Key Takeaways:

- Ford ended 2025 with record revenue of $187.3 billion, but its reported results were weighed down by large EV-related special charges and weaker profitability in its core auto business.

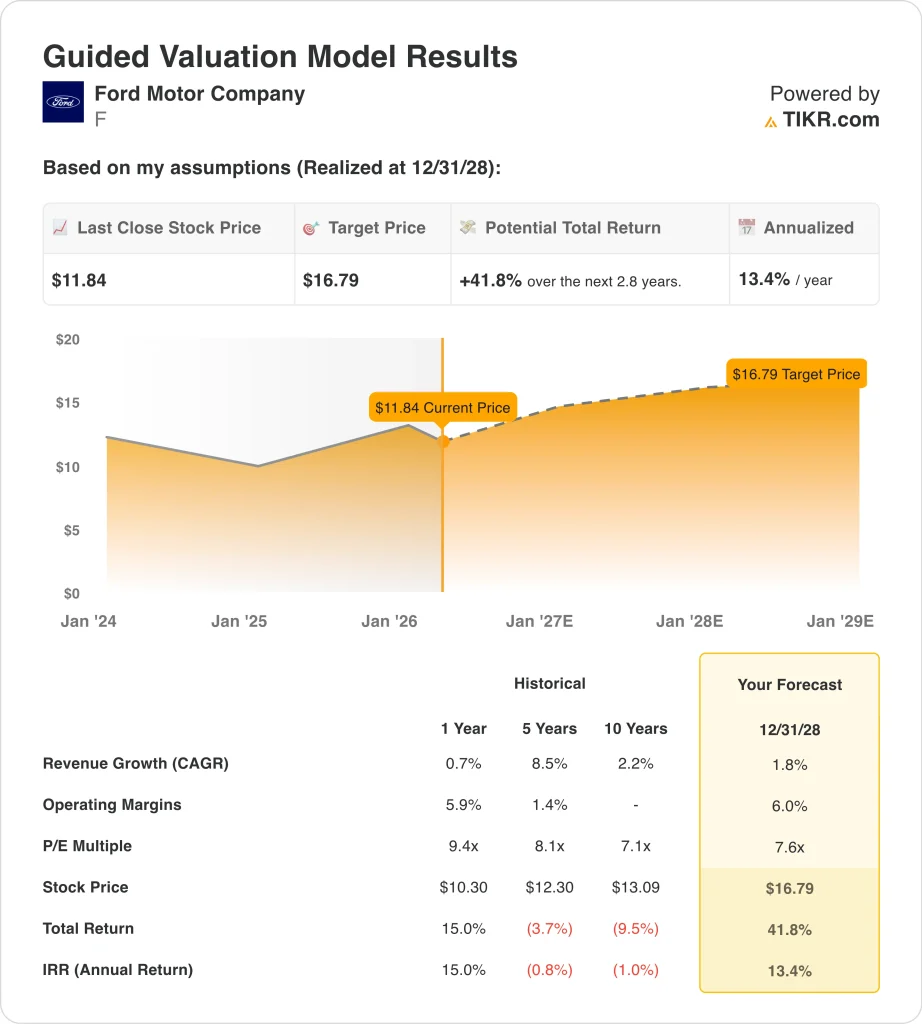

- Ford stock could reasonably reach $16.79 per share by December 2028, based on our valuation assumptions.

- This implies a total return of 41.8% from today’s price of $11.84, with an annualized return of 13.4% over the next 2.8 years.

- Ford is relevant now because investors are balancing a steadier 2026 profit outlook, a new anti-dilutive buyback plan, and a heavy stream of recalls that continues to pressure sentiment around quality and execution.

What Happened?

Ford is back in focus because the market is trying to decide whether 2025 was a reset year or a warning sign. The company reported fourth-quarter and full-year 2025 results in February, and those numbers showed record annual revenue but much weaker earnings quality. Ford posted full-year revenue of $187.3 billion, yet it also reported an $8.2 billion net loss and just $6.8 billion of adjusted EBIT after special charges tied largely to its EV strategy reset.

That mix has created a cautious tone around the stock. CEO Jim Farley said Ford delivered “a strong 2025 in a dynamic and often volatile environment,” and the company guided to $8.0 billion to $10.0 billion of adjusted EBIT for 2026. Still, investors are rethinking the setup because Ford’s auto margins remain thin, Ford Model e is still losing money, and the 2026 outlook depends heavily on cost control and better execution.

