Key Stats for Analog Devices Stock

- Past-Week Performance: +1.1%

- 52-Week Range: $158.7 to $363.2

- Current Price: $313.4

What Happened?

Analog Devices (ADI), a chipmaker whose semiconductors power industrial machines, data centers, and vehicles, posted fiscal Q1 revenue of $3.16 billion, up 30% year-over-year, marking its strongest cyclical recovery in years while the stock trades at $313.42 after hitting a 52-week high of $363.20.

On February 18, ADI reported adjusted EPS of $2.46, beating the IBES estimate of $2.31 by 6.5%, and guided Q2 revenue to $3.50 billion, roughly 8.4% above the $3.23 billion Wall Street consensus, driven by record orders in its Data Center segment and broad Industrial recovery.

ADI’s Communications segment, which houses its optical and power products for AI data centers, surged 63% year-over-year in Q1, while Industrial, its most profitable end market at 47% of revenue, grew 38% year-over-year, with ATE, the automated test equipment business that validates advanced semiconductors, hitting a record quarter.

CFO Richard Puccio stated on the Q1 2026 earnings call that “our revenue outlook for the second quarter reflects a new high-watermark for ADI, underscoring our strong execution against cyclical and secular growth tailwinds,” reinforcing the Q2 guidance of $2.88 adjusted EPS against a prior consensus of $2.46.

On February 17, ADI raised its quarterly dividend 11% to $1.10 per share, its 22nd consecutive annual increase, while targeting $1 billion in Maxim acquisition synergies by 2027 and guiding operating margins to 47.5% in Q2, building a compounding case for durable, above-market free cash flow generation.

Wall Street’s Take on ADI Stock

ADI’s Q2 guidance of $3.50 billion, 8.4% above the prior Wall Street consensus, confirms the cyclical recovery in Industrial has momentum, meaning the volume-driven operating leverage already visible in Q1’s 45.5% non-GAAP operating margin is only beginning to compound.

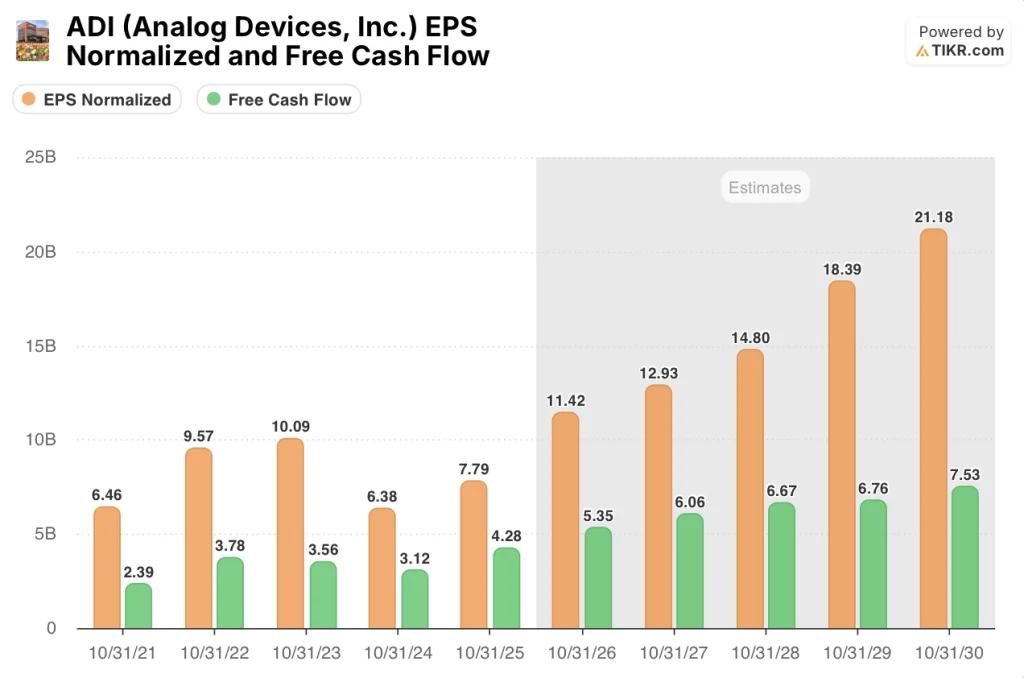

Normalized EPS is estimated to surge 46.7% from $7.79 in fiscal 2025 to $11.42 in fiscal 2026, supported by 26.8% revenue growth to $13.98 billion, as AI data center demand and Industrial’s broad-based recovery drive utilization and mix simultaneously higher.

Additionally, ADI’s FCF is estimated to grow 25.1% from $4.28 billion in fiscal 2025 to $5.35 billion in fiscal 2026, reaching a 38.3% FCF margin, which funds both the 22nd consecutive dividend increase and ongoing share count reduction without balance sheet strain.

