Key Stats for Garmin Stock

- Past-Week Performance: -0.5%

- 52-Week Range: $169.3 to $261.7

- Current Price: $241.1

What Happened?

Fitness revenue surpassing $2 billion for the first time in FY2025 confirmed that Garmin (GRMN), a maker of GPS-enabled wearables and navigation devices across five end markets, has structurally shifted its revenue mix toward high-margin consumer health technology, with the stock trading at $241.11 against a 52-week low of $169.26.

Garmin reported Q4 pro forma EPS of $2.79 last month, up 16% year-over-year, while consolidated Q4 revenue reached $2.125 billion, a new quarterly record and the first quarter in company history to exceed $2 billion, driven by 42% growth in the Fitness segment, which sells smartwatches and health-tracking wearables.

Fitness operating income surged 50% to $726 million for the full year, with operating margin expanding 360 basis points to 31%, a pace that outstrips wearable rivals as Pemble noted most new Fitness buyers are first-time Garmin customers, signaling share capture rather than mere category growth.

Clifton Pemble, President and CEO, stated on the Q4 2025 earnings call that “the momentum in the market for our brand and for our products is still there,” tying directly to FY2026 guidance calling for $7.9 billion in revenue and operating income exceeding $2 billion for the first time.

Garmin enters FY2026 with a $500 million share repurchase program approved through December 2028, a 17% dividend increase to $4.20 annually, the Mercedes-Benz domain controller program ramping significantly from early 2027, and Fitness flagged as the top growth contributor, making the forward earnings case rest on multiple named and funded catalysts rather than a single product cycle.

Wall Street’s Take on GRMN Stock

Fitness operating margin expanding 360 basis points to 31% in a year when Garmin absorbed generationally high tariff costs confirms that the segment’s share gains carry real pricing power, not just volume uplift, directly supporting the FY2026 operating income target above $2 billion.

TIKR estimates Garmin delivers $7.98 billion in revenue and $9.38 in normalized EPS in FY2026, growth rates of 10.1% and 9.6% respectively, backed by Fitness momentum, the Outdoor back-half product cycle Pemble flagged, and Marine stabilization off improving boat-show activity.

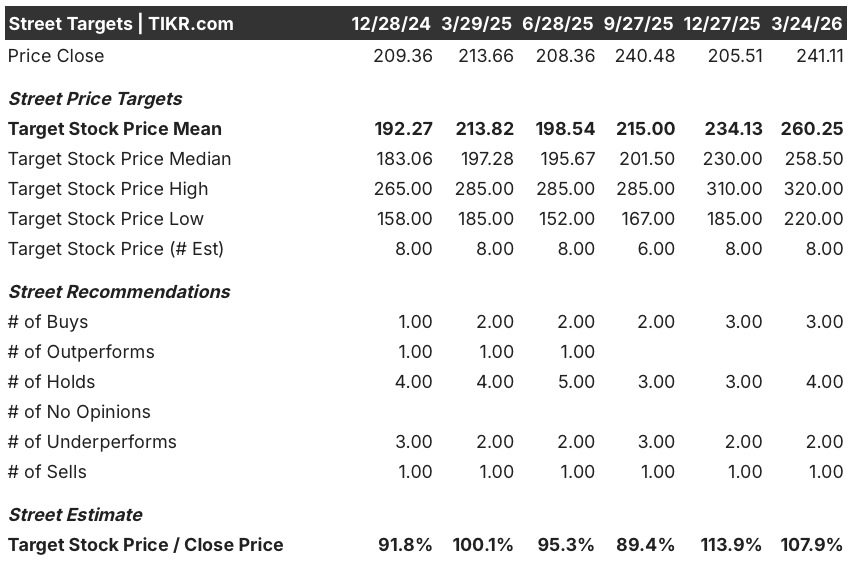

A divided Street assigns Garmin 3 buys, 4 holds, 2 underperforms, and 1 sell as of March 24, with a mean price target of $260.25 implying 7.9% upside from $241.11, a lukewarm consensus that reflects skepticism about tariff exposure and memory cost headwinds rather than any deterioration in the underlying business.

The $100 spread between the Street’s $220 low and $320 high targets reflects two distinct bets: the bear anchors on tariff permanence and Auto OEM losses persisting, while the bull prices in the Mercedes-Benz domain controller ramp beginning in early 2027 and continued Fitness share gains through a new product cycle.

What Does the Valuation Model Say?

The TIKR mid-case target of $345.36, implying a 43.2% total return through December 2030 at a 7.8% annual IRR, assumes a modest 7.9% forward revenue CAGR and net income margins of 21.7%, both conservative relative to Garmin’s 9.9% ten-year revenue CAGR and the 22.7% net income margin it posted in FY2025.

The market is pricing Garmin as a tariff-exposed hardware company, but FY2025 free cash flow of $1.36 billion on $7.25 billion in revenue, expanding to an estimated $1.64 billion in FY2026, reflects a structurally capital-light model that the current valuation does not fully credit.

Fitness operating income of $726 million on $2.36 billion in segment revenue, a 31% margin that expanded 360 basis points in one year, directly supports the TIKR model’s $345.36 target and its assumption that margin stability persists even as Garmin invests in a new Thailand manufacturing facility.

Moreover, Pemble’s confirmation that most new Fitness buyers are first-time Garmin customers, combined with Connect+’s nutrition feature driving high trial-to-paid conversion, signals a recurring-revenue layer building beneath the transactional hardware business that the Street’s hold-heavy consensus has not yet repriced.

Auto OEM operating losses of $49 million in FY2025 persist into FY2026 as BMW domain controller volumes peak; if Mercedes-Benz ramp timing slips past early 2027, the TIKR model’s FY2027 revenue estimate of $8.70 billion faces meaningful downside risk.

Garmin’s Q1 FY2026 earnings report is the first checkpoint: watch whether Fitness segment revenue sustains double-digit growth and whether management reaffirms the operating income above $2 billion target, the single figure that anchors the TIKR mid-case.

Should You Invest in Garmin Ltd.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up GRMN stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Garmin Ltd. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze GRMN stock on TIKR for Free →