Key Stats for Copart Stock

- Past-Week Performance: +1.6%

- 52-Week Range: $32.2 to $63.9

- Current Price: $33.4

What Happened?

Total loss frequency at U.S. auto insurers hit 24.2% in Q4 calendar 2025, up from 15.6% a decade ago, yet Copart (CPRT), the online salvage vehicle auctioneer that sells totaled and damaged cars on behalf of insurers to dealers and dismantlers globally, posted Q2 EPS of $0.36 against a $0.39 consensus, sending shares down 12% to $33 as softer insurance volumes briefly obscured a structural tailwind now trading at a 48% discount to its 52-week high of $63.85.

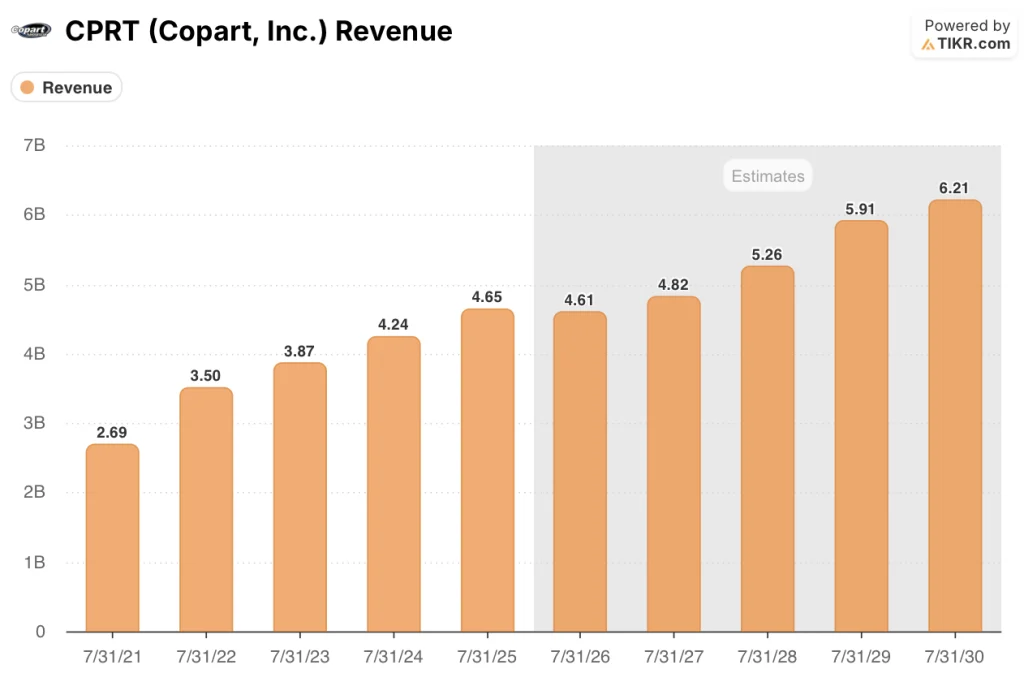

Copart reported Q2 revenue of $1.12 billion on February 19, down 3.6% year over year, as global insurance unit volumes fell 9.3%, though stripping out Hurricanes Helene and Milton catastrophe units processed in the prior year, the comparable revenue decline narrows to just 1.3% growth.

Record U.S. insurance average selling prices, up 9% ex-catastrophe units and outpacing all industry benchmarks, proved the auction marketplace’s pricing power even as unit volumes compressed, with gross profit declining 6.2% to $492.8 million but ex-CAT gross margin expanding 178 basis points to 45%.

CEO Jeff Liaw stated on the Q2 2026 earnings call that “our selling customers have also voted with their pocketbooks, entrusting us with more pure sale units than they ever have before, knowing our auction will achieve a full and fair market value,” directly validating the platform’s pricing superiority as the core competitive argument against cheaper rivals.

Copart’s $6.4 billion liquidity position, zero debt, 58% year-to-date free cash flow growth, and over $500 million in share repurchases fiscal year to date through February give it durable reinvestment capacity as rising total loss frequency, now at 24.2% versus 15.6% in 2015, structurally expands the addressable pool of vehicles over the next 3 to 5 years.

