Key Takeaways:

- ServiceNow is still growing quickly and launching new AI workflow products, but the stock has been repriced as investors question how AI changes the software sector.

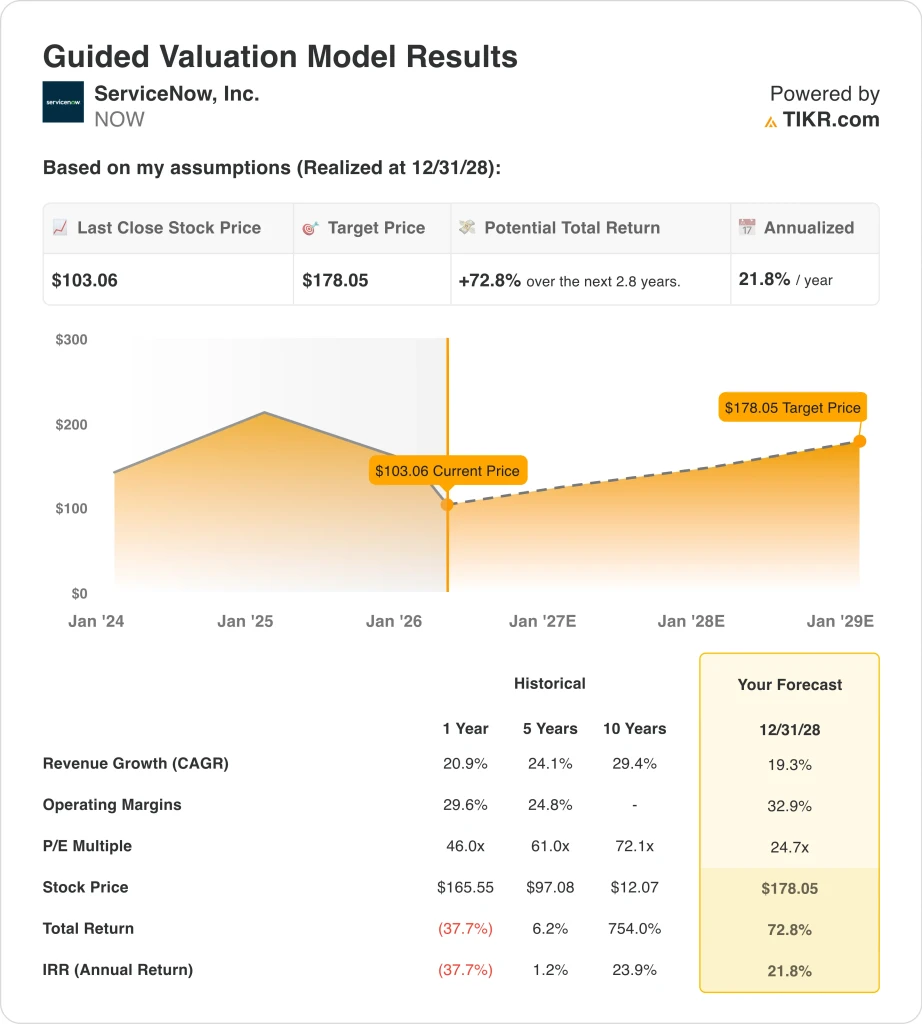

- ServiceNow stock could reasonably reach $178 per share by December 2028, based on our valuation assumptions.

- This implies a total return of 72.8% from today’s price of $103, with an annualized return of 21.8% over the next 2.8 years.

What Happened?

ServiceNow stock is moving on a mix of company execution and sector fear. In late January, the company forecast 2026 subscription revenue of $15.53 billion to $15.57 billion, above analyst expectations, and also announced another $5 billion share repurchase authorization. But Reuters reported that the stock still traded lower because investors were already worried that autonomous AI agents could pressure traditional software platforms.

That fear turned into a broader software rout. Reuters said software stocks lost nearly $1 trillion in market value last month after Anthropic introduced AI plugins for its Claude Cowork agent, which increased concerns that AI could automate tasks once handled by software suites. ServiceNow was pulled into that repricing even though its own results and guidance were strong.

The company has also kept pushing new AI products into the market. In late February, ServiceNow launched Autonomous Workforce and EmployeeWorks after closing the Moveworks deal, and in early March, it introduced government-focused AI tools for mission-critical public-sector workflows. Those launches matter because they show ServiceNow is trying to be the orchestration layer for enterprise AI, not just a legacy software vendor adding features.

Recent partnership news fits that same pattern. ServiceNow expanded its partnership with Carahsoft to broaden AI platform distribution in the U.S. and Canada, and Reuters also noted an expanded Vonage partnership on March 24. Investors now seem split between seeing a high-quality platform compounding through AI and worrying that the whole software group deserves lower multiples.

Here’s why ServiceNow stock could provide strong returns through 2030 as it monetizes enterprise AI, expands workflow automation, and converts strong subscription growth into higher margins and free cash flow. At the same time, the market is still debating how much of that value should be discounted today after the software selloff.

What the Model Says for NOW Stock

We analyzed the upside potential for ServiceNow stock using valuation assumptions based on its strong subscription growth, improving profitability, and expanding role in enterprise AI and workflow automation.

Based on estimates of 19.3% annual revenue growth, 32.9% operating margins, and a normalized P/E multiple of 24.7x, the model projects ServiceNow stock could rise from $103 to $178 per share by December 2028.

