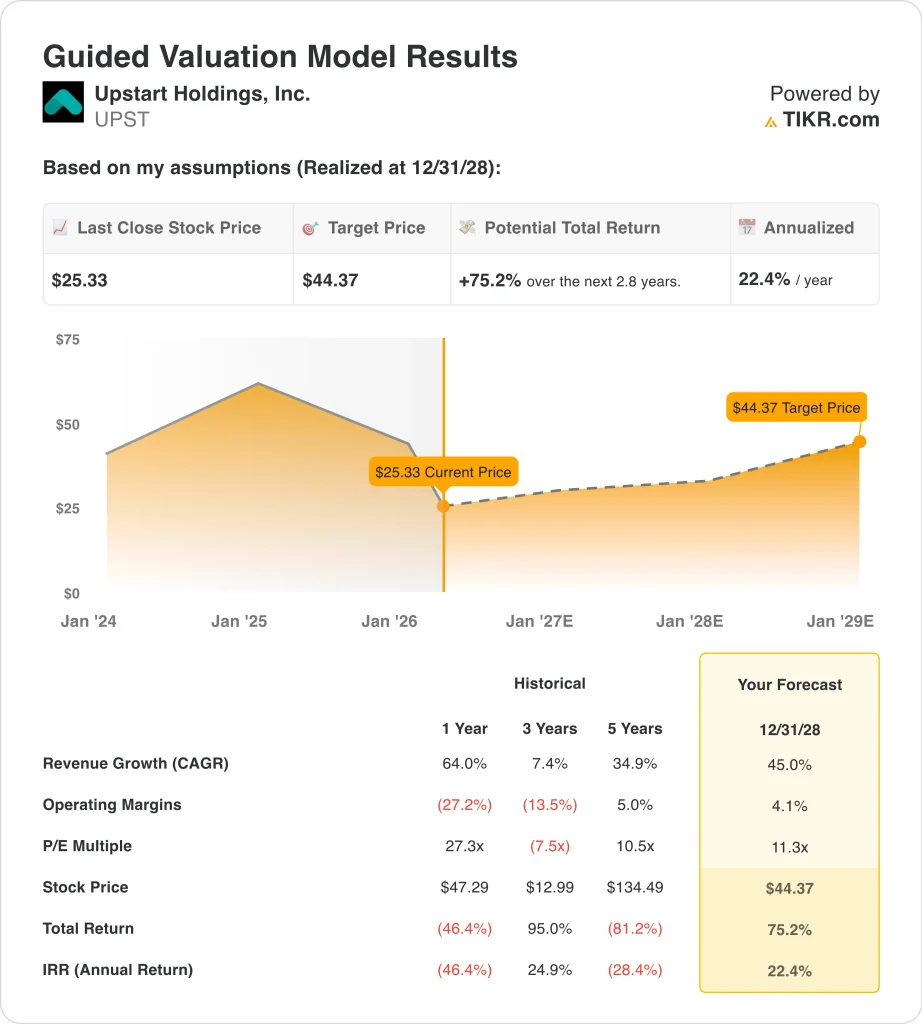

- Upstart stock could reasonably reach $44 per share by December 2028, based on our valuation assumptions.

- This implies a total return of 75.2% from today’s price of $25, with an annualized return of 22.4% over the next 2.8 years.

What Happened?

Upstart Holdings, Inc. (UPST) is relevant right now because the stock has been hit hard even as the business has started growing again. Shares closed at $25 on March 26, 2026, and the terminal overview shows the stock down 44.7% year to date and sitting just above its 52-week low of $25. That tells you investors are not questioning whether revenue recovered in 2025, but whether that recovery is strong enough to support the company’s balance sheet and long-term margins.

The biggest event was the February earnings report, which looked strong on the surface but was more mixed underneath. Upstart reported Q4 2025 revenue of $296 million, up 35% year over year, and diluted EPS of $0.17, while full-year 2025 revenue rose 64% to about $1.0 billion and net income improved to $53.6 million from a loss in 2024.