Wall Street’s Take on Copart Stock

The Q2 volume miss, driven by the hurricane base effect and consumer underinsurance trends Liaw described as cyclical, explains the revenue dip but not the structural free cash flow story accelerating underneath it.

TIKR estimates revenue recovers to $4.82 billion in FY2027 after a 0.9% dip in FY2026, supported by record U.S. insurance ASPs up 9% ex-CAT and continued international noninsurance unit growth of 9.1% in Q2, both already seeded in the earnings report.

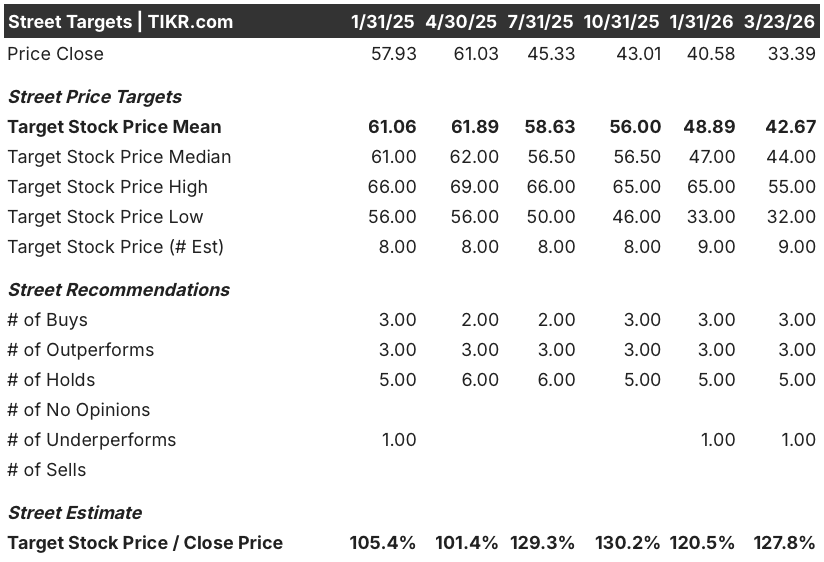

Nine analysts currently cover Copart with 3 buys, 3 outperforms, 5 holds, and 1 underperform; their mean target of $42.67 implies 27.8% upside from $33.39, grounded in expectations that the volume headwind proves temporary as insurance carrier growth reinvestment resumes.

The spread between the $32 low target and $55 high target is the widest it has been in over a year, with the bear case anchored to insurance unit volume staying structurally impaired and the bull case anchored to total loss frequency continuing its decade-long climb from 15.6% in 2015 to 24.2% today.

What Does the Valuation Model Say?

The TIKR mid-case target of $45.68 implies 36.8% total return by July 31, 2030 at a 7.5% IRR, built on a modest 5.8% revenue CAGR and net income margins holding at 31.5%, assumptions Copart’s $6.4 billion liquidity base and zero-debt structure make credible even under continued near-term volume pressure.

The market is pricing a secular volume decline; FCF margin expanding from 26.5% in FY2025 to an estimated 31.9% by FY2027 directly contradicts that read.

Copart’s over $500 million in fiscal year-to-date buybacks at prices above current levels and the TIKR mid-case target of $45.68 together make the case that management and the model agree: $33 is mispriced.

CEO Jeff Liaw’s February 19 disclosure of personal engagement with AI coding platforms and approximately 1,000 full-time engineers confirm this is a technology-led marketplace, not a commodity trucking operation, which the current 22x forward P/E does not reflect.

If insurance carrier policy growth fails to resume and U.S. insurance unit volumes remain down double digits beyond FY2026, the TIKR model’s 4.7% revenue recovery assumption for FY2027 breaks and the $45.68 target is not achievable.

Q3 FY2026 results, expected around May 2026, will confirm whether ex-CAT unit volume trends are stabilizing; watch U.S. insurance unit growth ex-direct-buy as the single most important number.

Should You Invest in Copart, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CPRT stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Copart, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CPRT stock on TIKR for Free →