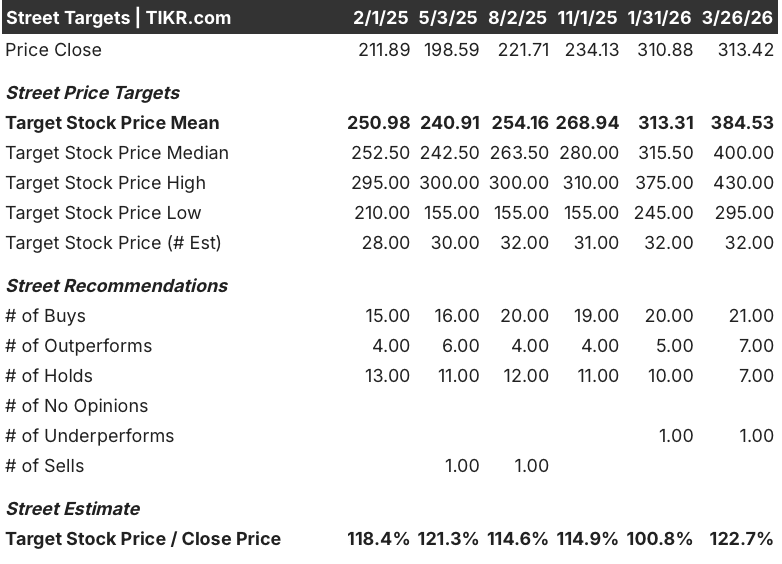

Twenty-one buys, 7 outperforms, and 7 holds among 32 analysts price ADI at a mean target of $384.53, implying 22.7% upside from $313.42, with bulls anchoring their conviction to AI infrastructure CapEx momentum and the Industrial cyclical recovery that drove Q1 revenues 30% above year-ago levels.

The analyst target range of $295.00 on the low end to $430.00 on the high end separates on one hinge: whether Automotive, which ended Q1 with a book-to-bill below 1, stabilizes in the second half of fiscal 2026 as management expects, or drags on Industrial’s recovery momentum.

What Does the Valuation Model Say?

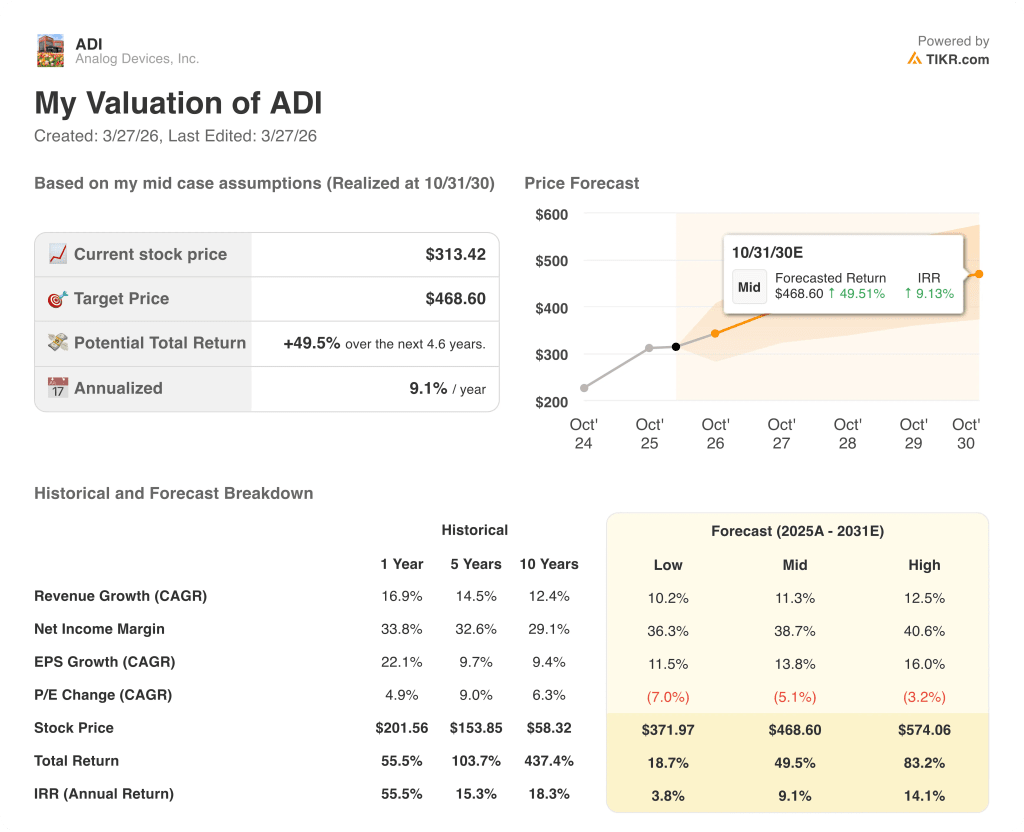

The TIKR mid-case target of $468.60 implies 49.5% total return over 4.6 years at a 9.1% IRR, assuming an 11.3% revenue CAGR and net income margins expanding to 38.7%, driven by the Industrial recovery, AI data center optical and power portfolio growth, and the $1 billion Maxim synergy target expected by 2027.

The market prices ADI at roughly 27x forward normalized EPS of $11.42, a discount to its own recent 32x NTM multiple, despite Industrial volumes still sitting 20% below prior peaks and the AI data center business growing above 50% annually.

ADI’s Q1 book-to-bill above 1 across all Industrial submarkets and geographies, before any pricing adjustment, signals genuine demand rather than channel refill, grounding the estimated 11.3% revenue CAGR in real order activity.

Automotive remains the one variable that breaks the model: if China auto demand, now 1/3 of ADI’s global auto revenue, weakens further beyond the tariff-related pull-in already absorbed in Q1, the fiscal 2026 EPS path to $11.42 faces compression at the segment level.

Q2 fiscal 2026 results, expected in May, will either validate or challenge the core assumption: watch whether non-GAAP operating margin hits the guided 47.5% midpoint and whether Industrial grows the projected 20% sequentially.

Should You Invest in Analog Devices, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ADI stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Analog Devices, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ADI stock on TIKR for Free →