Management still sounded optimistic about the operating setup. CEO Dave Girouard said Upstart had “re-established Upstart as a strongly profitable business,” and added that the company was “set up for a breakout in 2026.” That tone was backed by 2026 guidance for about $1.4 billion in revenue and a 21% adjusted EBITDA margin, plus a longer-term target of roughly 35% revenue CAGR from 2025 to 2028.

The story shifted back toward funding access and platform scale. Upstart said it plans to apply for a national bank charter, which it says could reduce operational, regulatory, and financial complexity, and it also announced a $1 billion forward-flow agreement with Eltura Ventures, Aperture Investors, and co-investors. On top of that, Harborstone Credit Union joined the platform for personal lending.

Here’s why Upstart stock could remain volatile in the near term as investors weigh faster revenue growth and new funding agreements.

What the Model Says for UPST Stock

We analyzed the upside potential for Upstart stock using valuation assumptions based on faster revenue growth, a return to positive profitability, and a much lower earnings multiple than the company traded at during its earlier cycle.

Based on estimates of 45% annual revenue growth, 4.1% operating margins, and a normalized P/E multiple of 11.3x, the model projects UPST stock could rise from $25 to $44 per share.

That would be a 75.2% total return, or a 22.4% annualized return over the next 2.8 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for UPST stock:

1. Revenue Growth: 45%

Upstart’s revenue has been volatile, so this assumption needs context. Total revenue fell from $853.3 million in 2022 to $548.5 million in 2023, then recovered to $677.0 million in 2024 and $1.08 billion in 2025. That rebound matters because it shows the platform is again originating and distributing more loans after the funding shock that hurt the business in 2022 and 2023.

The business drivers are loan volume, conversion, and funding partner demand. In 2025, Upstart originated about $11.0 billion of loans, up 86% year over year, and Q4 transaction volume rose 86% with a 19.4% conversion rate. The company also said more than 90% of loans are fully automated, which helps explain why scale can matter so much when volume returns.

Based on analysts’ consensus estimates, we used a 45.0% forecast. That is aggressive, but it lines up with management’s 2026 revenue target of about $1.4 billion and its 2025-2028 target of roughly 35% revenue CAGR, while also reflecting new funding agreements and partner additions announced in March. For Upstart, revenue growth is the clearest sign that its AI lending marketplace is attracting both borrowers and capital again.

2. Operating Margins: 4.1%

Upstart is no longer in the deep loss position it faced in 2023 and 2024, but margins are still fragile. Operating margin was negative 40.4% in 2023, negative 19.6% in 2024, and positive 6.9% in 2025. That swing back into positive territory is important because it shows the company can become profitable again once revenue scales faster than operating costs.

At the same time, investors have not fully bought into the margin story. Q4 contribution margin fell to 53% from 61% a year earlier, and the stock sold off after earnings, even though EPS came in positive. That reaction makes sense because Upstart’s business depends not just on revenue growth, but on how much of each dollar it keeps after funding, model, and platform costs.

Based on analysts’ consensus estimates, we use 4.1% operating margins. That is actually below the 6.9% operating margin the company posted in 2025, which makes the model look conservative on this line. In other words, the valuation is not assuming a major margin miracle, and is instead giving more weight to revenue growth and normalization in the funding environment.

3. Exit P/E Multiple: 11.3x

The multiple assumption is one of the most important parts of this model. Upstart’s historical P/E has been all over the place because earnings have swung from strong profits to steep losses and back again, and the guided model uses just 11.3x by 2028. That is modest for a company still targeting rapid growth, and it reflects how skeptical the market remains after the stock’s boom-and-bust cycle.

There are real reasons for that caution. The terminal overview shows LTM net debt of $1.24 billion and LTM net debt to EBITDA of 10.57x, while the balance sheet shows total debt rose to $1.90 billion at year-end 2025. Upstart also had a negative free cash flow of $148.1 million in 2025, so investors are still watching liquidity, warehouse funding, and dilution risk very closely.