That would be a 72.8% total return, or a 21.8% annualized return over the next 2.8 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for NOW stock:

1. Revenue Growth: 19.3%

ServiceNow grew revenue 20.9% in 2025 to $13.3 billion, and fourth-quarter subscription revenue rose 21.0%. Management also guided for 2026 subscription revenue growth of 19.5% to 20.0% in constant currency, which supports a high-teens revenue outlook.

The quality of that growth also looks solid. Current remaining performance obligations rose 25.0% to $12.85 billion, and the company ended the quarter with 603 customers generating more than $5 million in annual contract value, up about 20.0%. That shows ServiceNow is still expanding inside large enterprises, even while the market worries about AI disruption.

2. Operating Margins: 32.9%

ServiceNow’s LTM EBIT margin in your overview is 15.1%, but margins have been moving higher as scale improves. In 2025, operating income rose 43.2% to $2.0 billion, and free cash flow reached $4.6 billion, equal to a 34.5% free cash flow margin.

So the model’s 32.9% operating margin assumption is clearly more ambitious than today’s EBIT margin, but it is tied to a business already showing strong incremental profitability. Management also emphasized disciplined margin expansion in the latest earnings release, which supports the case for higher normalized profitability over time.

3. Exit P/E Multiple: 24.7x

ServiceNow is trading at about 24.7x NTM P/E and 61.7x LTM P/E. The guided model uses that 24.7x forward-style multiple, so it is not assuming valuation expansion from today’s forward earnings base.

That assumption looks reasonable because the company still has a large net cash position, with LTM net debt of -$7.65 billion in your overview, and analysts remain constructive. But it also reflects a market that is less willing to pay peak multiples for software until AI winners become clearer.

Build your own Valuation Model to value any stock (It’s free!) >>>

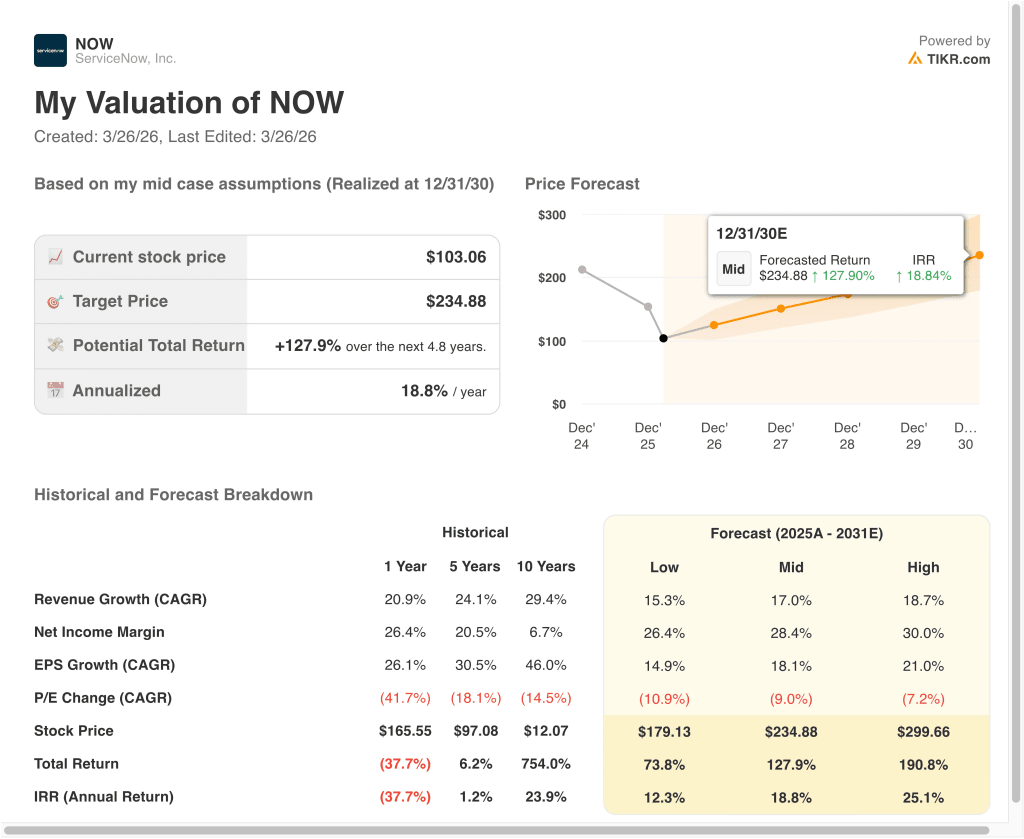

What Happens If Things Go Better or Worse?

Different scenarios for NOW stock through 2030 show varied outcomes based on AI adoption, margin expansion, and valuation durability (these are estimates, not guaranteed returns):

- Low Case: AI competition pressures multiples, and growth slows modestly → 12.3% annual returns

- Mid Case: ServiceNow compounds enterprise AI and workflow demand while margins expand → 18.8% annual returns

- High Case: AI platform adoption accelerates, and the market rewards stronger earnings growth → 25.1% annual returns

Even in the conservative case, NOW stock offers positive returns supported by its recurring revenue base, strong free cash flow generation, and net cash balance sheet.

See what analysts think about NOW stock right now (Free with TIKR) >>>

Should You Invest in ServiceNow?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up NOW, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track NOW alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze ServiceNow stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!