News flow in March added more pressure. Ford recalled 254,640 SUVs in the U.S. because software issues could disable the rearview camera image and some driver-assistance features. Earlier in March, there were also separate recalls affecting 1.74 million vehicles, and Ford had already issued 17 recalls in 2026 affecting more than 7.3 million vehicles.

At the same time, investors are also watching two offsetting themes. Ford disclosed an anti-dilutive repurchase program authorizing buybacks of up to 31.7 million shares, while its first-quarter 2026 results are scheduled for April 29. Rising gasoline prices are another moving piece because higher fuel costs could push some buyers toward EVs and hybrids, which matters for Ford. After all, it sells hybrids successfully but is still trying to improve EV economics.

What the Model Says for Ford Stock

We analyzed the upside potential for Ford stock using valuation assumptions based on its slower revenue profile, modest margin recovery, and low earnings multiple.

Based on estimates of 1.8% annual revenue growth, 6.0% operating margins, and a normalized P/E multiple of 7.6x, the model projects Ford stock could rise from $12 to $17 per share.

That would be a 41.8% total return, or a 13.4% annualized return over the next 2.8 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Ford stock:

1. Revenue Growth: 1.8%

Ford’s revenue base is large, but growth has slowed sharply. Total revenue rose from $176.2 billion in 2023 to $185.0 billion in 2024 and then to $187.3 billion in 2025. That means growth slowed from 11.5% in 2023 to 5.0% in 2024 and just 1.2% in 2025, which supports using a low top-line assumption.

The business mix also explains why modest growth can still matter. Ford Pro generated more than $66 billion of revenue in 2025, with $6.8 billion of EBIT and a double-digit margin, while Ford Credit increased earnings before taxes by 55% to $2.6 billion. Those businesses help offset slower growth in traditional vehicle operations, and they give Ford a more resilient base than a simple unit-sales story would suggest.

A 1.8% revenue growth assumption also fits the current industry backdrop. Higher fuel prices can help demand for hybrids and efficient vehicles, but they can also pressure consumer budgets and broader auto demand. So the model assumes Ford can keep growing, but only slowly, because the company is balancing product strength in trucks and commercial vehicles against a more mature and cyclical auto market.

2. Operating Margins: 6%

Ford’s margin recovery is the key to the valuation. The company’s operating margin was 3.0% in 2024, but it fell to -0.3% in 2025 as gross margin dropped to 5.8% from 8.4% a year earlier. That makes the 6.0% model assumption look less like a continuation of current performance and more like a recovery target tied to better execution and fewer special costs.

There are real business reasons for expecting some improvement. Ford guided to $8.0 billion to $10.0 billion of adjusted EBIT in 2026, versus $6.8 billion in 2025, and it said Ford Model e’s EBIT loss should improve to $4.0 billion to $4.5 billion from $4.8 billion last year. Ford Pro is still the main earnings engine, and Ford Blue remains profitable even though its margins have narrowed.

Still, that 6.0% assumption is not aggressive when viewed against the risks. Recalls keep raising questions about quality, and quality problems can pressure warranty costs, brand perception, and dealer confidence. So the model assumes Ford can recover margins, but not to a level that ignores the operational issues investors are watching closely.

3. Exit P/E Multiple: 7.6x

Ford already trades at a low earnings multiple relative to much of the market. The TIKR overview shows a 7.8x NTM P/E, while the guided valuation model uses a 7.6x exit P/E. That means the model does not assume investors will suddenly pay a premium for the stock by 2028.

This low multiple reflects real concerns. Ford’s LTM EBIT margin is -0.3%, its LTM ROE is -20.2%, and its LTM net debt stands at $137.3 billion, with net debt to EBITDA of 21.9x in the overview. Those figures help explain why investors continue to value Ford as a leveraged cyclical manufacturer rather than a higher-quality industrial compounder.

