Key Stats for Helios Stock

- Past-Week Performance: -1.8%

- 52-Week Range: $26.8 to $76.5

- Current Price: $67.5

What Happened?

After a decade of acquisition-fueled growth that bloated margins and pushed leverage above 3x, Helios Technologies (HLIO), a motion control and electronics component maker supplying construction, agriculture, and recreation equipment globally, snapped a 12-quarter sales decline streak in 2025 and just laid out a CORE 2030 plan to double revenue to $1.6B, with shares trading at $67.54 against a Street median target of $73.

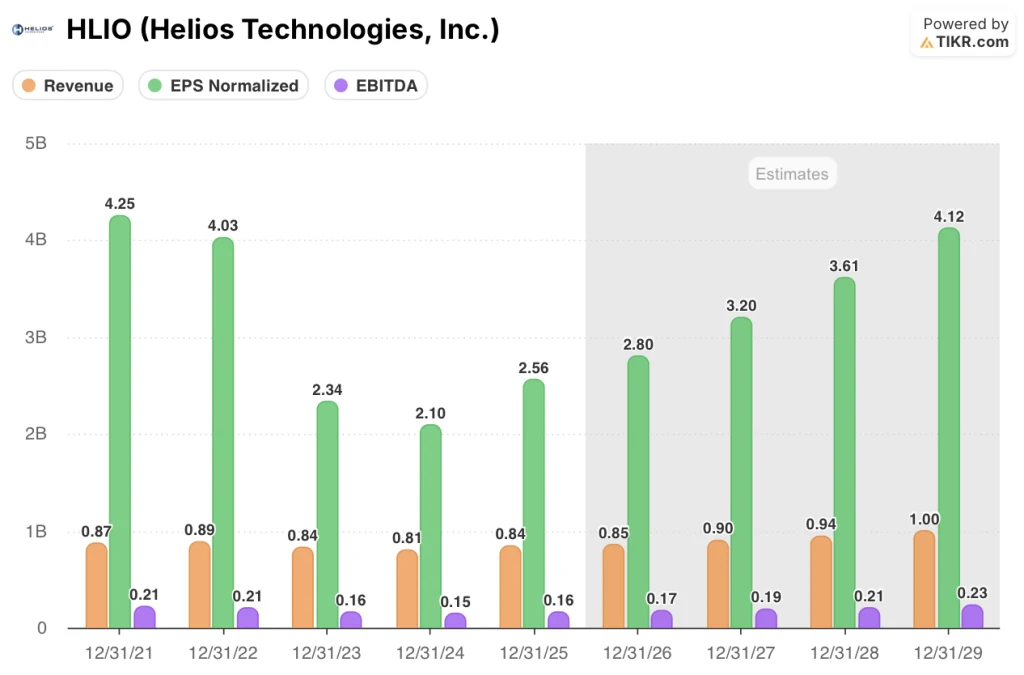

Q4 FY2025 results, released March 2, delivered the clearest proof yet: net sales hit $210.7M, a 17% gain that beat the six-analyst IBES consensus of $197M, while adjusted diluted EPS of $0.81 crushed the $0.72 estimate by 13%, and adjusted EBITDA of $42.3M topped the $40.2M consensus as gross margin expanded 350 basis points to 33.6%.

Gross margin posted its fourth consecutive quarter of expansion, reaching 33.6% in Q4 on higher volume, improved product mix, and ongoing productivity actions, a trajectory management says will reach the mid-30% range in 2026 as operating leverage builds on a largely fixed cost base requiring no new facility capacity.

At the March 20 Investor Day, Sean Bagan, President and CEO, stated on the analyst and investor day that “we are going to double the size of our sales in 5 years by 2030,” directly anchoring the CORE 2030 Strategy, which targets $1.6B in revenue, 25%-plus adjusted EBITDA margins, and a 20%-plus adjusted operating margin by that date.

Helios enters 2026 with net debt-to-EBITDA at 1.8x, $60M in new business wins secured in 2025, a $100M buyback authorization with shares repurchased at an average of ~$55, and a 33% dividend increase declared March 20, its first ever, as the Electronics segment’s Faster unit moves into the fast-growing data center liquid cooling market with a product already tested and OEM discussions underway.

Wall Street’s Take on HLIO Stock

The Q4 beat across all three headline metrics — revenue, adjusted EPS, and adjusted EBITDA — confirms that the revenue recovery Helios began in Q3 is now translating into the operating leverage that defines the bull case.

Normalized EPS is projected to grow from $2.56 in FY2025 to $2.80 in FY2026 and $4.12 by FY2029, supported by EBITDA margin expansion from 19.2% to 23.1%, as recovering volume flows across a fixed cost base requiring no material new capacity investment.

