Key Stats for CRM Stock

- Past week’s performance: -1.5%

- 52-week range: $174.6 to $296.1

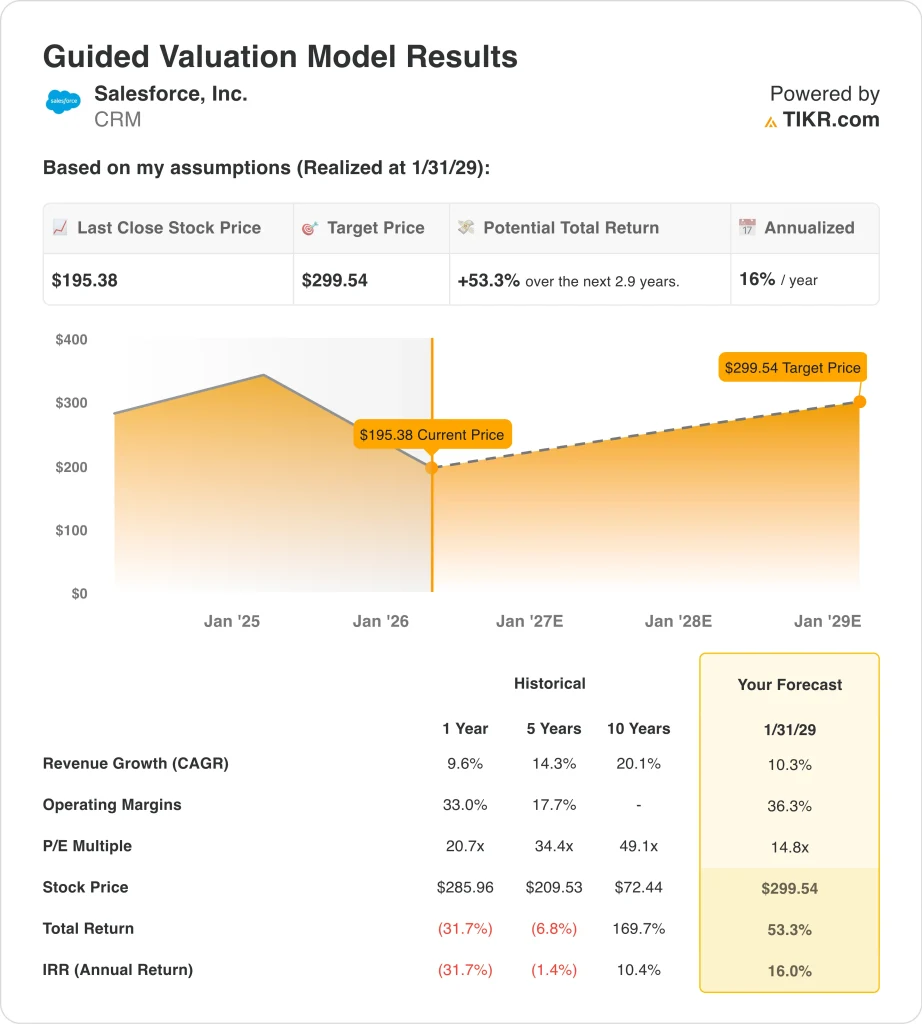

- Valuation model target price: $300

- Implied upside: 53.3% over 2.9 years

Value your favorite stocks like CRM with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Salesforce (CRM) stock has stayed under pressure in recent weeks, even though the business just posted record annual revenue and profit. Shares were at $194.90 on March 23. That tells you investors are still debating the company’s growth outlook and AI positioning, not just its latest results.

The biggest recent development was capital allocation. Salesforce launched a $25 billion accelerated share repurchase on March 16, and it said the initial delivery was about 103 million shares. The company had already priced $25 billion of senior notes on March 11, so the market is weighing the benefit of aggressive buybacks against a higher debt load.

At the same time, investors are still focused on software-wide AI disruption fears. Software stocks sold off earlier this year as investors worried AI tools could pressure traditional enterprise software models, and Salesforce was among the names impacted in that decline. The company is still seen as relatively well-positioned because of its proprietary customer data and enterprise integration.

The company has also tried to reinforce that message with product news and public appearances. Salesforce announced a new NVIDIA partnership on March 17 to bring Agentforce and NVIDIA models into enterprise workflows, and management has stayed visible through investor and industry events this month. So the stock’s recent move looks less like a reaction to one headline and more like a market still sorting out how much AI can help, or hurt, software valuations.

See analysts’ growth forecasts and price targets for CRM (It’s free) >>>

Is CRM Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 10.3%

- Operating Margins: 36.3%

- Exit P/E Multiple: 14.8x

Based on these inputs, the model estimates a target price of $299.54. That implies a 53.3% total return from the current share price of $195.38 and a 16.0% annualized return over the next 2.9 years. Those are strong modeled returns, but they still depend on Salesforce sustaining margin gains and steady growth.

The underlying business has been moving in the right direction. Fiscal 2026 revenue rose 10% to $41.5 billion, while gross margin reached 77.7% and operating margin improved to 21.5%. This shows Salesforce can still expand profitability even as growth moderates from earlier years.

Cash generation is also a major part of the valuation case. Free cash flow reached $14.4 billion in fiscal 2026, and free cash flow margin was 34.7%, which supports buybacks, dividends, and continued investment. That level of cash flow is one of the key reasons management has leaned into aggressive capital returns.

Even so, the valuation model is not assuming hypergrowth. Revenue growth is modeled at 10.3%, which aligns closely with the company’s recent performance. The larger driver of upside is margin expansion, reflecting ongoing cost discipline and operating leverage.

What’s Driving the Stock Going Forward?

The next move in Salesforce stock will likely depend on whether AI turns into measurable business results. Investors already understand the company’s AI strategy, but they are watching for evidence that it drives stronger bookings, higher deal sizes, or faster revenue growth. Until that shows up clearly in results, sentiment may remain mixed.

Margins will matter just as much as growth. Salesforce’s operating margin reached 21.5% in fiscal 2026, while the valuation model assumes 36.3% by 2029. Continued margin expansion would support earnings growth and justify higher valuation multiples.

Capital allocation is another major factor. The $25 billion accelerated share repurchase could support EPS growth and reduce share count, but the associated debt financing adds a new layer of scrutiny. Investors will be watching whether the balance between buybacks and leverage remains disciplined.

There are also clear near-term catalysts ahead. The company is set to pay a $0.44 dividend on April 9 and is expected to report fiscal Q1 2027 results on May 27. These events should provide updated insight into demand trends, AI monetization, and whether Salesforce can sustain its combination of growth and profitability.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Salesforce, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CRM, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CRM alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Salesforce stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!