At the same time, the multiple is not disconnected from Ford’s history. The guided model shows a 5-year historical P/E of 8.1x and a 10-year historical P/E of 7.1x, so a 7.6x exit multiple sits near where the stock has traded over longer periods. That makes the valuation framework relatively grounded because it assumes Ford earns a familiar multiple rather than a re-rating story.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

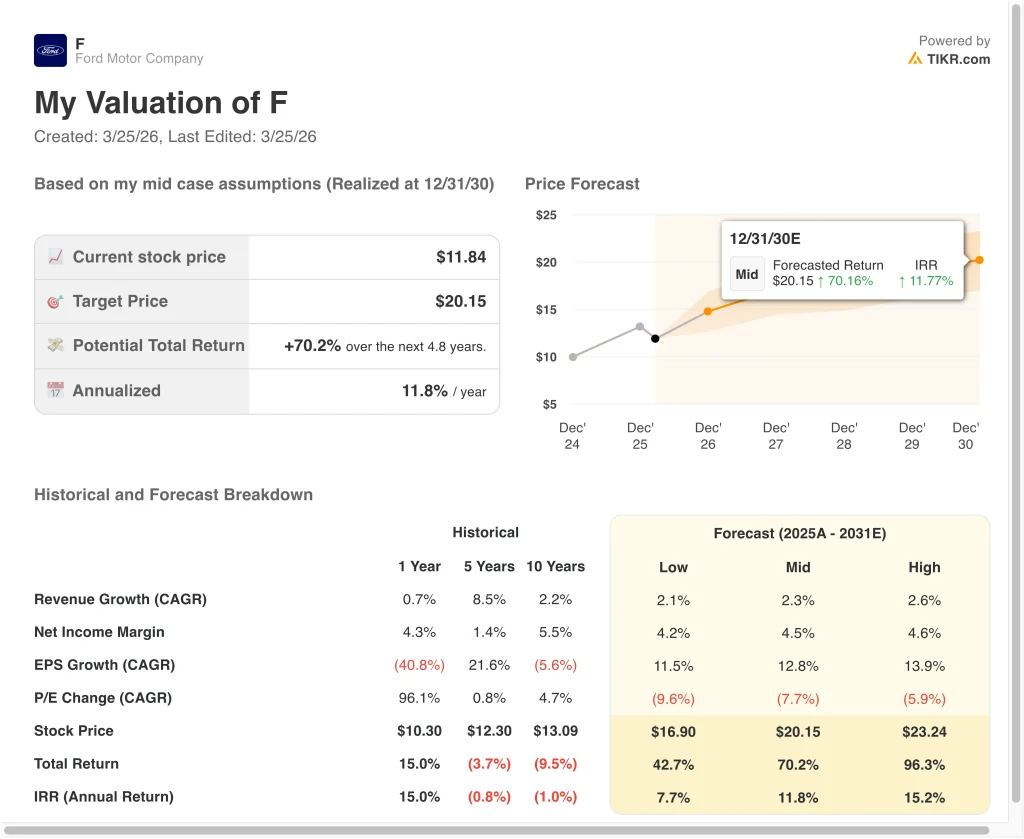

Different scenarios for Ford stock through 2030 show varied outcomes based on margin recovery, EV losses, and capital allocation discipline (these are estimates, not guaranteed returns):

- Low Case: Ford’s revenue growth stays modest, EV losses remain elevated, and the valuation compresses further → 7.7% annual returns

- Mid Case: Ford Pro stays strong, margins recover gradually, and the business delivers steadier earnings growth → 11.8% annual returns

- High Case: Ford improves EV economics, holds pricing, and expands profits across Ford Blue and Ford Pro → 15.2% annual returns

Even in the conservative case, Ford stock offers positive returns supported by its large cash generation, entrenched truck franchise, and strong commercial vehicle business. Cash from operations rose to $21.3 billion in 2025, and free cash flow increased to $12.5 billion, even with heavy capital spending. That matters because Ford still has the financial capacity to invest, pay dividends, and offset some dilution through buybacks.

The mid case likely depends on execution more than macro help. Ford needs Ford Pro to keep producing high margins, Ford Blue to remain profitable, and Ford Model e to lose less money over time. It also needs recalls and quality issues to stop dominating the story, because those issues can delay any improvement in investor confidence.

The high case would probably require a cleaner operating backdrop. Higher fuel prices could help hybrids and efficient vehicles, while a steadier regulatory path could make long-term planning easier for automakers. But Ford still has to prove that better products, tighter costs, and fewer quality setbacks can convert a huge revenue base into sustainably better margins.

See what analysts think about Ford stock right now (Free with TIKR) >>>

Should You Invest in Ford Motor Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Ford, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Ford alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Ford Motor stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!