Key Takeaways:

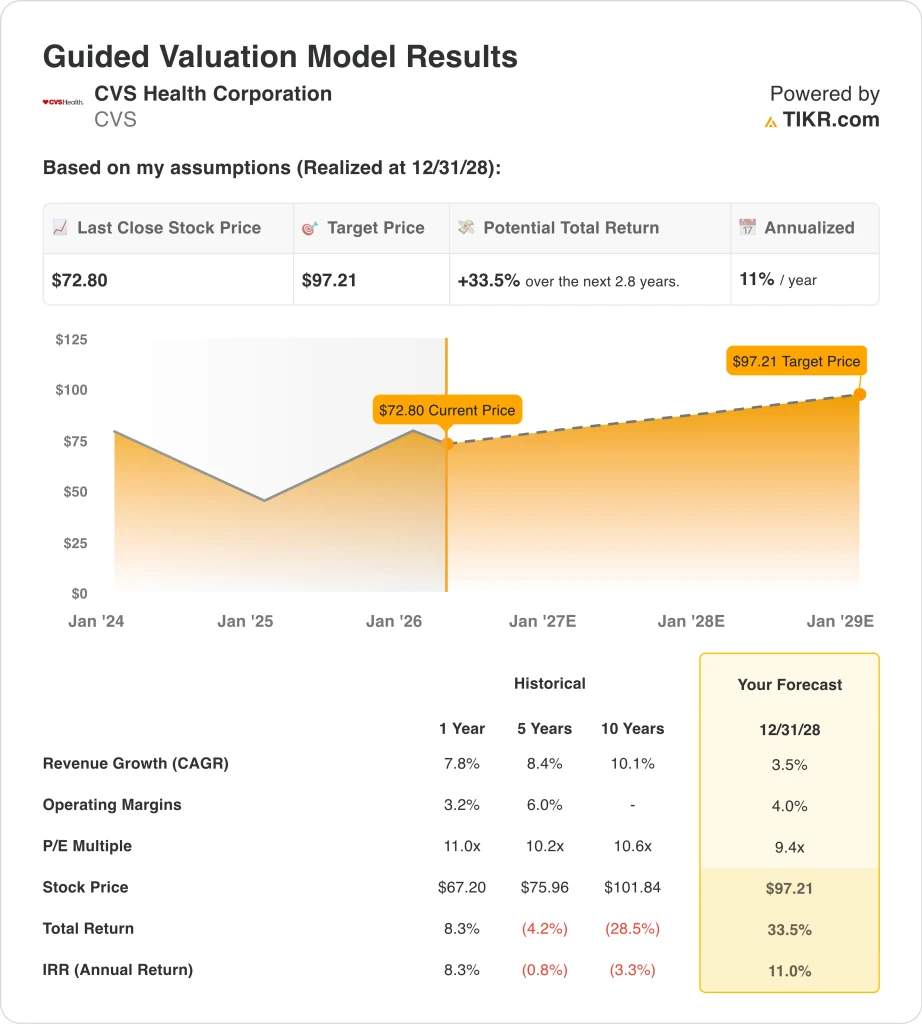

- CVS stock could reasonably reach $97 per share by December 2028 based on valuation assumptions.

- This implies a 33.5% total return from today’s price of $73, or 11% annualized returns over the next 2.8 years.

- Revenue growth remains stable, but margins and regulatory risks are key drivers of valuation.

CVS Health Corporation (CVS) is back in focus as investors reassess the healthcare giant’s earnings power following a volatile 2025. The stock has recovered from its 2024 lows but remains below prior highs, reflecting ongoing uncertainty around margins, regulatory scrutiny, and insurance profitability.

Recent headlines have driven much of the stock’s movement, particularly around legal settlements, partnerships, and earnings surprises. CVS Health reported Q4 2025 adjusted EPS of $1.09, beating expectations, which helped stabilize sentiment after a difficult year. At the same time, developments like the FTC insulin pricing settlement and Aetna’s $117.7 million Medicare-related settlement continue to weigh on investor confidence.

The company is also leaning into innovation, highlighted by its partnership with Google Cloud to launch AI-driven healthcare platforms. This signals a strategic shift toward technology-enabled care, which management believes can improve engagement and efficiency. However, investors remain cautious as execution risks and cost pressures persist across its insurance and pharmacy segments.

Here’s why CVS stock could deliver moderate returns through 2028 as it stabilizes margins and navigates regulatory headwinds.

What the Model Says for CVS Stock

We analyzed the upside potential for CVS stock using valuation assumptions based on its diversified healthcare platform, steady revenue growth, and margin recovery potential.

Based on estimates of 3.5% annual revenue growth, 4.0% operating margins, and a 9.4x P/E multiple, the model projects CVS stock could rise from $73 to $97 per share.

That would represent a 33.5% total return, or 11% annualized returns over the next 2.8 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for CVS stock:

1. Revenue Growth: 3.5%

CVS Health generated nearly $400 billion in revenue over the last twelve months, reflecting consistent growth across its pharmacy, insurance, and health services segments. Revenue has increased from $291 billion in 2021 to $399 billion in 2025, showing resilience despite industry pressures.

However, growth has slowed in recent years, with 2024 growth at 3.9% before rebounding to 7.9% in 2025. This reflects normalization after pandemic-driven demand and ongoing adjustments in insurance pricing and utilization trends.

Based on analysts’ consensus estimates, we use a 3.5% growth assumption, reflecting stable but mature business expansion.