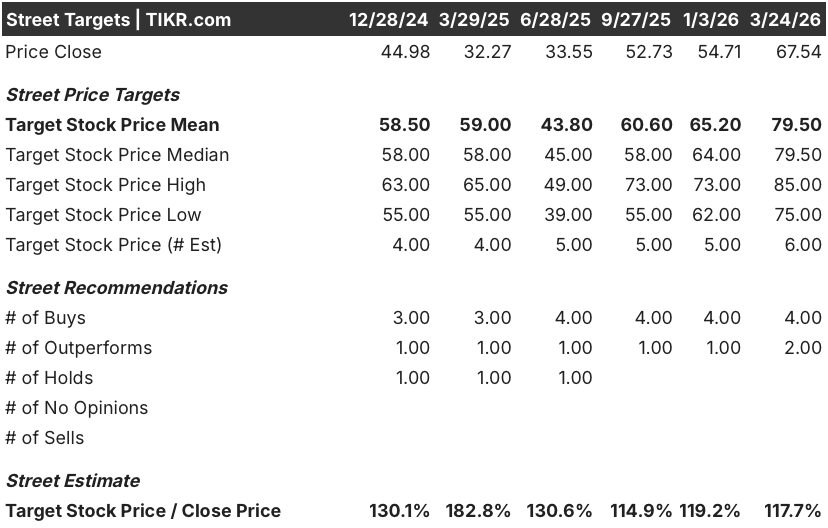

All six covering analysts rate HLIO a buy or outperform, with a mean price target of $79.50 and a median of $79.50, implying 17.7% upside from the current $67.54, as the Street prices in sustained margin recovery anchored by the CORE 2030 commitment to 25%-plus adjusted EBITDA.

The target spread runs from $75 on the low end to $85 on the high end, with the bear case hinging on second-half 2026 order deceleration and memory chip cost inflation already flagged by management, while the bull case reflects full conversion of the $60M new business win pipeline.

What Does the Valuation Model Say?

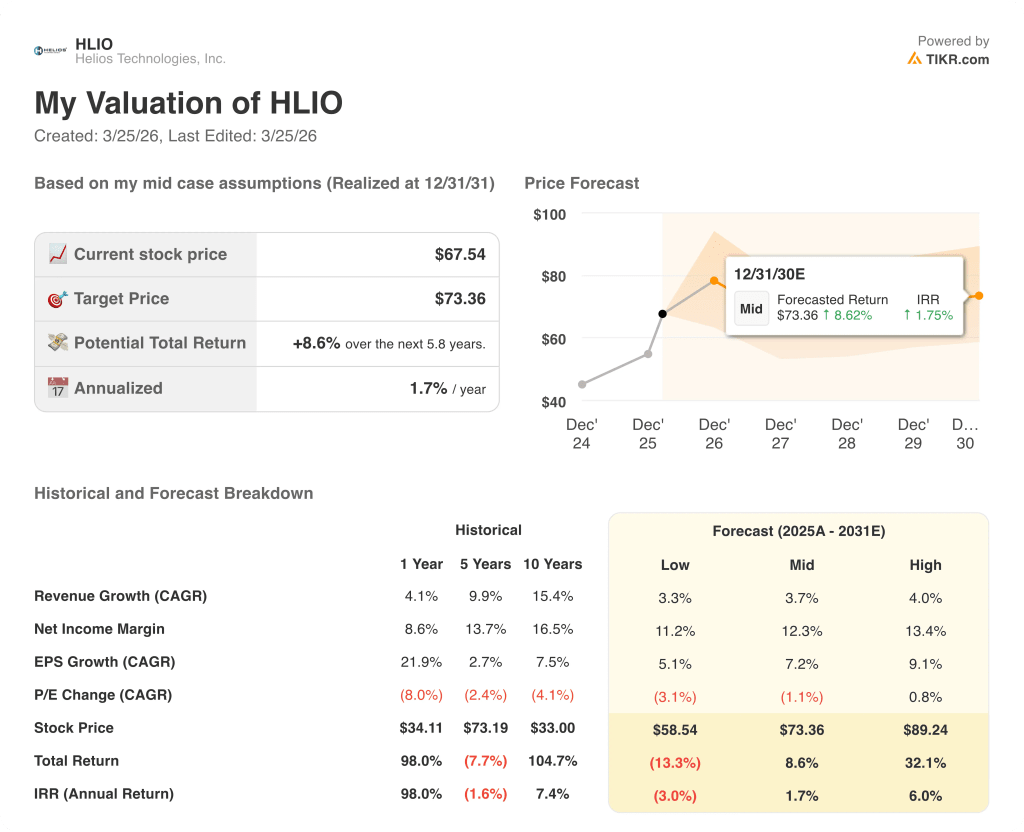

The TIKR mid-case model targets $73.36 per share on a 3.7% revenue CAGR through FY2031, a conservative assumption relative to management’s 5%-plus organic growth commitment, suggesting the model underweights the Faster data center liquid cooling opportunity already in customer discussions.

The market is pricing HLIO as a slow-growth industrial, yet four consecutive quarters of gross margin expansion and a 145% adjusted EPS gain in Q4 say otherwise.

The TIKR model’s $73.36 target reflects modest 3.7% revenue growth; the $60M in confirmed FY2025 new business wins and the MultiQTC construction equipment launch argue for the upside case at $89.24.

Management’s nine consecutive quarters of meeting or beating forward guidance is the signal: this is not an aspirational story but a demonstrated execution track record.

Tariff escalation and memory chip supply constraints, already cited by CFO Jeremy Evans as live risks for FY2026, are the developments most likely to compress the EBITDA margin expansion the TIKR model depends on.

Q1 FY2026 results are the first test of the CORE 2030 ramp; watch whether adjusted EBITDA margin holds above 19.5%, the floor of management’s own guidance range, as confirmation that operating leverage is tracking.

Should You Invest in Helios Technologies, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up HLIO stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Helios Technologies, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze HLIO stock on TIKR for Free →