Based on analysts’ consensus estimates, we maintain an 11.3x exit multiple. That looks reasonable because it leaves room for growth without assuming investors will value Upstart like a premium software company again. If the stock works from here, it will probably be because the company keeps expanding originations and funding relationships while proving that profits can stay positive through the cycle.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

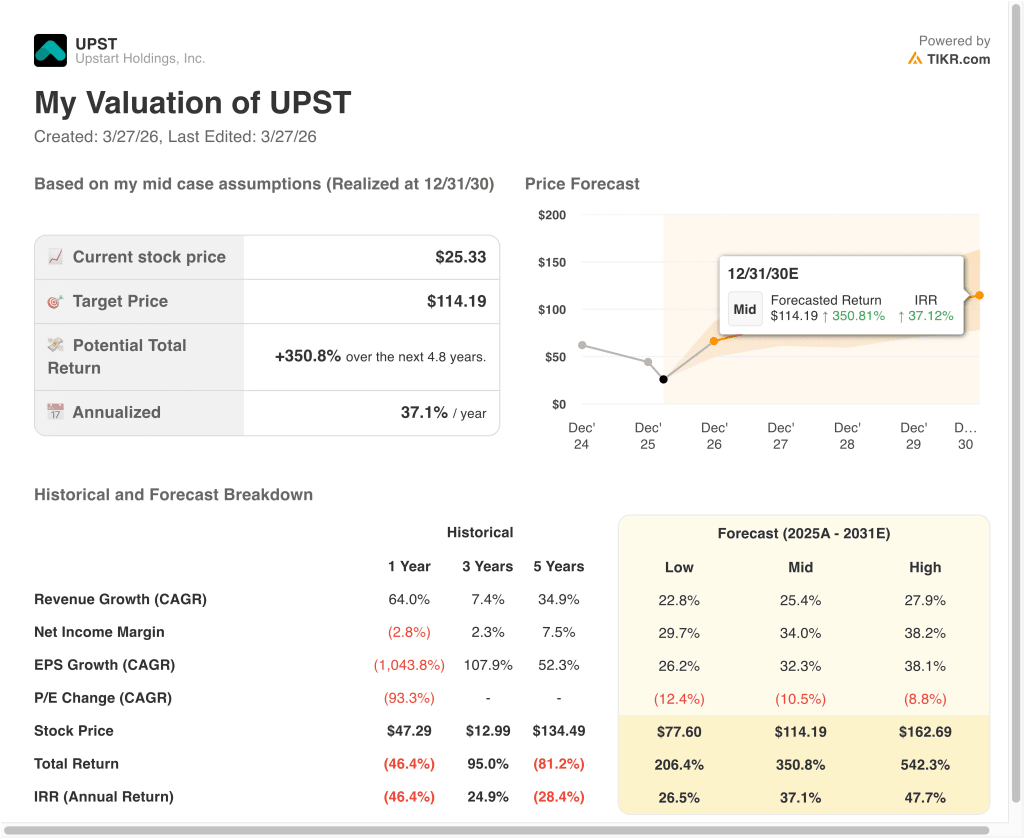

Different scenarios for Upstart stock through 2030 show varied outcomes based on loan funding, revenue growth, and profitability (these are estimates, not guaranteed returns):

- Low Case: Funding markets stay uneven, loan buyers remain cautious, and earnings growth comes in below expectations → 26.5% annual returns

- Mid Case: Upstart keeps rebuilding loan demand, bank and credit union partnerships expand, and profitability improves at a healthy pace → 37.1% annual returns

- High Case: The funding ecosystem deepens quickly, conversion stays strong, and Upstart proves its AI underwriting can scale across more lending products → 47.7% annual returns

Even in the conservative case, the model still shows large upside because Upstart’s starting valuation is low relative to its prior revenue base and long-term growth targets.

But that does not mean the path will be smooth, because this stock still trades on funding conditions, credit sentiment, and confidence in management’s ability to keep the marketplace liquid. That is why UPST can move sharply on product updates, partner announcements, and any signal that loan buyers are either returning or pulling back.

Going forward, the next key checkpoints are funding progress and Q1 results expected on May 5. Investors will likely watch whether the bank charter effort advances, whether new forward-flow and partner deals keep coming, and whether revenue growth is translating into steadier free cash flow. If those pieces keep improving together, the stock’s valuation could look very different by the end of 2026 than it does today.

See what analysts think about UPST stock right now (Free with TIKR) >>>

Should You Invest in Upstart Holdings, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up UPST, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track UPST alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Upstart stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!