2. Operating Margins: 4%

CVS operating margins have declined significantly from 4.9% in 2021–2022 to just 2.2% in 2024 before recovering slightly to 2.5% in 2025. This compression reflects higher medical costs, insurance utilization, and restructuring charges.

The company also recorded significant impairments and legal expenses, including a $5.7 billion goodwill impairment and ongoing settlement costs. These factors have materially impacted profitability and investor sentiment.

Based on analysts’ consensus estimates, we assume margins recover to 4.0%, supported by cost control initiatives, AI-driven efficiencies, and normalization in healthcare utilization trends.

3. Exit P/E Multiple: 9.4x

CVS currently trades at a relatively low valuation compared to historical levels, reflecting investor concerns around growth durability and margin pressure. The stock’s multiple has compressed alongside declining earnings and rising uncertainty in its insurance business.

Street price targets currently average around $96.50, suggesting upside from current levels. At the same time, analyst sentiment has improved, with buy ratings increasing to 18 and fewer hold recommendations.

Based on analysts’ consensus estimates, we use a 9.4x P/E multiple, slightly below historical averages, to reflect a balanced view of risk and recovery potential.

Build your own Valuation Model to value any stock (It’s free!) >>>

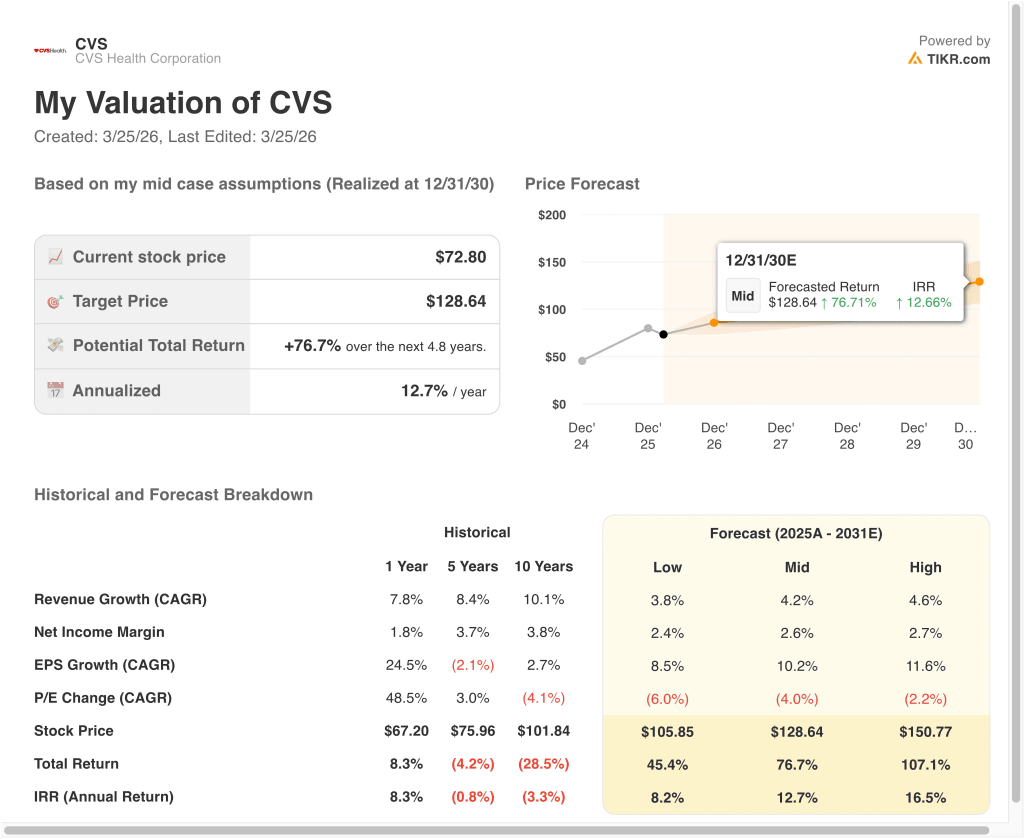

What Happens If Things Go Better or Worse?

Different scenarios for CVS stock through 2030 show varied outcomes based on margin recovery and execution (these are estimates, not guaranteed returns):

- Low Case: Margin recovery stalls and regulatory pressures persist → 8.2% annual returns

- Mid Case: Stable growth and moderate margin expansion → 12.7% annual returns

- High Case: Strong execution and cost control drive earnings growth → 16.5% annual returns

The range of outcomes highlights how sensitive CVS is to operating margins and healthcare cost trends. While revenue growth remains steady, profitability is the key swing factor in valuation.

CVS stock movement in 2026 has been driven by a mix of earnings results, regulatory developments, and strategic initiatives. The Q4 2025 earnings beat provided short-term support, but ongoing legal and regulatory challenges continue to create volatility.

Recent developments, such as the FTC insulin pricing settlement and Aetna’s Medicare-related settlement, have added uncertainty. These issues highlight broader industry scrutiny around pricing and reimbursement practices, which directly impact CVS’s insurance and pharmacy businesses.

At the same time, the company’s partnership with Google Cloud signals a push toward innovation and digital transformation. This aligns with broader healthcare trends toward AI and data-driven care, but investors are still waiting for clear financial benefits.

Looking ahead, the upcoming Q1 2026 earnings report on May 6 will be a key catalyst. Investors will focus on margin trends, medical cost ratios, and progress in stabilizing the insurance segment.

See what analysts think about CVS stock right now (Free with TIKR) >>>

Should You Invest in CVS Health Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CVS, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CVS alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze CVS Health Corporation stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!